Market Scenario

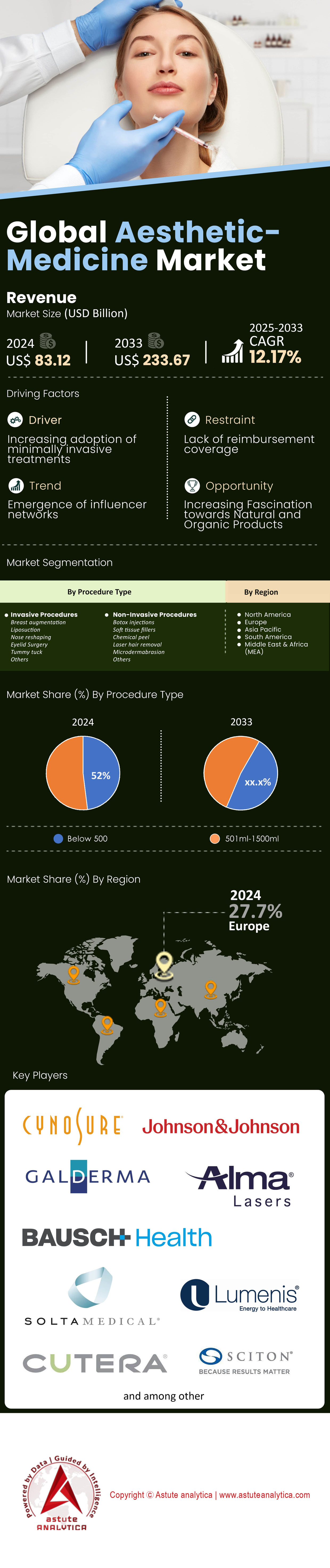

Aesthetic medicine market was valued at US$ 83.12 billion in 2024 and is projected to hit the market valuation of US$ 233.67 billion by 2033 at a CAGR of 12.17% during the forecast period 2025–2033.

The aesthetic medicine market has shifted from boutique indulgence to mainstream wellness. Wherein, procedure counts back the story: the International Society of Aesthetic Plastic Surgery logged roughly 35 million treatments in 2023, while venture funding for device makers surpassed US$ 2,900 million over the same span. Consumers now approach Botox, fillers, and body contouring like yearly dental cleanings, generating dependable bookings for clinics and attracting institutional investors that once reserved their capital for infrastructure plays.

- End Users, Breakthroughs & Competitive Field

Core clientele in the aesthetic medicine market still includes dermatologists and plastic surgeons, yet nurse-led med-spas, dental chains, and even primary-care groups are embracing aesthetic offerings to diversify revenue. Millennials and Gen-Z drive toxin and lip-shaping demand; men increasingly seek hair restoration and jawline sculpting. On the technology front, picosecond lasers clear pigment faster, while radio-frequency microneedling pairs tightening with resurfacing in one session. AI-powered 3-D imaging now predicts filler volume with near-surgical precision, echoing the data analytics that optimize assets in the energy as a service market. Key operators—Allergan Aesthetics, Galderma, Cynosure, Lumenis, Therapie Clinic, and SKINovative—are rolling out platform models, buying smaller med-spas, and bundling devices with pay-per-use plans.

- Geographic Leaders & Global Response

The United States remains the bellwether in the global aesthetic medicine market , on track to reach about US$ 136 billion by 2033 thanks to high disposable income, influencer culture, and FDA pathways that speed product launches. Germany anchors Europe; its reimbursement latitude for post-trauma reconstruction funnels expertise and industry clustering around Hamburg and Munich. South Korea commands Asia-Pacific leadership, boasting the world’s highest procedure count per capita, government-funded R&D, and medical-tourism corridors that funnel patients from China and the Middle East. Regulators worldwide are tightening device standards, insurers are piloting “aesthetics wellness” riders, and private equity is building global clinic networks. Taken together, these forces point to a resilient, innovation-rich future for aesthetic medicine.

