Vietnam Commercial Vehicle Market: By Vehicle Class (Light Commercial Vehicles (LCV), Medium Commercial Vehicles (MCV), Heavy Commercial Vehicles (HCV), Specialty Vehicles); Vehicle Type (Trucks, Vans, Passenger Commercial Vehicles, Delivery Vans / Urban Delivery Units, Special Vehicles); Propulsion Type (Internal Combustion Engine (ICE) and Electric Commercial Vehicles); Power Output (<150 hp, 150-250 hp, 250-350 hp, 350 hp (Heavy-Duty Long-Haul & Mining)); By Weight (Class 1-3: Up to 6 tons, Class 4-6: 6-16 tons, Class 7-8: 16+ tons); Application (Logistics & Transportation, Construction & Mining, Public Transport, Agriculture & Forestry, Oil & Gas, Municipal Services, Tourism & Hospitality Transport, Government & Defense, Others); Sales Channel (OEM / New Vehicle Sales, Aftermarket / Fleet Refurbishment, Leasing & Rentals); Region—Market Size, Industry Dynamics, Opportunity Analysis and Forecast for 2026–2035

- Last Updated: 25-Dec-2025 | | Report ID: AA12251624

Market Scenario

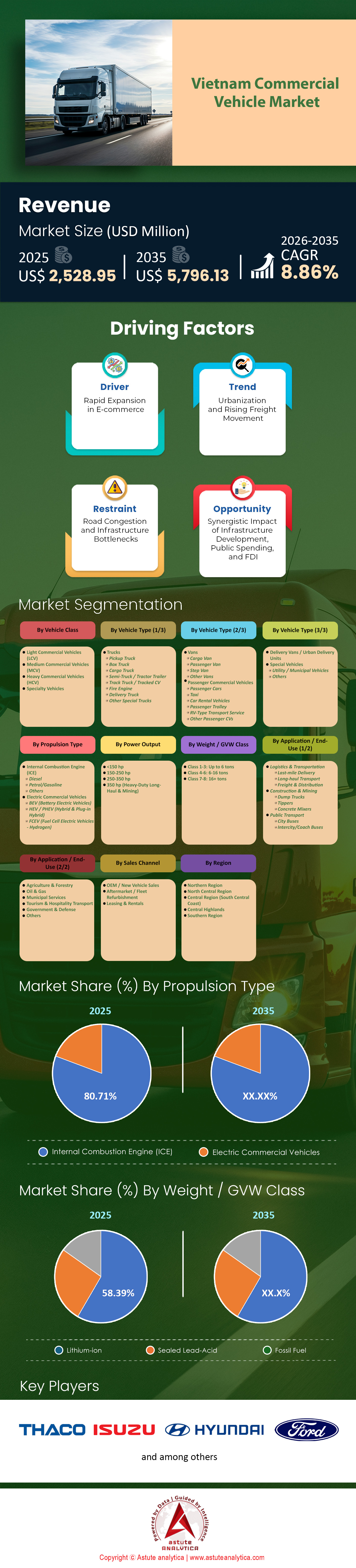

Vietnam commercial vehicle market size was valued at USD 2,528.95 million in 2025 and is projected to hit the market valuation of USD 5,796.13 million by 2035 at a CAGR of 8.86% during the forecast period 2026–2035.

Key Findings

- Based on vehicle class, light commercial vehicles drives the dominance in the Vietnam commercial vehicle market. They accounts for more than 26.17% market share.

- Based on vehicle type, trucks generate nearly 51% revenue of the Vietnam market.

- Based on propulsion, ICE still dominates the market by capturing more than 80.71% market share.

- Based on power output, commercial vehicles having <150 hp power takes the lead and capture the highest 54% market share.

- Based on weight/GVW Class, commercial vehicles having weight carrying capacity Up to 6 tons takes the lead and dominates the market by accounting for more than 58.39% market share.

In the last few years, the Vietnam commercial vehicle market has decisively shifted from recovery to structural expansion, reshaping the Southeast Asian automotive landscape. Following a period of post-pandemic volatility that tested the resilience of manufacturers and logistics providers, the market is now propelled by urgent capacity building rather than simple fleet replacement. The sentiment across the country—from the bustling ports of Hai Phong to the industrial parks of Binh Duong—is one of cautious but palpable optimism. Stakeholders are realizing that the window to capitalize on Vietnam’s infrastructure-led automotive boom is fully open, driven by a $460 billion economy aggressively positioning itself as the region's new manufacturing hub.

