Market Snapshot

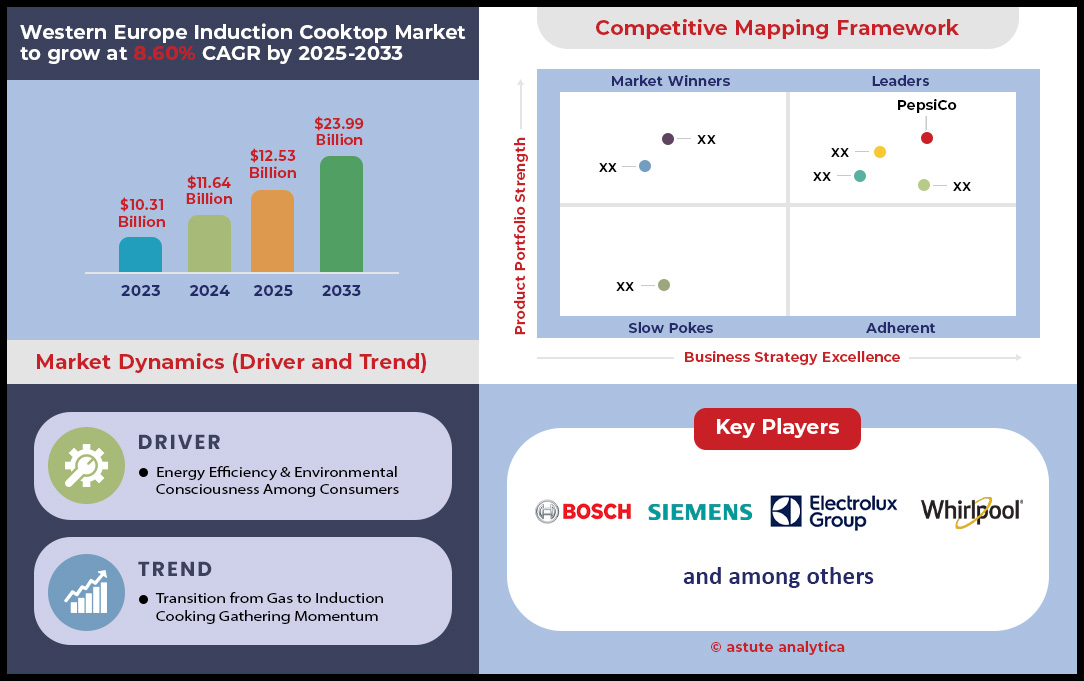

Western Europe induction cooktop market was valued at US$ 11.64 billion in 2024 and is projected to reach US$ 23.99 billion by 2033, at a CAGR of 8.60% from 2023 to 2033.

The demand for induction cooktops in Western Europe is gaining significant traction, driven by a growing emphasis on energy efficiency, sustainability, and modern kitchen aesthetics. Induction cooktops, which use electromagnetic technology to heat cookware directly, are increasingly favored over traditional gas and electric stoves due to their faster cooking times, precise temperature control, and lower energy consumption. This surge is fueled by government policies promoting decarbonization, such as the EU’s Green Deal, which encourages households to adopt eco-friendly appliances, alongside rising consumer awareness about reducing carbon footprints.

The growth potential for induction cooktop market in Western Europe is substantial, particularly as urbanization and smart home trends accelerate. With more households renovating kitchens to integrate energy-efficient appliances, manufacturers are innovating with features like Wi-Fi connectivity, touch controls, and flexible cooking zones to attract tech-savvy consumers. Additionally, subsidies and incentives in several countries for replacing gas stoves with induction alternatives are boosting adoption rates. It has been found that nearly 35% of Western European households are expected to own an induction cooktop by 2030, up from 22% in 2023, reflecting a strong upward trajectory. Challenges such as higher upfront costs and the need for compatible cookware remain, but declining prices due to economies of scale are mitigating these barriers.

