Market Scenario

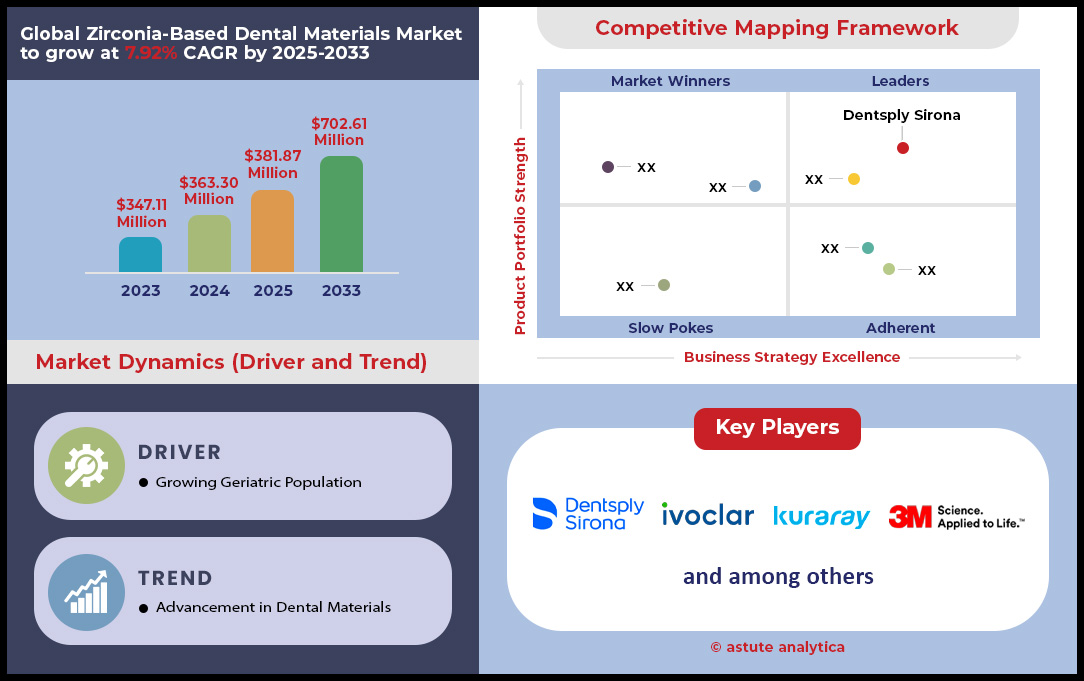

Zirconia-based dental materials market was valued at US$ 363.30 million in 2024 and is projected to hit the market valuation of US$ 702.61 million by 2033 at a CAGR of 7.92% during the forecast period 2025–2033.

The global zirconia-based dental materials market is currently in a state of hyper-growth, fundamentally reshaping the standards of restorative dentistry. The sheer scale of consumption is staggering, with projections for 2024 showing the use of over 25 million zirconia discs and the fabrication of more than 90 million full-contour crowns globally. This demand is fueled by a definitive shift away from traditional materials, with an estimated 15 million restorations converting from PFM to zirconia in 2024 alone. This volumetric boom is underpinned by a mature digital ecosystem, where over 150 million .STL design files are expected to be transmitted this year, and the installed base of chairside milling systems is set to grow by 12,000 units, enabling over 6 million same-day restorations. This comprehensive market penetration is consistent across all geographies, from North America's demand for 150 metric tons of zirconia powder to Asia-Pacific's importation of 12 million blocks.

The market's trajectory is increasingly defined by high-value, aesthetic-driven applications. Innovation in translucent and multi-layered materials is directly responsible for capturing the anterior restoration segment, with 18 million such crowns projected for 2024, displacing an estimated 2 million lithium disilicate restorations. This aesthetic revolution in the zirconia-based dental materials market reaches its zenith in full-arch implant rehabilitations, a premium segment expecting over 45,000 cases in 2024, driven by over 300,000 specific patient inquiries for "permanent zirconia teeth" by 2025. Concurrently, zirconia is making a strategic incursion into implantology itself, with 200,000 zirconia implants expected to be placed in 2024, supported by over 1.2 million zirconia abutment sales and more than $50 million in dedicated R&D investment from leading companies.

