Market Scenario

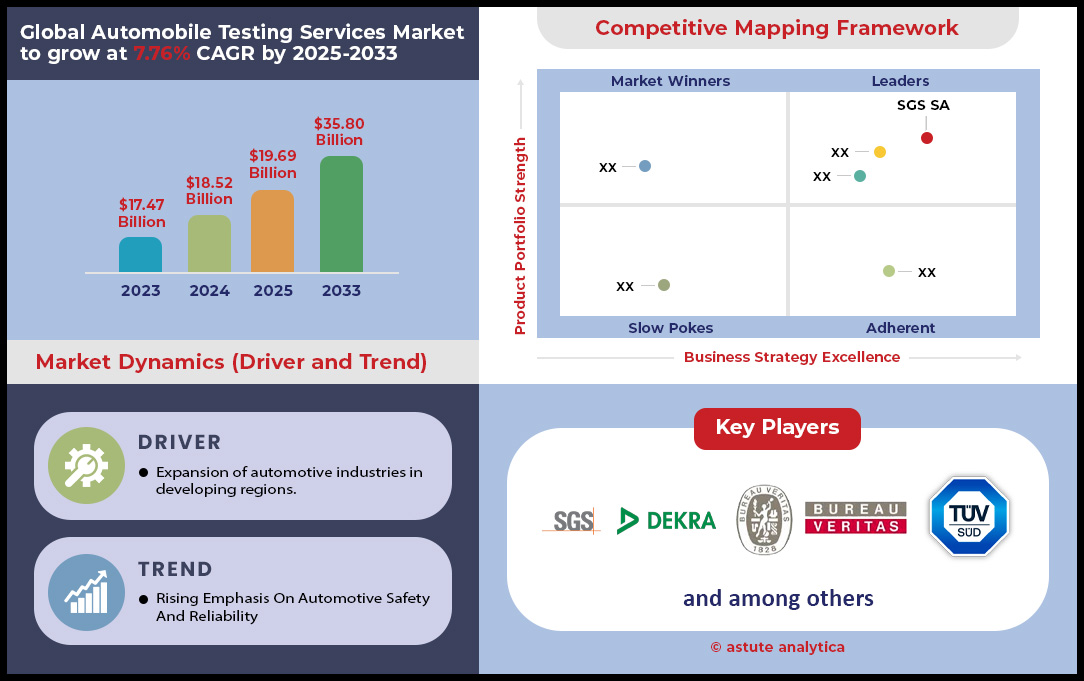

Automobile testing services market was valued at US$ 18.52 billion in 2024 and is projected to hit the market valuation of US$ 35.80 billion by 2033 at a CAGR of 7.76% during the forecast period 2025–2033.

Key Findings in Global Automobile Testing Services Market

- Based on component, Service segment holds highest share of 57.13%.

- Based on vehicle type, Passenger Vehicles segment holds highest share 63.82%.

- Based on vehicle component, Vehicle segment holds highest share 42.55%.

- Based on propulsion type, Internal Combustion Engine (ICE) Vehicles segment holds highest share 62.22%.

- Based on business model, Fee-for-Service Testing segment holds highest share 40.54%.

- Based on location, Off-Site segment holds highest share 63.26%

- Based on testing duration, Mid-cycle (Feature validation, 3-6 months) segment holds highest share 44.81%.

- Based on End Users, OEMs (Vehicle Manufacturers) segment holds highest share 40.38%.

- Europe with 38.17% of the market share projected to continue leading the market.

- Global automobile testing services market is set to reach US$ 35.80 billion by 2033.

The demand shaping the global automobile testing services market is tangible and accelerating, driven by massive capital investments in physical infrastructure. Stakeholders are witnessing the construction of advanced facilities, such as UTAC's upgraded 85,000 sq ft electrification center and Toyota's new $50 million EV battery laboratory opening in 2025. Testing providers are expanding capabilities to meet new technical requirements; for instance, UTAC's new e-motor test cells can now reach speeds of 25,000 RPM. New regulations, like Europe's 2025 mandate for EVs to retain 80% battery capacity after 100,000 km, create a non-negotiable need for long-term durability validation. Schaeffler's construction of a 130,000-square-foot plant for electric drivetrains further underscores the manufacturing shift that precedes testing demand.