To Get more Insights, Request A Free Sample

What Do the Numbers Reveal About Market Velocity?

To understand the Vietnam commercial vehicle market's trajectory, we must look at the pivotal turnaround of 2024 and the accelerated growth of 2025. The year 2024 concluded with the Vietnam Automobile Manufacturers Association (VAMA) reporting commercial vehicle sales of 79,332 units, a solid 15% year-on-year increase that signaled B2B confidence returning faster than consumer sentiment. However, a holistic view requires including non-VAMA giants like TC Motor (Hyundai), which reported 10,385 commercial units, placing the total estimated 2024 volume between 90,000 and 95,000 units.

The momentum in the Vietnam commercial vehicle market has only gathered speed in 2025. Based on current economic modeling, the total market is on track to breach the 105,000 to 110,000 unit mark by December 31, representing a weighted growth of approximately 10-12%. Within this aggregate, Heavy-Duty Trucks (HDT) are expected to rise by 9.5%, while Light Commercial Vehicles (LCVs) are witnessing the highest velocity with a projected 14% growth. Even the dual-use pickup segment remains robust, where the Ford Ranger alone sold 17,508 units last year, driving the category to another 8-10% expansion.

Why is Demand for Commercial Vehicles Accelerating?

The sales growth across the Vietnam commercial vehicle market is led by three economic cylinders creating a perfect storm for procurement. First is the government's aggressive public investment blitz, with a staggering 2025 disbursement target of nearly VND 900 trillion ($36 billion). This liquidity flows directly into infrastructure megaprojects like the North-South Expressway and Phase 1 of Long Thanh International Airport, necessitating massive fleets of dump trucks and heavy haulers.

Simultaneously, realized Foreign Direct Investment (FDI) capital, which reached a record $23.2 billion in 2023, continues to drive demand. As global electronics giants open factories in provinces like Bac Giang, the logistics "tail" required to service them expands, directly correlating industrial output with medium-duty truck sales. Furthermore, the digital economy is reshaping urban logistics; with an e-commerce market projected to hit $29 billion by the end of 2025, the demand for vans and light trucks under 2.5 tons is insatiable as providers race to serve a population with 70% internet penetration.

Who Holds the Power in this Competitive Landscape?

Vietnam commercial vehicle market structure remains an intense oligopoly dominated by local assemblers with strong foreign partnerships. Thaco (Truong Hai Auto Corporation) sits at the pinnacle, leveraging its Chu Lai manufacturing complex to secure approximately 20-25% of the specialized commercial market, having sold nearly 19,000 trucks and buses in the previous year. However, they face fierce competition from TC Motor, whose Hyundai Porter H150 and Mighty series drove over 10,000 unit sales, cementing a strong second position. In the specialized "dual-use" niche, Ford is the undisputed king, capturing a staggering 75% market share in pickups and holding a near-monopoly of over 60% in the 16-seat commercial van category.

Meanwhile, Japanese giants Isuzu and Hino control the "profitability" segment, dominating corporate fleets where Total Cost of Ownership (TCO) is paramount. Isuzu’s massive 63.7% growth spike in late 2024 proves that as the economy stabilizes, businesses are returning to premium reliability.

How Are Economic Conditions Influencing Purchasing Power?

The economic backdrop of Vietnam commercial vehicle market influences purchasing decisions through a mix of relief and pressure. A critical stabilizer has been the State Bank of Vietnam cooling lending rates to around 8-10% for corporate borrowers, a significant drop from the 13-14% peaks of 2023. This 300-400 basis point reduction is vital for fleet operators who typically finance 70-80% of purchases, allowing them to upgrade fleets without destroying balance sheets.

Additionally, forecasted GDP growth of 6.8% to 7% is restoring business confidence. However, the exchange rate remains a silent profit killer; with the VND under pressure against the USD and roughly 80% of truck components imported, currency fluctuation is pushing buyers toward locally assembled (CKD) units to avoid the price volatility of Completely Built-Up (CBU) imports.

Where Are the New Revenue Pockets Emerging in the Vietnam Commercial Vehicle Market?