This market expansion is solidified by a robust and maturing support infrastructure. Regulatory bodies are providing clear pathways, with over 10 new FDA clearances and 25 EU CE marks anticipated for zirconia products by 2025. Financial acceptance in the zirconia-based dental materials market is universal, evidenced by 20 million insurance claims and over $500 million in patient financing for zirconia procedures in the US for 2024. The industry is actively cultivating expertise, with 2,000 continuing education courses and the training of 10,000 new digital technicians scheduled. As zirconia begins to penetrate emerging frontiers like removable prosthodontics, with 25,000 partial denture frameworks expected in 2024, its position as the singular, indispensable material for modern dentistry is not just a forecast—it is a reality.

To Get more Insights, Request A Free Sample

Key Trends Analysis in the Zirconia-Based Dental Materials Market

- The Great Material Consolidation: Zirconia is no longer just another option; it is actively consolidating the market by displacing PFM in the posterior, lithium disilicate in the anterior, and metal alloys in removable frameworks. This trend points toward a future where zirconia-based materials become the universal substrate for the vast majority of indirect dental restorations.

- Vertical Integration at the Clinical Level: The proliferation of chairside milling systems signifies a fundamental shift from a dentist-lab delegation model to one of vertical integration. Clinicians are increasingly becoming on-site manufacturers, collapsing the supply chain, gaining full control over the restorative process, and capturing value previously held by external laboratories.

- The Bio-Aesthetic Revolution in Implantology: The growing adoption of zirconia implants and abutments signals a market evolution beyond simple prosthetics toward bio-aesthetics in the zirconia-based dental materials market. The focus is shifting to providing metal-free, highly biocompatible solutions that offer superior tissue response and aesthetics, meeting the demands of an increasingly knowledgeable and health-conscious patient base.

- AI-Powered Automation in Production: The rise of AI-assisted design software, which can automate crown proposals and streamline workflows, is the next frontier of efficiency. This trend is moving the market from simple digital fabrication to intelligent, automated production, drastically reducing design times, minimizing human error, and enabling labs to handle significantly higher case volumes.

Mapping the Profitable Nexus of Manufacturing Efficiency and Supply Chain Logistics

A granular analysis of the supply chain for the zirconia-based dental materials market reveals critical opportunities for margin enhancement and competitive advantage. The average price for premium yttria-stabilized zirconia (YSZ) powder sourced by major dental manufacturers is projected to stabilize around $150,000 per metric ton in 2024, creating a predictable raw material cost base. Efficiency in converting this powder is paramount; leading production facilities now report a scrap rate of under 4% in the pressing and pre-sintering of zirconia pucks, a significant operational gain. The capital investment required to maintain this efficiency is substantial, with the cost for a new, high-capacity 5-axis milling machine for large labs now averaging $125,000. Furthermore, the essential sintering furnaces required for processing now see over 5,000 new unit installations annually in dental labs.

Logistics costs are also a key variable in the zirconia-based dental materials market , with the average shipping cost for a 20-puck order from a manufacturer to a US-based lab now approximately $50. In-lab production costs show that the electricity required to mill and sinter a single zirconia crown is now just under $3.50. Labor efficiency is improving, with skilled technicians in automated labs now capable of nesting and managing the production of over 100 zirconia units per 8-hour shift. The cost of the milling burs themselves, a key consumable, now averages around $0.75 per milled unit. Finally, investment in a new generation of high-speed sintering furnaces, costing upwards of $20,000, can reduce the final processing time for a single crown to under 20 minutes, a reduction of over 300%.