Simultaneously, the growth of the software-defined vehicle is creating an immense, non-physical testing frontier. A premium vehicle in 2024 contains over 100 million lines of code, a figure that introduces profound complexity. The discovery of a record-high 530 cybersecurity vulnerabilities in 2024 highlights the critical need for robust digital validation services. In the autonomous vehicle space, the 9.06 million autonomous miles driven in California and the 28,800 driver disengagements recorded in 2024 reflect the sheer scale and rigor of current testing protocols. Virtual testing has become essential, with Waymo's fleet running 20 million simulated miles daily and AVL's simulators processing 10,000 ADAS scenarios per hour.

Regulatory pressures are a foundational driver for the automobile testing services market, compelling continuous and evolving validation. The upcoming Euro 7 standard, which will measure particulate emissions down to 10 nanometers, and its new 3mg/km brake dust limit for EVs, create entirely new testing requirements. Safety protocols are also becoming more stringent, with ANCAP's 2025 side impact test speed increasing to 60km/h. Furthermore, the emergence of alternative fuels, demonstrated by AVL's hydrogen engine achieving 150 kW per liter, introduces another specialized testing vertical. Even environmental durability testing is advancing, as seen with UTAC's "Sun Bench" that uses 700 infrared lamps to simulate extreme solar conditions.

To Get more Insights, Request A Free Sample

Three Shifts in Automobile Testing Services Market

- Generative AI and Digital Twins are Creating Hyper-Realistic Virtual Proving Grounds

The future of testing is increasingly virtual. Companies are leveraging generative AI to create synthetic sensor data—from cameras to LiDAR—to test autonomous systems in millions of simulated scenarios that are too dangerous or rare to replicate physically. This trend is accelerating development, with some manufacturers reporting a 43% reduction in overall test cycle times and a 60% acceleration in test case generation. By 2025, digital twins, which are precise virtual replicas of physical vehicles, will allow for continuous, real-time monitoring and analysis, dramatically reducing the reliance on costly physical prototypes.

- EV Thermal Management is Becoming a Critical and Complex Testing Discipline

As electric vehicles push the boundaries of battery capacity and charging speeds, thermal management has become a paramount safety and performance concern in the automobile testing services market. Testing is moving beyond simple temperature monitoring to validating complex liquid-cooling circuits, integrated heat pump systems, and the performance of advanced materials like silver-sintered die-attaches for power electronics. With EV junction temperatures expected to surpass 175°C, ensuring the reliability of every component under extreme thermal stress is a major growth area for specialized testing services.

- Data Localization and In-Country Testing Mandates are Reshaping Global Strategies

Emerging automotive markets are increasingly implementing regulations that require vehicle testing to be conducted within their own borders. Countries are establishing their own NCAP (New Car Assessment Program) standards and mandating local validation for emissions and safety systems. For instance, Japan will fully implement on-board diagnostic (OBD) testing for new imported vehicles from October 2025, requiring specific, in-country compliance. This trend forces global OEMs and testing providers to invest in local facilities and expertise, shifting the market away from centralized testing hubs.

Advanced Materials Drive a New Paradigm in Physical Durability Testing

A powerful demand driver for the automobile testing services market stems from the industry's aggressive adoption of advanced materials. The transition to electric vehicles and stringent efficiency mandates have ignited a revolution in material science, compelling a complete overhaul of physical and durability testing protocols. Lightweighting is no longer a luxury but a necessity, leading to the integration of complex composites, alloys, and polymers that require specialized validation. The average luxury EV in 2024 now incorporates over 150 kilograms of advanced composites to offset battery weight. In critical safety applications, new grades of advanced high-strength steel are being tested in 2025 to withstand tensile strengths exceeding 1,500 megapascals. The methods for joining these dissimilar materials are also under intense scrutiny. New structural adhesives must now prove they can endure shear forces of 25 megapascals to ensure body rigidity.

Furthermore, EV-specific components demand extreme performance validation. Battery enclosures, often made from multi-material composites, must now pass tests simulating thermal runaway events that reach 800 degrees Celsius for a minimum of 5 minutes. The thermoplastics used in body panels are subjected to over 2,000 hours of accelerated weathering tests to validate color and gloss stability. Even smaller components are tested rigorously; new carbon fiber reinforced plastic components are validated to absorb 50 kilojoules of impact energy in low-speed crash tests. The glass-fiber composites used in suspension systems undergo 1 million cycles of fatigue testing. To ensure longevity, polymer components are tested for fluid resistance against at least 15 different automotive chemicals. Finally, advanced coatings applied to lightweight alloys must pass 1,000 hours of continuous salt spray testing without corrosion.