New money is migrating rapidly toward specialization. Cold chain logistics is the hottest segment in the Vietnam commercial vehicle market, valued at $202 million and expected to reach $295 million by late 2025, driving demand for refrigerated trucks at double the rate of general cargo vehicles. Simultaneously, urbanization is fueling a surge in specialized construction vehicles like concrete pumps and mobile cranes, which offer higher dealer margins. The electric CV market is also awakening; VinFast is aggressively entering the space, while Chinese OEMs like BYD and Dongfeng are piloting electric light trucks in Hanoi and Ho Chi Minh City to anticipate future "zero-emission zones."

What Trends and Challenges Are Reshaping the Horizon?

Buyer behavior across the Vietnam commercial vehicle market is being fundamentally altered by modernization trends, specifically the enforcement of Euro 5 emission standards which is forcing a fleet replacement cycle. In parallel, telematics has become standard, with adoption rising to over 75% for heavy-duty fleets in 2024 as owners seek to combat logistics costs that hover at a high 16-18% of GDP. Additionally, the "China+1" shift is increasing cross-border trucking demand for high-power tractor units.

However, the road ahead contains potholes; logistics bottlenecks squeeze margins, and infrastructure lag limits LCV efficiency, with delivery vans in Ho Chi Minh City averaging only 15-20 km/h. Finally, policy uncertainty following the expiration of the 50% registration fee cut keeps the industry anxious for new incentives to sustain the current momentum.

Segmental Analysis

Heavy Commercial Vehicles to Keep Dominating the Market

Heavy commercial vehicles (HCVs) in Vietnam are controlling the largest 37.49% revenue share. The dominance of the segment is inextricably linked to the sheer volume of physical assets being moved to support industrialization. With the Cai Mep - Thi Vai port cluster processing 152 million tonnes of cargo in 2024, light trucks simply cannot handle the throughput. The market requires high-capacity tractor-trailers to clear the 6.5 million TEUs that arrived that year. Furthermore, the handling of 918 vessels, including 321 massive mother ships, necessitates a synchronized fleet of heavy haulers capable of port-to-factory transport. The logistics density is so high that total seaport throughput hit 501.117 million tonnes in just seven months, making HCVs the only viable solution for inter-provincial freight.

Moreover, the scale of construction projects demands heavy-duty capability. The 422 trillion VND transport budget is largely channeled into earthworks and highway construction, tasks that require heavy dump trucks and mixers. Specific projects, such as the 1.43 trillion VND infrastructure component of the Da Nang industrial park, or the 2.47 trillion VND disbursement for the airport terminal, rely exclusively on heavy machinery. When industrial FDI hits USD 5.63 billion, it translates directly into steel, cement, and machinery transport. Consequently, the Vietnam commercial vehicle market favors HCVs because the nation is currently in a phase of heavy physical development where payload capacity is the primary metric of efficiency.

The Enduring Reign of ICE: Operational Superiority in Vietnam's Commercial Fleets

Internal Combustion Engine (ICE) vehicles maintain unwavering dominance in the Vietnam commercial vehicle market, capturing more than 80.71% market share due to established reliability and infrastructure. Fleet operators remain hesitant to transition to electric alternatives given the severe lack of charging stations; only 30% of planned stations were operational by 2024. Diesel engines offer the necessary torque and an extensive range of 800 to 1,000 kilometers, crucial for long-haul routes like Hanoi to Ho Chi Minh City that currently challenge battery capacities. Economic pragmatism further tethers businesses to diesel, as refueling takes merely 10 minutes compared to the hours required for EV charging, and ICE trucks avoid the 500 to 1,000-kilogram payload penalty imposed by battery packs.

Vietnam’s 50,000 kilometers of national highways are perfectly suited for ICE transport, further adding fuel to their sell in the Vietnam commercial vehicle market. These engines boast commercial lifespans exceeding 500,000 kilometers while adhering to Euro 5 emissions standards, which include a 20-liter urea tank capacity. The market’s loyalty stems from the logistics principle that time is money; a truck sitting at a charger represents lost revenue, whereas diesel units operate continuously. Until battery density improves and infrastructure matures, diesel powertrains will unequivocally maintain their lead.