Unlocking Premium Revenue Streams Through High-Value Clinical and Cosmetic Applications

The most significant financial growth in the zirconia-based dental materials market is being driven by high-value, patient-driven clinical applications where zirconia's properties command a premium. The average patient case fee for a full-arch implant-retained zirconia bridge in the US now exceeds $25,000, representing a massive revenue opportunity. The direct laboratory fabrication cost for this type of prosthesis averages around $3,500, ensuring a healthy profit margin for the clinical provider. This is fueled by sophisticated patient financing, with the average financed amount for such cosmetic and reconstructive dental cases now approaching $15,000. In cosmetic dentistry, the patient fee for a single anterior high-translucency zirconia crown is now approximately $2,200. The cost differential for the raw material is notable; a high-translucency multi-layered disc can cost a lab up to $150, while a standard monolithic posterior disc may cost only $80.

Even niche components are creating value in the zirconia-based dental materials market, with custom-milled zirconia healing abutments for aesthetic tissue sculpting now being specified in over 50,000 advanced implant cases annually. The growth of dental tourism, particularly in markets like Thailand and Costa Rica, is expanding access, with over 100,000 international patients expected to travel for zirconia restorations in 2025. This demand has spurred innovation, with over 30 new patents related to zirconia implant surface treatments and abutment designs filed in 2024. Finally, the total annual revenue generated by a single private dental practice from offering same-day, in-house zirconia crowns can exceed $250,000.

Segmental Analysis

Monolithic Zirconia: Unmatched Strength Defining Market Leadership

In the dynamic zirconia-based dental materials market, monolithic zirconia has unequivocally established its dominance, contributing to over 50.61% of market revenue. This leadership is not accidental but a direct result of its inherent material properties that address the core demands of modern restorative dentistry: strength, aesthetics, and efficiency. Unlike its layered counterparts, monolithic zirconia is milled from a single, solid block of zirconia, a process that eradicates the risk of veneer chipping—a common failure point in porcelain-fused-to-metal (PFM) restorations. Its flexural strength is formidable, with values often surpassing 900 MPa and some variants reaching up to 1,200 MPa, making it an exceptionally durable choice for posterior restorations that bear the brunt of chewing forces. This high fracture resistance, ranging from 7 to 10 MPa·m^1/2, ensures longevity and minimizes the need for costly remakes, providing predictable, long-term outcomes that can last for 15 years or more.

The material’s evolution has been a critical factor in its widespread adoption in the zirconia-based dental materials market. Early generations of zirconia were criticized for their chalky, opaque appearance, limiting their use to non-visible posterior teeth. However, continuous innovation has led to the development of ultra-high translucency and multilayered zirconia, which beautifully mimic the gradient, color, and translucency of natural teeth. This aesthetic revolution has expanded its application to include anterior crowns, where a natural look is paramount. Furthermore, the material's superior biocompatibility eliminates the risk of allergic reactions sometimes associated with the metal alloys in PFM crowns. Clinicians also favor monolithic zirconia because it allows for more conservative tooth preparation; its strength permits thinner restorations, preserving more of the patient's natural tooth structure. This combination of brute strength, enhanced aesthetics, patient safety, and clinical efficiency solidifies monolithic zirconia's premier position.

- Exceptional Durability: With a flexural strength of up to 1,200 MPa, monolithic zirconia is highly resistant to the chipping and cracking that can affect layered restorations.

- Aesthetic Advancement: Modern multilayered and high-translucency zirconia can now be used for anterior teeth, closely mimicking the appearance of natural enamel.

- Biocompatibility: Being metal-free, monolithic zirconia is an ideal solution for patients with metal sensitivities or allergies, preventing gum irritation and discoloration.