High-Voltage EV Architectures Demand Radical New Component-Level Testing Protocols

The rapid shift toward high-voltage electric vehicle architectures is creating a surge in demand for highly specialized component-level testing services in the global automobile testing services market. The move from legacy 400-volt systems to new 800-volt platforms has fundamentally altered the electrical stresses on every part of the powertrain, necessitating a new generation of validation equipment and procedures. These platforms require insulation testing that can withstand up to 4,000 volts DC to prevent catastrophic failures. The heart of these systems, the silicon carbide (SiC) inverters, are now validated to operate at sustained switching frequencies of 20 kilohertz, creating unique challenges for electromagnetic compatibility testing. The e-motors themselves are spinning faster than ever, with new performance models requiring validation for continuous operation at 22,000 revolutions per minute.

The ecosystem of supporting components also requires more rigorous testing. High-power 22-kilowatt AC onboard chargers must now successfully endure over 1,000 hours of endurance testing at full thermal and electrical load. Battery Management Systems (BMS) are becoming more sophisticated in the automobile testing services market, with 2025 requirements demanding a response time of under 250 microseconds to isolate a fault condition. The DC-DC converters that power the vehicle's low-voltage systems are tested to achieve a power conversion efficiency of 97 percent to minimize energy loss. To ensure safety from electrical breakdown, critical busbars and connectors undergo partial discharge testing at voltages exceeding 1,500 volts. Power modules containing IGBTs are subjected to 100,000 thermal cycles. Even the charging inlets are tested to withstand 10,000 mating cycles while carrying their maximum rated current, ensuring long-term reliability for the end-user.

Segmental Analysis

Passenger Vehicle Testing Ensures Safety Amidst Rapid Innovation

The passenger vehicle segment's commanding 63.82% share in the automobile testing services market is a direct result of its sheer volume and relentless pace of innovation. With global sales hitting 74.6 million units in 2024, the scale is immense. Each vehicle is subject to rigorous safety and performance standards that are constantly evolving. The complexity is compounded by the launch of hundreds of new models, such as the 330 planned by Chinese automakers from 2024 to 2026, and the 24 new EV models introduced in the U.S. in 2024 alone. This continuous cycle of development and release makes comprehensive evaluation a necessity. Furthermore, post-launch issues underscore the critical role of the automobile testing services market, with over 28 million vehicles recalled in the U.S. in 2024, and 13.8 million of those stemming from complex software and electronic issues.

Investments in testing infrastructure, like DEKRA's $22.8 million center and Toyota's $50 million proving ground expansion, confirm the segment's importance. These facilities are essential for validating the next generation of automotive technology. The push for safer vehicles is not just market-driven but also regulatory, with upcoming mandates for features like Automatic Emergency Braking (AEB) by 2029 forcing OEMs to engage in extensive pre-compliance testing. The existence of 72.7 million vehicles on U.S. roads with open recalls represents a significant area of ongoing activity for the automobile testing services market.

- Software validation is paramount, as evidenced by 174 recall campaigns in 2024 for electronic system failures.

- The introduction of 24 new electric car models in the U.S. in 2024 created fresh demand for specialized battery and charging system testing.

- Government mandates, such as the upcoming AEB requirement, create a non-negotiable demand for specific validation services across all new models.

ICE and Hybrid Vehicles Sustain Robust Testing Demand

Despite the global shift towards electrification, the Internal Combustion Engine (ICE) vehicle segment continues to anchor the automobile testing services market with a 62.22% share. This dominance is rooted in the massive global fleet of existing ICE vehicles, which number in the hundreds of millions and require ongoing safety and emissions checks. In 2025, the majority of the nearly 290 million vehicles on U.S. roads will still rely on combustion engines. Continuous production of new ICE and hybrid models, particularly in emerging markets, further fuels this demand. For instance, in 2024, Austria alone saw registrations of over 84,000 new petrol cars and nearly 67,000 petrol-hybrids, each requiring validation against modern standards.