The <150 HP Engine Advantage: Tailored Power for Vietnam's Diverse Roadways

Commercial vehicles equipped with engines below 150 horsepower capture the highest market share at 54%, a dominance in the commercial vehicle market attuned to Vietnam's unique operating conditions. The market favors these moderate power outputs because they deliver sufficient torque for payloads under 6 tons without excessive fuel consumption. Engines ranging from 100 to 130 horsepower, such as the 130 Metric Horsepower Hyundai H150 or Kia K200 with 255 Newton-meters of torque, strike the ideal balance for stop-and-go city driving where speed limits are restricted to 50 or 60 kilometers per hour. Higher horsepower is largely inefficient for vehicles spending the majority of their time in congested traffic.

Cost efficiency drives this preference, as lower displacement engines—typically 2.5-liter—incur lower taxes and consume only 9 to 10 liters of fuel per 100 kilometers. In older districts with lane widths limited to 3.5 meters, agile vehicles like the Thaco Towner (95 horsepower) are paramount. These vehicles operate extended shifts of 16 to 20 hours daily with an average load factor between 70% and 80%, proving that the sub-150 horsepower range provides necessary pull without the overhead of a heavy-duty drivetrain.

Market Leadership in Tonnage: Sub-6-Ton Vehicles Master Vietnam's Urban Logistics

Vehicles with a carrying capacity of up to 6 tons dominate the Vietnam commercial vehicle market with an impressive 58.39% share, primarily driven by strict "truck ban" regulations in metropolises like Hanoi and Ho Chi Minh City. Vehicles under specific thresholds, such as 2.5 tons or 1.5 tons, enjoy operating exemptions that grant them access to city centers during daytime hours. Consequently, the estimated 5 million household businesses and delivery giants like Shopee rely on light trucks—ranging from the Suzuki Blind Van (580-kilogram payload) to the Thaco Towner 990 (990-kilogram capacity)—to fulfill over 2 billion annual e-commerce orders.

These sub-6-ton vehicles are the only viable option for daytime logistics. Regulations like HCMC’s peak-hour exemption for trucks under 2.5 tons and Hanoi’s leniency for those under 1.25 tons create an indispensable niche. While inner-city permits cost USD 50 to USD 100 annually, the flexibility afforded by vehicles with lengths under 5 meters and tight 4.5-meter turning radii is priceless in density zones exceeding 4,000 people per square kilometer. From FMCG to wet market supplies, these light tonnage vehicles remain the indispensable capillaries of the national supply chain.

Customize This Report + Validate with an Expert

Access only the sections you need—region-specific, company-level, or by use-case.

Includes a free consultation with a domain expert to help guide your decision.

Industrial Backbones: Heavy Trucks Secure Revenue Supremacy in Vietnam

While LCVs dominate unit sales in the Vietnam commercial vehicle market, heavy trucks command nearly 50.91% of the revenue in the Vietnam market, firmly establishing themselves as the financial backbone of the industrial economy. This revenue supremacy is intrinsically linked to the government's target of USD 36 billion for public infrastructure investment in 2025, including the North-South Expressway and the USD 67 billion High-Speed Rail project. High-value units from brands like Chenglong and Howo, often exceeding USD 50,000 per vehicle, drive substantial revenue despite lower volumes. Construction contractors and cross-border logistics firms heavily invest in these assets to handle the staggering freight volume that already exceeds 1.5 billion tons annually.

Although restricted to operating hours typically between 10 PM and 6 AM in major cities, heavy trucks are indispensable to Vietnam’s status as a global manufacturing hub. With export turnover to the US surpassing USD 100 billion and seaports handling over 700 million tons of cargo, efficient export logistics rely entirely on these giants. Even with annual logistics costs estimated at USD 40 billion and Chinese truck imports exceeding USD 1 billion in trade value, the essential function of heavy trucking in powering national development secures their unparalleled financial position.

To Understand More About this Research: Request A Free Sample

Recent Developments in Vietnam Commercial Vehicle Market

- THACO AUTO inaugurated advanced production technology at its THACO Bus Plant on December 4, 2025, launching new-generation THACO buses and trucks with enhanced efficiency, localization, and digital integration. Shineray topped Vietnam's mini-van commercial vehicle market with 30.1% share in H1 2025, leveraging full-chain localization via 25,000-unit capacity plants and new S1/529 models for urban logistics. Isuzu Vietnam introduced the D-MAX UTZ Frozen Box pickup in September 2025, tailored for urban cold-chain transport with cost-optimized flexibility.