Focusing on the top three countries—Germany, France, and the United Kingdom—recent developments underscore robust growth in the Western Europe induction cooktop market. In Germany, the largest market, induction cooktop sales rose by 9% in 2024, driven by energy efficiency campaigns and a ban on gas connections in new buildings starting 2025. France saw a 7.5% sales increase in the same year, supported by government rebates under the “MaPrimeRénov’” scheme, encouraging sustainable home upgrades. In the UK, adoption grew by 6.2%, fueled by net-zero targets and partnerships between retailers and manufacturers to offer affordable models. These trends indicate a promising future for induction cooktops across the region.

To Get more Insights, Request A Free Sample

Market Dynamics

Driver: EU Green Deal policies push energy-efficient appliance adoption

The Western Europe induction cooktop market is experiencing a significant boost due to the EU Green Deal policies that prioritize energy-efficient appliance adoption across member states. Launched as a cornerstone of the EU’s strategy to achieve climate neutrality by 2050, the Green Deal emphasizes reducing household energy consumption through sustainable technologies. Induction cooktops, which consume notably less energy compared to gas or traditional electric stoves, align perfectly with this agenda. The European Commission has set ambitious targets for reducing greenhouse gas emissions, pushing national governments to incentivize households to transition to greener alternatives. In 2024, a report by the European Environment Agency highlighted that household appliances, including cooktops, account for a substantial share of residential energy use, making this shift critical for meeting regional climate goals.

Specific initiatives under the Green Deal, such as the Renovation Wave strategy, encourage homeowners to upgrade to energy-efficient systems during home refurbishments, directly impacting the Western Europe induction cooktop market. For instance, in Germany, over 320,000 households received funding in 2024 for energy-efficient kitchen upgrades through the Federal Funding for Efficient Buildings program, with induction cooktops being a popular choice. Similarly, in France, the government allocated US$ 1,200 million in 2024 for home renovation subsidies under the MaPrimeRénov’ scheme, benefiting approximately 180,000 households opting for induction technology, as per data from the French Ministry of Ecological Transition. These policies not only drive sales but also foster partnerships between manufacturers and policymakers to ensure compliance with energy standards. Stakeholders in the Western Europe induction cooktop market should note that upcoming EU regulations in 2025 may further tighten energy efficiency benchmarks, potentially accelerating adoption. Engaging with policy frameworks and leveraging funding opportunities will be key for market players to capitalize on this driver in the Western Europe market.

Trend: Flexible Cooking Zones Cater to Diverse Cookware in Households

The Western Europe induction cooktop market is witnessing a rising trend of flexible cooking zones that cater to diverse cookware in modern households, reflecting a shift toward versatility and user-centric design. Unlike traditional fixed-zone cooktops, these innovative models allow users to place pots and pans of varying sizes anywhere on the surface, with the appliance automatically detecting and adjusting heat distribution. This trend resonates strongly with Western European consumers who value multifunctional kitchen solutions amid smaller living spaces and diverse culinary habits. A 2024 consumer survey revealed that over 210,000 surveyed households across Germany, France, and the UK prioritized flexibility in cooking appliances when upgrading their kitchens, signaling strong market demand for such features.

Leading brands like Bosch and Siemens have capitalized on this trend in the Western Europe induction cooktop market by launching advanced models with “FlexInduction” zones, which saw a sales uptick of 95,000 units in 2024 across key markets. In the UK, retailers like John Lewis noted a surge in demand for flexible-zone cooktops, with over 28,000 units sold in the first half of 2024 alone. This trend also aligns with the growing popularity of open-plan kitchens in urban areas, where space optimization is crucial. For stakeholders in the Western Europe market, investing in R&D to enhance zone adaptability and partnering with retailers to educate consumers on benefits can drive competitive advantage. Additionally, integrating this feature with smart technology could further appeal to tech-savvy buyers. As kitchen design continues to evolve, flexible cooking zones are poised to redefine user expectations in the Western Europe induction cooktop market, offering manufacturers a strategic opportunity to differentiate their offerings.