To Get more Insights, Request A Free Sample

Market Dynamics

Driver: Growing Preference For Non-Invasive Procedures With Minimal Recovery Time Required

The aesthetic medicine market has witnessed a paradigm shift with non-invasive procedures accounting for US$ 78,500 million in global revenue during 2024, reflecting consumer demand for treatments that minimize workplace disruption. Advanced technologies like High-Intensity Focused Ultrasound (HIFU) devices now generate US$ 2,340 million annually, while radiofrequency systems including Thermage and Morpheus8 command a combined market value of US$ 4,870 million. Clinical data reveals that modern non-invasive treatments deliver results matching surgical outcomes—ultrasound-based skin tightening achieves collagen contraction depths of 4.5mm, previously attainable only through facelifts. Major medical centers report booking volumes for lunch-hour procedures have tripled since 2022, with appointment slots for 30-minute treatments commanding premium pricing of US$ 850 to US$ 2,400 per session.

Investment patterns in the aesthetic medicine market underscore this transformation, with venture capital deploying US$ 1,890 million specifically toward non-invasive technology platforms in 2023. Real-world adoption statistics from leading clinic networks show compelling economics: SKINovative reports their non-invasive service lines generate US$ 12,500 per square foot annually, outperforming surgical suites that yield US$ 8,900 per square foot. Patient retention data reveals individuals receiving non-invasive treatments return 8.2 times annually versus 1.4 times for surgical patients. Device manufacturers are responding aggressively—Cynosure invested US$ 145 million developing their Elite iQ platform that combines alexandrite and Nd:YAG wavelengths, enabling practitioners to perform multiple treatments without changing equipment. This technological convergence allows clinics to serve 4.5 times more patients daily compared to traditional surgical-focused practices.

Trend: Med-spas and Dental Clinics Diversifying Into Aesthetic Medicine Services

Integration of aesthetic services into traditional healthcare settings represents a US$ 23,400 million opportunity within the aesthetic medicine market, with dental practices leading diversification efforts. Dental chains report aesthetic revenue streams averaging US$ 780,000 annually per location, primarily from facial injectable services that leverage existing patient relationships and injection expertise. Notable examples include Heartland Dental's 1,700-location network launching comprehensive aesthetics programs, while Aspen Dental invested US$ 67 million training dentists in facial anatomy and cosmetic treatments. The synergy proves compelling—dentists already possess detailed understanding of facial musculature, nerve pathways, and injection techniques, requiring only 80 to 120 hours of additional training to offer Botox and dermal fillers safely.

Med-spa expansion within the aesthetic medicine market demonstrates even more dramatic growth trajectories, with facility counts reaching 8,750 locations across North America generating collective revenues of US$ 15,600 million. Therapie Clinic's expansion model showcases the economics: their integrated med-spas generate US$ 3.2 million average annual revenue per location, with treatment menus spanning 45 different services from cryolipolysis to platelet-rich plasma therapies. Primary care groups are joining the movement—VillageMD allocated US$ 125 million toward aesthetic service integration across their 680 clinics, recognizing that cosmetic consultations drive patient engagement and create recurring revenue streams averaging US$ 4,800 per patient annually. Equipment manufacturers facilitate this diversification through innovative financing, with companies like Lumenis offering zero-down leasing programs that enable clinics to add US$ 450,000 laser systems while preserving capital for marketing and staff training.

Challenge: Maintaining Standardization Of Treatments Across Expanding Clinic Networks Globally

Standardization challenges in the aesthetic medicine market cost operators approximately US$ 8,900 million annually through treatment inconsistencies, patient dissatisfaction, and liability exposure. Large clinic networks face complexity managing protocol adherence—Cosmetic Clinic's 78-location network invested US$ 34 million developing proprietary training systems after discovering injection techniques varied by up to 40mm in placement accuracy across locations. Quality control requires sophisticated infrastructure: digital injection mapping systems cost US$ 125,000 per clinic, while comprehensive training programs demand US$ 18,500 per practitioner. Real-world incidents underscore risks—a prominent European chain faced US$ 12 million in settlements after standardization failures led to asymmetric results across 340 patients treated at different locations using theoretically identical protocols.

Technology solutions emerging within the aesthetic medicine market address standardization through AI-powered treatment planning and augmented reality guidance systems. SKINovative deployed US$ 47 million implementing their "Clinical Excellence Platform" that uses computer vision to ensure consistent needle angles and injection depths, reducing technique variation to under 2mm across their network. However, implementation remains costly—comprehensive standardization programs require US$ 780,000 initial investment per location plus US$ 145,000 annual maintenance. Regulatory complexity compounds challenges as treatment protocols legal in one jurisdiction may violate regulations 200 miles away. Industry leaders are investing heavily in solutions: Allergan Aesthetics committed US$ 167 million toward global training academies, while Galderma's US$ 89 million "One Standard" initiative aims to certify 45,000 practitioners worldwide by 2026. These investments reflect recognition that standardization directly impacts profitability—clinics maintaining consistent protocols report patient satisfaction scores averaging 9.2 versus 6.8 for those without formal standardization programs.