- Hino Motors Vietnam opened its new 3S Vinh Thinh dealership on October 27, 2025, in Ho Chi Minh City, expanding sales, service, and genuine parts access to boost nationwide commercial vehicle support. THACO AUTO rolled out new-generation trucks nationwide in September 2025 via events with mobile repairs, advancing logistics with upgraded models amid export pushes to ASEAN/Middle East. These direct company announcements underscore localization, electrification prep, and network growth

Top Companies in the Vietnam Commercial Vehicle Market

- THACO (Truong Hai Auto Corporation)

- Isuzu Vietnam Co., Ltd.

- Ford Vietnam Limited

- Toyota Motor Vietnam

- Hyundai Motor Company

- UD Trucks Vietnam

- Mercedes-Benz Vietnam

- Mitsubishi Motors Vietnam

- AB Volvo

- Nissan Motor Co. Ltd.

- Honda Vietnam Co.

- Dongfeng Motor Corporation

- Other Prominent Players

Market Segmentation Overview

By Vehicle Class

- Light Commercial Vehicles (LCV)

- Medium Commercial Vehicles (MCV)

- Heavy Commercial Vehicles (HCV)

- Specialty Vehicles

By Vehicle Type

- Trucks

- Pickup Truck

- Box Truck

- Cargo Truck

- Semi-Truck / Tractor Trailer

- Track Truck / Tracked CV

- Fire Engine

- Delivery Truck

- Other Special Trucks

- Vans

- Cargo Van

- Passenger Van

- Step Van

- Other Vans

- Passenger Commercial Vehicles

- Passenger Cars

- Taxi

- Car Rental Vehicles

- Passenger Trolley

- RV-Type Transport Service

- Other Passenger CVs

- Delivery Vans / Urban Delivery Units

- Special Vehicles

- Utility / Municipal Vehicles

- Others

By Propulsion Type

- Internal Combustion Engine (ICE)

- Diesel

- Petrol/Gasoline

- Others

- Electric Commercial Vehicles

- BEV (Battery Electric Vehicles)

- HEV / PHEV (Hybrid & Plug-in Hybrid)

- FCEV (Fuel Cell Electric Vehicles - Hydrogen)

By Power Output

- <150 hp

- 150-250 hp

- 250-350 hp

- 350 hp (Heavy-Duty Long-Haul & Mining

By Weight/GVW Class

- Class 1-3: Up to 6 tons

- Class 4-6: 6-16 tons

- Class 7-8: 16+ tons

By Application/End Use

- Logistics & Transportation

- Last-mile Delivery

- Long-haul Transport

- Freight & Distribution

- Construction & Mining

- Dump Trucks

- Tippers

- Concrete Mixers

- Public Transport

- City Buses

- Intercity/Coach Buses

- Agriculture & Forestry

- Oil & Gas

- Municipal Services

- Tourism & Hospitality Transport

- Government & Defense

- Others

By Sales Channel

- OEM / New Vehicle Sales

- Aftermarket / Fleet Refurbishment

- Leasing & Rentals

By Region

- Northern Region

- North Central Region

- Central Region (South Central Coast)

- Central Highlands

- Southern Region

LOOKING FOR COMPREHENSIVE MARKET KNOWLEDGE? ENGAGE OUR EXPERT SPECIALISTS.

SPEAK TO AN ANALYST

.svg)

Features | Type of License | ||||

Data Book | Single User |   Multi User | Corporate | ||

| e-Access | ✓ | ✓ | ✓ | ✓ | |

User Sharing | 1 User Only | 1 User Only | Up to 7 Users | Unlimited User Access | |

⨉ | ⨉ | ⨉ | ✓ | ||

Free Customization | No Free Customization | Up To 30 hrs work | Up To 60 hrs work | Up To 80 hrs work | |

Deliverable |

| ⨉ | ✓ | ✓ | ✓ |

| ✓ | ⨉ | ✓ | ✓ | |

| ⨉ | ⨉ | ⨉ | ✓ | |

Analyst Support | 2-Months Analyst Support | 4-Months Analyst Support | 7-Months Analyst Support | One Year Analyst Support | |

Free Report update in next update cycle | ⨉ | ⨉ | ⨉ | ✓ | |

Free Industry Update (Within 180 days) | ⨉ | ⨉ | ⨉ | ✓ | |

Benefit | Up to 10% off on Post Purchase | Up to 20% off on Post Purchase | Up to 30% off on Post Purchase | Up to 40% off on Post Purchase | |