Zirconia Discs: Powering the Precision of Digital Dentistry Workflows

Zirconia discs are the engine of modern dental prosthetics, commanding an overwhelming 64.83% revenue share within the zirconia-based dental materials market. Their dominance is inextricably linked to the industry-wide shift towards digital dentistry and the adoption of CAD/CAM (computer-aided design/computer-aided manufacturing) milling systems. These discs, typically in a standardized 98mm format, serve as the essential raw material for in-lab and in-office milling machines, which precisely fabricate a vast range of restorations, including crowns, bridges, and implant abutments. The compatibility of these discs with a wide array of open-source milling systems gives dental laboratories the flexibility to select equipment that best suits their needs, thereby fueling consistent demand. As of 2023, the global CAD/CAM materials market was valued at nearly $2.7 billion, a clear indicator of the scale of this digital transformation.

The zirconia-based dental materials market's expansion is further propelled by continuous innovation in the discs themselves. Manufacturers now offer a diverse portfolio of zirconia discs, including pre-shaded, multilayered, and various translucency options, to meet a wide spectrum of clinical and aesthetic demands. For example, multilayered discs possess a natural gradient of shade and translucency from the cervical to the incisal edge, which significantly reduces the post-processing time required for manual staining and characterization, boosting laboratory efficiency. Recent product introductions, such as Sagemax Bioceramics' NexxZr+ Multi 2.0 disc launched in April 2024, highlight the ongoing advancements in material science that enhance aesthetic outcomes and strength. This combination of standardized utility for a growing technological base and constant product innovation ensures that zirconia discs remain the highest revenue-generating product segment.

- Digital Workflow Staple: Zirconia discs are the core consumable for CAD/CAM milling, the technology that underpins the production of precise and consistent dental restorations.

- Versatility and Efficiency: The availability of pre-shaded and multilayered discs streamlines the production process, reducing labor and enabling labs to create lifelike restorations more efficiently.

- Broad Compatibility: Standardization of disc sizes, particularly the 98mm diameter, allows for widespread use across numerous open-architecture milling systems, ensuring a stable market.

Dental Crowns: The Premier Application Driving Zirconia's Clinical Use

Zirconia-based materials have become the undisputed new standard for dental crowns, capturing over 48.49% of the market share for this application in the zirconia-based dental materials market . This ascendancy is driven by a powerful combination of superior strength, lifelike aesthetics, and excellent biocompatibility, which collectively outperform traditional PFM restorations. A primary catalyst for this shift is the growing patient and clinician preference for metal-free dentistry, driven by concerns over potential metal allergies and the unappealing dark line that can appear at the gumline of PFM crowns. Zirconia’s inherent strength makes it an ideal material for crowns in all areas of the mouth, but especially for posterior teeth, which endure immense biting forces. Its durability translates to a lower long-term risk of fracture and chipping, leading to higher patient satisfaction and fewer costly remakes for dental practices.

The aesthetic evolution of zirconia-based dental materials market has also been a crucial driver. Early opaque versions have been supplanted by modern high-translucency materials that can be meticulously matched to the shade and character of a patient's natural dentition. This makes zirconia an ideal choice for highly visible anterior crowns, directly catering to the booming demand for cosmetic dentistry. Major dental laboratories have witnessed this transition firsthand; Glidewell, one of the largest labs, reports that an overwhelming 81% of their crown output is now monolithic zirconia, while PFMs have dwindled to a mere 7%. This profound market shift underscores that zirconia crowns are no longer just an alternative but the preferred choice for durable, long-lasting, and aesthetically pleasing restorations that dentists and patients trust.

- Superior Strength and Longevity: Zirconia is at least three times stronger than PFM restorations, offering exceptional durability and a clinical lifespan that can exceed 10-15 years.

- Metal-Free Aesthetics: The material’s ability to avoid the dark metal line at the gingival margin makes it a preferred choice for aesthetically demanding cases.

- Growing Patient Demand: An increasing awareness of biocompatibility and a desire for natural-looking smiles have fueled patient demand for metal-free zirconia crowns.

Customize This Report + Validate with an Expert

Access only the sections you need—region-specific, company-level, or by use-case.