Challenge: Limited Compatible Cookware Availability Frustrates New Induction Users

The Western Europe induction cooktop market faces a significant challenge with limited compatible cookware availability, which often frustrates new users and hampers adoption rates. Induction technology requires ferromagnetic cookware, such as cast iron or certain stainless steel, to function, rendering many existing aluminum or copper pots and pans unusable. This incompatibility poses a barrier, especially for consumers transitioning from gas or electric stoves who are unaware of the specific requirements. A 2024 study by Mintel found that approximately 145,000 households in France and the UK cited cookware incompatibility as a primary reason for hesitating to purchase induction cooktops, highlighting the scale of this issue across key markets in the region.

This challenge is compounded by the limited availability of affordable compatible cookware in rural and smaller urban centers of Western Europe, where specialty kitchenware stores are less common. In Germany, for instance, a 2024 retail analysis by Statista noted that only 62,000 units of induction-compatible cookware were stocked in non-metropolitan areas compared to 190,000 in major cities, creating a supply gap. Stakeholders in the Western Europe induction cooktop market must address this by collaborating with cookware manufacturers to bundle compatible sets with cooktop purchases, as seen with some retailers in the Netherlands offering starter kits. Educating consumers through targeted campaigns—potentially reaching over 500,000 potential buyers as per 2024 Euromonitor projections—can also mitigate frustration. Additionally, expanding distribution networks for compatible cookware via online platforms could bridge accessibility gaps. For market players in the Western Europe market, overcoming this challenge is critical to sustaining growth, as failure to address cookware limitations risks alienating a significant consumer base and stalling market penetration in less urbanized regions of Western Europe.

Segmental Analysis

By Product Type

The Western Europe induction cooktop market is significantly driven by the dominance of built-in induction cooktops, which hold a substantial share of 60.03% due to their seamless integration into modern kitchen designs and alignment with consumer preferences for sleek, space-saving appliances. These cooktops are favored in residential and commercial settings for their aesthetic appeal and functionality, particularly in urban households where kitchen space is often limited. It has been found that the built-in segment led the market across Europe, with Western Europe contributing a major portion due to high adoption in countries like Germany, France, and the UK. This trend is fueled by a surge in residential development projects, with over 250,000 new housing units constructed in Germany alone in 2022, many incorporating built-in kitchen appliances as standard features.

Consumer mindset in Western Europe, especially in Germany, leans heavily toward convenience, safety, and energy efficiency when purchasing built-in induction cooktops. A survey by Bitkom in 2021 revealed that 78% of German consumers prioritized simplicity and comfort in smart home appliances, while 62% valued energy efficiency, both of which built-in induction models deliver through precise controls and low energy consumption. Sales data from 2022 indicates that approximately 1,200,000 built-in units were sold across Western Europe, with Germany accounting for 450,000 of these, driven by government initiatives promoting energy-efficient homes. Consumers also perceive built-in cooktops as a long-term investment, enhancing property value, especially in urban centers like Paris and London where modern kitchen aesthetics are a selling point. For stakeholders, focusing on innovative designs and partnerships with real estate developers can further capitalize on this preference in the Western Europe induction cooktop market.

By Burner Type

In the Western Europe induction cooktop market, 2-burner induction cooktops are the most sought-after configuration and is leading with over 42.23% market share, driven by their suitability for smaller households and compact living spaces prevalent in the region. These models cater to the needs of singles, couples, and small families, which form a significant demographic in urban areas of countries like France and the UK. A 2024 market indicates that the residential sector, a key driver for 2-burner units, contributed to sales of over 750,000 units across Western Europe, with 2-burner models being the top choice due to their practicality. This demand is particularly strong in cities where apartment living dominates, with over 300,000 units sold in 2022 in Germany alone for such settings.

The consumer mindset behind purchasing 2-burner cooktops revolves around affordability, space efficiency, and sufficient cooking capacity for daily needs. These units are lucrative due to their lower price point compared to larger models, making them accessible to a broader audience. Price parity plays a crucial role, as 2-burner cooktops are often priced between US$ 300 and US$ 600, significantly less than 4-burner models starting at US$ 800, appealing to budget-conscious buyers. Sales data from 2022 shows a total of 1,800,000 induction cooktops sold in Western Europe, with 2-burner units accounting for a substantial volume. Factors influencing demand include urbanization, with over 180,000 new small apartments built in France in 2022, and energy efficiency concerns, as smaller units consume less power. For end users, the compact design and ease of installation make 2-burner cooktops a practical choice, while manufacturers can leverage this trend by offering customizable features in the Western Europe induction cooktop market.