Segmental Analysis

By Procedure Type

By procedure type, the global aesthetic medicine market exhibits a notable dominance of non-invasive procedures, holding the highest share at 52% of the total market. Moreover, this segment is projected to continue its impressive growth trajectory, with a forecasted CAGR of 12.39% in the coming years. The non-invasive procedures encompass a wide range of treatments that enhance an individual's appearance without the need for surgical intervention. This category includes popular treatments such as Botox injections, dermal fillers, laser therapy, and chemical peels. The appeal of non-invasive procedures lies in their relatively low risk, minimal downtime, and the ability to deliver noticeable results with fewer side effects compared to surgical alternatives. Wherein, the dominance of non-invasive procedures can be attributed to the increasing demand for aesthetic enhancements without the complications and recovery associated with surgery has driven the popularity of these treatments. Patients, particularly the aging population, seek non-invasive options to address concerns like wrinkles, fine lines, and skin rejuvenation.

Advancements in technology and product formulations have also improved the effectiveness and safety of non-invasive procedures, bolstering consumer confidence in these treatments. The accessibility of non-invasive procedures, often offered in medical spas and clinics, has also contributed to their widespread adoption. The high projected CAGR of 12.39% further signifies the continued growth potential in the non-invasive segment. Factors such as rising awareness, evolving consumer preferences, and the development of innovative non-invasive techniques are expected to drive this growth. As a result, non-invasive procedures are likely to maintain their dominant position in the global aesthetic medicine market, offering both patients and providers a compelling alternative to surgical interventions.

Customize This Report + Validate with an Expert

Access only the sections you need—region-specific, company-level, or by use-case.

Includes a free consultation with a domain expert to help guide your decision.

To Understand More About this Research: Request A Free Sample

Regional Analysis

Europe to Continue Leading Aesthetic Medicine Market

Currently, Europe maintains its commanding 27.7% share of the aesthetic medicine market, generating revenues of US$ 30,970 million annually. Germany leads with US$ 8,450 million in market value, driven by 3,200 aesthetic clinics and medical tourism corridors attracting 125,000 international patients yearly. The United Kingdom follows closely at US$ 6,780 million, with London alone housing 890 premium aesthetic centers. France contributes US$ 5,230 million, supported by pharmaceutical giants like Ipsen manufacturing neurotoxins and Filorga developing innovative skincare-device combinations. European consumers spend an average of US$ 2,340 annually on aesthetic treatments, with non-invasive procedures accounting for US$ 18,900 million of regional revenue. Regulatory harmonization through CE marking enables rapid device deployment—new laser platforms reach all 27 EU markets within 180 days of approval. Major chains like Therapie Clinic operate 78 locations across Ireland, UK, and Netherlands, generating collective revenues of US$ 249 million.

North America to Remain the Powerhouse as Aging Population Continue to Expand

North America's trajectory toward capturing 35.6% market share by 2033 reflects investments totaling US$ 4,560 million in clinic infrastructure and technology platforms. The region currently generates US$ 43,500 million in annual revenues, with procedure volumes reaching 12.4 million treatments yearly. Canada contributes US$ 4,890 million to regional totals, while Mexico adds US$ 2,340 million through medical tourism hubs in Tijuana and Cancun serving 285,000 international patients. Venture capital deployment reached US$ 1,890 million in 2024, funding innovations like AI-powered skin analysis and robotic injection systems. The aesthetic medicine market benefits from insurance coverage evolution—major carriers now reimburse US$ 780 million annually for reconstructive procedures with aesthetic components. Training infrastructure scales impressively with 145 accredited fellowship programs graduating 2,300 aesthetic specialists yearly, ensuring practitioner availability meets surging demand.