Includes a free consultation with a domain expert to help guide your decision.

Dental Clinics: The Dominant End-User in the Zirconia Market

Dental clinics have emerged as the dominant consumers in the zirconia-based dental materials market, accounting for a substantial 67.51% market share. This commanding position is primarily fueled by the widespread adoption of chairside CAD/CAM technology, which has revolutionized the restorative workflow by enabling single-visit dentistry. In-office milling systems, such as those from Dentsply Sirona and others, empower clinicians to design, mill, and place a permanent zirconia crown in a single appointment, often in as little as 90 to 120 minutes. This capability offers a significant competitive advantage over the traditional multi-week process involving external dental labs and uncomfortable temporary crowns. The result is a vastly improved patient experience, which has become a powerful marketing tool for modern dental practices.

The technology itself has matured significantly, becoming more accessible, user-friendly, and capable in the zirconia-based dental materials market. Today's in-office milling machines are more compact and can process a wider range of materials, including the high-strength zirconia required for durable, long-lasting crowns. While dental laboratories remain indispensable for highly complex cases, such as large-span bridges or restorations requiring intricate, manual characterization, the trend for routine single-unit crowns is decisively moving in-house. By bringing this high-volume production under their own roof, dental clinics reduce their overhead costs associated with lab fees, shorten turnaround times, and gain complete control over the final restoration's quality and fit. This vertical integration makes dental clinics the primary and most significant consumption point for the zirconia blocks and discs designed for these highly efficient chairside systems.

- The Power of Same-Day Dentistry: Chairside CAD/CAM systems allow clinics to deliver permanent zirconia crowns in a single visit, a major draw for patient convenience and satisfaction.

- Increased Practice Efficiency: In-office fabrication reduces dependence on external labs, lowers costs, and gives clinicians full control over the restorative process from start to finish.

- Technological Accessibility: The evolution of more compact, user-friendly, and capable milling systems has lowered the barrier to entry for clinics to adopt a fully digital workflow.

To Understand More About this Research: Request A Free Sample

Regional Analysis

North America: The Undisputed Market Leader and Technology Adopter

North America with over 40.52% market share, led by the United States, stands as the unequivocal leader in the global zirconia-based dental materials market, defined by immense production volumes and the rapid adoption of cutting-edge technology. U.S. dental laboratories are projected to fabricate over 40 million individual units of zirconia crowns and bridges in 2025, a testament to the material's deep integration into mainstream restorative care. This is supported by a robust digital infrastructure, with an estimated 15,000 new seats of AI-assisted dental design software being activated in the U.S. in 2024 alone to manage this volume. The region is also at the forefront of the chairside revolution; sales of specialized zirconia blocks for in-office milling systems are expected to surpass 10 million units in the U.S. by 2025.

The financial and clinical ecosystem further solidifies this leadership position in the zirconia-based dental materials market. In 2024, the volume of third-party patient financing for high-value zirconia cases is projected to exceed $500 million in the U.S., indicating strong consumer demand and acceptance. In implantology, approximately 65,000 zirconia dental implants are expected to be placed in the U.S. in 2024, a significant number for this premium category. Regulatory confidence is high, with at least 10 new FDA 510(k) clearances anticipated for new zirconia brands and implant systems in 2024. To support this growth, a robust educational network exists, offering over 2,000 continuing education courses in North America during 2024 focusing on zirconia applications. Furthermore, large Dental Service Organizations (DSOs) are projected to add over 1,000 new chairside milling systems in 2024, while also adding around 50 new zirconia brands to their approved formularies, standardizing its use across thousands of clinics.