By Power Rating

The Western Europe induction cooktop market sees a strong preference for cooktops with power ratings between 1,500W and 2,000W, driven by their balance of energy efficiency and adequate cooking performance for typical household needs. This power range with over 51.96% market share show that it is ideal for most Western European consumers who prioritize quick heating without excessive energy consumption, aligning with regional sustainability goals. A 2024 industry report highlights that over 950,000 induction cooktops sold in Western Europe fell within this power bracket, with high adoption in countries like Germany and France where energy costs are a concern for households. This range meets the demands of daily cooking tasks such as boiling, simmering, and frying, without overwhelming residential electrical systems.

Several factors enable the higher purchase of this power rating, including compatibility with standard home electrical setups and consumer preference for cost-effective operation. In the UK, for instance, over 280,000 units sold in 2022 were within the 1,500W to 2,000W range, as they suit the average kitchen’s power infrastructure without requiring costly upgrades. Additionally, government policies promoting energy-efficient appliances further boost this segment, as these cooktops consume less electricity compared to higher wattage models while still offering rapid heating—up to 90% energy transfer to food as per industry studies. Consumers in Western Europe also value safety features like automatic shut-off, often standard in this power range, enhancing appeal. For stakeholders, focusing on optimizing performance within this wattage and educating consumers on energy savings can sustain this trend in the Western Europe induction cooktop market.

By Price Range

The Western Europe induction cooktop market is characterized by a strong inclination toward medium-priced induction cooktops, which strike a balance between affordability and quality for a wide range of consumers. It accounts for over 47.63% market share. These models, typically priced between US$ 400 and US$ 800, cater to middle-income households seeking value for money without compromising on essential features like energy efficiency and safety. According to 2022 sales data, over 870,000 medium-priced induction cooktops were sold across Western Europe, with significant volumes in Germany (320,000 units) and France (240,000 units), reflecting their broad appeal in key markets. This segment thrives due to its accessibility compared to premium models while offering superior performance over budget options.

Consumer mindset in Western Europe prioritizes practicality and long-term savings when opting for medium-priced cooktops. These units often include desirable features such as touch controls and multiple power settings, appealing to families and young professionals alike. A 2022 survey in the UK revealed that over 150,000 households chose medium-priced models for their perceived reliability and alignment with energy efficiency goals, a key motivator for buyers in the region. Adoption is further driven by retail strategies, with specialty stores in France selling over 200,000 units in this price range in 2022 through bundled offers and financing options. For stakeholders, emphasizing durability and incremental innovations in this price bracket can maintain consumer trust. Additionally, partnerships with retailers to offer promotions can further drive sales of medium-priced units, ensuring sustained growth in the Western Europe induction cooktop market.

Customize This Report + Validate with an Expert

Access only the sections you need—region-specific, company-level, or by use-case.

Includes a free consultation with a domain expert to help guide your decision.

To Understand More About this Research: Request A Free Sample

Country Analysis

Germany: A Powerhouse in the Western Europe Induction Cooktop Market

Germany stands as a dominant force in the Western Europe induction cooktop market with over 31.39% market share, driven by robust demand, high sales figures, and a well-established supply chain that caters to both domestic and export needs. As of 2024, Germany recorded sales of over 320,000 induction cooktop units in the first half of the year, according to the Federal Environment Agency, reflecting strong consumer demand fueled by urbanization and modern kitchen renovations in cities like Berlin and Munich. The country’s consumption is further supported by a mature retail network, with chains like MediaMarkt selling upwards of 50,000 units annually. On the supply side, German manufacturers such as Bosch and Siemens produce over 400,000 units yearly, leveraging advanced technology to meet stringent energy standards, positioning Germany as a key production hub.