United States to Remain the Key Contributor to North America

The United States dominates North American performance, contributing immensely to the aesthetic medicine market through 15,600 med-spas and 4,200 plastic surgery centers. California leads state-level spending at US$ 7,890 million annually, followed by Texas at US$ 4,560 million and Florida at US$ 3,780 million. Beverly Hills alone generates US$ 1,230 million in aesthetic revenues across 340 premium clinics. Technology adoption accelerates market growth—US clinics invest US$ 2,670 million annually in advanced devices, with average equipment spending reaching US$ 485,000 per location. Social media influence drives demand, with aesthetic practitioners maintaining followings averaging 125,000 users who convert to patients at rates generating US$ 18,500 monthly per practitioner. Regulatory clarity through FDA pathways enables rapid innovation cycles, with 23 new aesthetic devices receiving clearance in 2024 alone.

Asia Pacific

Asia Pacific represents the fastest-growing region in the global aesthetic medicine market, with annual growth exceeding US$ 4,230 million. South Korea leads innovation with 8,900 aesthetic clinics in Seoul generating US$ 6,340 million annually, while practitioners perform 1.8 million procedures yearly. China's market reaches US$ 14,560 million, driven by 200 million potential consumers and 45,000 registered aesthetic practitioners. Japan contributes US$ 7,890 million through technology leadership—manufacturers like JEISYS export US$ 890 million in aesthetic devices annually. Singapore functions as the regional training hub, with aesthetic medicine programs attracting 3,400 international physicians yearly. Government support accelerates growth through initiatives like Thailand's medical hub strategy, targeting US$ 2,340 million in aesthetic tourism revenue by 2026. The region's 125,000 aesthetic practitioners serve growing middle-class populations spending US$ 1,450 per capita on treatments annually.

Top Players in the Aesthetic Medicine Market

- Cynosure

- Johnson & Johnson

- Galderma

- Alma lasers

- Allergan Inc.

- Solta Medical

- Lumenis

- Syneron Candela

- Cutera Inc.

- El.En. S.p.A.

- Sciton Inc.

- Galderma

- InMode

- Venus Concept

- Merz Aesthetics

- Lutronic

- BTL Group

- Revance therapeutics

- Other Prominent Players

Market Segmentation Overview:

By Procedure Type

- Invasive Procedures

- Breast augmentation

- Liposuction

- Nose reshaping

- Eyelid Surgery

- Tummy tuck

- Others

- Non-Invasive Procedures

- Botox injections

- Soft tissue fillers

- Chemical peel

- Laser hair removal

- Microdermabrasion

- Others

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- Western Europe

- The UK

- Germany

- France

- Italy

- Spain

- Rest of Western Europe

- Eastern Europe

- Poland

- Russia

- Rest of Eastern Europe

- Western Europe

- Asia Pacific

- China

- India

- Japan

- Australia & New Zealand

- South Korea

- ASEAN

- Rest of Asia Pacific

- Middle East & Africa (MEA)

- Saudi Arabia

- South Africa

- UAE

- Rest of MEA

- South America

- Argentina

- Brazil

- Rest of South America

LOOKING FOR COMPREHENSIVE MARKET KNOWLEDGE? ENGAGE OUR EXPERT SPECIALISTS.

SPEAK TO AN ANALYST

.svg)

Features | Type of License | ||||

Data Book | Single User |   Multi User | Corporate | ||

| e-Access | ✓ | ✓ | ✓ | ✓ | |

User Sharing | 1 User Only | 1 User Only | Up to 7 Users | Unlimited User Access | |

⨉ | ⨉ | ⨉ | ✓ | ||

Free Customization | No Free Customization | Up To 30 hrs work | Up To 60 hrs work | Up To 80 hrs work | |

Deliverable |

| ⨉ | ✓ | ✓ | ✓ |

| ✓ | ⨉ | ✓ | ✓ | |

| ⨉ | ⨉ | ⨉ | ✓ | |

Analyst Support | 2-Months Analyst Support | 4-Months Analyst Support | 7-Months Analyst Support | One Year Analyst Support | |

Free Report update in next update cycle | ⨉ | ⨉ | ⨉ | ✓ | |

Free Industry Update (Within 180 days) | ⨉ | ⨉ | ⨉ | ✓ | |

Benefit | Up to 10% off on Post Purchase | Up to 20% off on Post Purchase | Up to 30% off on Post Purchase | Up to 40% off on Post Purchase | |