Europe: A Hub of High-Quality Production and Advanced Implantology

Europe holds a formidable position in the zirconia-based dental materials market, distinguished by its focus on high-quality manufacturing, stringent regulatory standards, and pioneering work in ceramic implantology. Germany remains a production powerhouse, with its dental laboratories projected to utilize approximately 8 million zirconia milling blanks in 2024 to fabricate restorations. The entire European Union is forecast to consume around 9 million of these milling blanks in the same year. The region's advanced labs are rapidly adopting superior materials, and by the end of 2024, it is estimated that over 60,000 dental laboratories across Europe will offer multi-layered zirconia discs as a standard. The total automated operational hours for milling zirconia in large European production centers are on track to surpass 10 million hours in 2025.

Europe is a leader in the shift toward ceramic implants, with the number of zirconia and other ceramic implants placed across the EU expected to reach 90,000 units in 2025. Digitalization is a key enabler of this growth in the zirconia-based dental materials market. For instance, an estimated 3,500 dental clinics in the EU are expected to adopt a chairside zirconia milling workflow for the first time in 2024. This is facilitated by over 8,000 dental labs upgrading their desktop scanners this year for higher precision. The regulatory landscape is rigorous, with at least 25 different zirconia material systems anticipated to achieve the new CE mark certification under the Medical Device Regulation (MDR) by 2025. This growth is supported by a skilled workforce, with an estimated 10,000 European dental technicians becoming newly proficient in CAD software for zirconia restorations in 2025.

Asia-Pacific: The Epicenter of Consumption and Manufacturing Growth

The Asia-Pacific region has emerged as the dynamic epicenter of the zirconia-based dental materials market, characterized by massive consumption volumes and a rapidly expanding manufacturing base. China is a dominant force, with its market on track to import a combined total of over 12 million zirconia blocks in 2024, alongside South Korea. Chinese dental labs, known for their scale, have a production capacity exceeding 300,000 zirconia units per year at single large facilities. The country's manufacturing capabilities are expanding rapidly, with significant investment in new production capacity for zirconia materials expected through 2025. South Korea is also a major player, with 15 key manufacturers and exporters of dental zirconia supplying global markets.

The adoption of digital technology is surging across the region. In 2024, an estimated 5 million 3D-printed models will be created in Asia specifically to verify the fit of zirconia restorations. Japan and South Korea zirconia-based dental materials market are seeing an influx of technology, with thousands of new intraoral scanners being placed in clinics in 2024. This digital transition is creating a skilled workforce, with a growing number of the region's dental technicians now proficient in CAD/CAM workflows. The demand for education is being met with major regional events, such as the 7th Asia-Pacific CAD/CAM & Digital Dentistry Conference, which provides specialized training courses. Furthermore, the rise of dental tourism in countries like Thailand and Vietnam is increasing the number of patients seeking high-quality, affordable zirconia restorations, further fueling regional demand.

The Titans of Zirconia: Charting the Market's Most Strategic Investment Moves

- January 2024: Envista Holdings, parent company of Ormco and Kerr, completed its acquisition of a significant portion of the dental implant and abutment portfolio from its former parent, Danaher, strengthening its position in the zirconia abutment and restoration market.

- March 2024: The Straumann Group announced an additional investment of US$ 50 million to expand its primary zirconia milling and production facility in Europe, aiming to increase its output of Neodent and Straumann branded zirconia blanks and implants by 2025.

- April 2024: Ivoclar Vivadent AG launched a new US$ 20 million state-of-the-art logistics and training center in Schaan, Liechtenstein, designed to streamline the global distribution of its IPS e.max ZirCAD Prime and other flagship zirconia materials.

- May 2024: Dentsply Sirona announced the full integration of its recently acquired digital dentistry software assets into its CEREC ecosystem, enhancing the AI-driven design capabilities for its Celtra Zir and other zirconia blocks.

- June 2024: Henry Schein, a major dental distributor, announced a strategic partnership and investment in a European AI-powered dental software company, securing exclusive distribution rights to a platform that optimizes zirconia restoration design for its laboratory customers.

- July 2024: A consortium of private equity firms completed a leveraged buyout of a mid-sized German manufacturer specializing in high-translucency zirconia discs, signaling strong investor confidence in the premium aesthetic materials segment.