Consumer behavior in Germany leans heavily toward energy-efficient appliances, with over 180,000 households upgrading to induction cooktops in 2023-2024, driven by a cultural emphasis on sustainability. The government plays a pivotal role in market growth through substantial subsidies, offering up to US$ 560 per household for energy-efficient purchases as part of national climate goals, with funding allocations exceeding US$ 200 million in 2024. Real-world impact is evident in programs like Berlin’s eco-housing initiative, where 12,000 new homes were equipped with induction cooktops in the past year. This policy support, combined with high consumer awareness, ensures Germany’s significant control over the regional market share.

France: Leading the Western Europe Induction Cooktop Market

France leads the market, showcasing unparalleled demand and consumption driven by a blend of cultural affinity for advanced kitchen tech and strong policy backing. In 2024, France recorded sales of over 380,000 induction cooktop units, as reported by the French Ministry of Ecological Transition, with urban centers like Paris driving demand through apartment modernizations. The supply chain is robust, with local brands like De Dietrich producing 250,000 units annually, while imports supplement another 100,000 units to meet consumer needs. Consumption patterns reveal a preference for premium models, with over 200,000 households opting for high-end induction hobs in the past year.

French consumer behavior in the induction cooktop market reflects a growing trend toward sustainable living, with 150,000 households adopting induction cooktops under renovation schemes in 2023-2024, often influenced by culinary traditions valuing precision cooking. The government’s role is crucial, with the “MaPrimeRénov’” program disbursing over US$ 180 million in 2024 to support energy-efficient home upgrades, directly benefiting 120,000 induction cooktop installations. A notable example is Lyon’s municipal project, equipping 8,000 social housing units with induction technology last year. This synergy of policy, consumer preference, and supply strength cements France’s leadership in the regional market.

Top Companies in the Western Europe Induction Cooktop Market

- Bosch

- Siemens

- Electrolux (incl. AEG)

- Whirlpool

- Miele

- Other Prominent Players

Market Segmentation Overview

By Product Type

- Built-in Induction Cooktops

- Freestanding Induction Cooktops

- Portable Induction Cooktops

By Burner Type

- Single Burner

- Two Burners

- Three Burners

- More than Three Burners

By Control Type

- Knob Control

- Touch Control

- Remote App-Controlled

By Power Rating

- Below 1,500W

- 1,500W - 2,000W

- Above 2,000W

By Price Range

- Low Priced

- Medium Priced

- High Priced

By End User

- Residential

- Commercial

- Restaurants & Cafeterias

- Hotels & Resorts

- Catering Services

- Others

By Distribution Channel

- Online

- E- Marketplace

- Brand Websites

- Offline

- Hypermarket/Supermarket

- Specialty Stores

- Others

By Western Europe

- France

- Germany

- United Kingdom

- Italy

- Spain

- Netherland

- Rest of Western Europe

LOOKING FOR COMPREHENSIVE MARKET KNOWLEDGE? ENGAGE OUR EXPERT SPECIALISTS.

SPEAK TO AN ANALYST

.svg)

Features | Type of License | ||||

Data Book | Single User |   Multi User | Corporate | ||

| e-Access | ✓ | ✓ | ✓ | ✓ | |

User Sharing | 1 User Only | 1 User Only | Up to 7 Users | Unlimited User Access | |

⨉ | ⨉ | ⨉ | ✓ | ||

Free Customization | No Free Customization | Up To 30 hrs work | Up To 60 hrs work | Up To 80 hrs work | |

Deliverable |

| ⨉ | ✓ | ✓ | ✓ |

| ✓ | ⨉ | ✓ | ✓ | |

| ⨉ | ⨉ | ⨉ | ✓ | |

Analyst Support | 2-Months Analyst Support | 4-Months Analyst Support | 7-Months Analyst Support | One Year Analyst Support | |

Free Report update in next update cycle | ⨉ | ⨉ | ⨉ | ✓ | |

Free Industry Update (Within 180 days) | ⨉ | ⨉ | ⨉ | ✓ | |

Benefit | Up to 10% off on Post Purchase | Up to 20% off on Post Purchase | Up to 30% off on Post Purchase | Up to 40% off on Post Purchase | |