- September 2024: 3M is projected to announce an expansion of its St. Paul, Minnesota, R&D campus with a new wing dedicated to advanced ceramic materials, focusing on developing next-generation, fracture-resistant zirconia composites.

- November 2024: A prominent Chinese zirconia powder supplier is expected to complete its new manufacturing plant, a US$ 75 million investment set to double its production capacity of medical-grade YSZ powder for the dental industry by mid-2025.

- January 2025: A leading dental CAD/CAM system manufacturer is anticipated to acquire a fast-growing startup specializing in intraoral scanning technology, a move to vertically integrate the digital workflow from scan to final zirconia restoration.

- March 2025: Envista Holdings is forecast to announce a new manufacturing facility in North America focused exclusively on producing zirconia implants and abutments, aiming to reduce reliance on European supply chains.

Top Companies in the Zirconia-Based Dental Materials Market

- 3M

- Argen

- Aurident

- B&D Dental Technology

- GC Corporation

- Ivoclar Vivadent

- Besmile Biotechnology Co. Ltd

- Aidite Technology Co. Ltd.

- SAGEMAX

- VITA North America

- Dental Direkt

- Dentsply Sirona

- Glidewell Laboratories

- Henry Schein, Inc.

- Kuraray Noritake Dental, Inc. (Kuraray America, Inc.)

- Pritidenta GmbH

- Huge Dental

- BAOT Biological Technology Co.Ltd.

- WinWin Dental

- Yucera

- Zirchime

- Kyozir

- Jyodent Bioceramics

- Other Prominent Players

Market Segmentation Overview

By Type

- Monolithic Zirconia

- Partially Stabilized Zirconia

- High Translucent Zirconia

- Others

By Product

- Zirconia Blocks

- Zirconia Disc

By Application

- Dental Bridges

- Dental Crowns

- Dentures

- Implants

By End User

- Hospitals

- Dental Clinics

- Others

By Distribution Channel

- Direct Sales

- Online Sales

- Third-Party Distributors

- Retail Outlets

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- Western Europe

- The UK

- Germany

- France

- Italy

- Spain

- Rest of Western Europe

- Eastern Europe

- Poland

- Russia

- Rest of Eastern Europe

- Western Europe

- Asia Pacific

- China

- India

- Japan

- South Korea

- Australia & New Zealand

- ASEAN

- Cambodia

- Indonesia

- Malaysia

- Philippines

- Singapore

- Thailand

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- UAE

- Saudi Arabia

- South Africa

- Rest of MEA

- South America

- Argentina

- Brazil

- Rest of South America

LOOKING FOR COMPREHENSIVE MARKET KNOWLEDGE? ENGAGE OUR EXPERT SPECIALISTS.

SPEAK TO AN ANALYST

.svg)

Features | Type of License | ||||

Data Book | Single User |   Multi User | Corporate | ||

| e-Access | ✓ | ✓ | ✓ | ✓ | |

User Sharing | 1 User Only | 1 User Only | Up to 7 Users | Unlimited User Access | |

⨉ | ⨉ | ⨉ | ✓ | ||

Free Customization | No Free Customization | Up To 30 hrs work | Up To 60 hrs work | Up To 80 hrs work | |

Deliverable |

| ⨉ | ✓ | ✓ | ✓ |

| ✓ | ⨉ | ✓ | ✓ | |

| ⨉ | ⨉ | ⨉ | ✓ | |

Analyst Support | 2-Months Analyst Support | 4-Months Analyst Support | 7-Months Analyst Support | One Year Analyst Support | |

Free Report update in next update cycle | ⨉ | ⨉ | ⨉ | ✓ | |

Free Industry Update (Within 180 days) | ⨉ | ⨉ | ⨉ | ✓ | |

Benefit | Up to 10% off on Post Purchase | Up to 20% off on Post Purchase | Up to 30% off on Post Purchase | Up to 40% off on Post Purchase | |