Stringent environmental regulations remain a primary driver, mandating complex and precise emissions testing for all new and existing models. Furthermore, safety recalls specific to ICE and hybrid powertrains continue to generate significant testing work. In 2024, Volkswagen recalled over 260,000 vehicles for a fuel pump defect, while Toyota recalled over 280,000 Tundras and Sequoias for a transmission control issue. These large-scale actions necessitate extensive diagnostic and validation services. Even as the market evolves, the sheer scale and mechanical complexity of ICE technology ensure a sustained and significant need for the automobile testing services market.

- The 22 million vehicles in Texas, mostly ICE-powered, are subject to localized emissions testing, creating a steady stream of regional demand.

- Large-scale recalls, like GM's action on 820,000 trucks, often involve components unique to ICE platforms, requiring specialized testing knowledge.

- New model launches from Chinese brands for export markets will include many ICE variants, each needing to be tested for compliance in the destination country.

OEMs Remain the Primary Drivers of Testing Demand

Vehicle Manufacturers (OEMs) are the definitive end-users in the automobile testing services market, commanding a 40.38% share because the ultimate responsibility for a vehicle's safety and compliance rests with them. Every stage of a car's life, from initial concept to end-of-life, is governed by a testing protocol created, funded, and managed by the OEM. This is evident in the massive investments manufacturers make in their own facilities, such as Toyota's over $50 million proving ground enhancement and GM's new EV center at Milford. These sites are the heart of R&D, where new technologies and entire vehicle platforms are rigorously validated before reaching the public.

OEMs are also the source of all testing activity related to recalls and product updates. In the first half of 2024, manufacturers like Ford and Chrysler recalled millions of vehicles, triggering enormous internal and external testing campaigns that they are required to oversee. The competitive drive to earn accolades like the IIHS TOP SAFETY PICK awards also pushes OEMs to conduct relentless testing to meet ever-higher safety benchmarks. Whether performed in-house or outsourced, every test is ultimately initiated to meet an OEM's objective, solidifying their central role in the automobile testing services market.

- The launch of 330 new car models by Chinese OEMs directly places the immense burden of pre-production testing squarely on the manufacturers.

- In Q2 2024, Chrysler and Ford led in recall campaigns, initiating 14 and 12 respectively, each requiring a cascade of validation tests.

- Twenty major automakers voluntarily met a commitment to implement AEB, a feat that required years of dedicated, OEM-led testing and development.

Customize This Report + Validate with an Expert

Access only the sections you need—region-specific, company-level, or by use-case.

Includes a free consultation with a domain expert to help guide your decision.

Fee-for-Service Model Delivers Essential Independent Expertise

The Fee-for-Service business model leads the automobile testing services market with a 40.54% share by providing specialized, impartial, and cost-effective solutions that are indispensable to the industry. The increasing complexity of vehicles, particularly in areas like software, cybersecurity, and V2X communication, requires expertise and equipment that is unfeasible for many OEMs to develop in-house. This is demonstrated by the high usage of third-party facilities like Toyota's Arizona Proving Grounds, which has already hosted 37 different organizations. These independent providers offer a critical service for validation, handling overflow testing, and certifying compliance with new and complex regulations, such as China's upcoming mandatory OTA standard.

Major investments from independent testing companies, including DEKRA's new $22.8 million facility in Michigan, highlight the growth and vitality of this segment. These centers are crucial for the entire ecosystem, from startups to established giants. When millions of vehicles are recalled for software issues, as seen with Tesla's 5.1 million affected vehicles in 2024, the need for third-party software validation becomes paramount to ensure fixes are robust and secure. The automobile testing services market relies on these external partners to maintain integrity and manage the sheer volume of testing required in the modern automotive landscape.

- The 203,400 hours of testing performed for external clients at just one facility showcases the immense scale of outsourced testing demand.

- Companies like Applus are focusing on technological development to specifically cater to the growing need for advanced, independent validation.

- The rise of OTA updates, affecting over 11 million cars in China in 2024, creates a new frontier for specialized, fee-based software testing services.

To Understand More About this Research: Request A Free Sample

Regional Analysis

Europe Sets the Global Pace Through Regulatory and Technological Rigor

Europe's dominance with over 40% market share in the automobile testing services market is fortified by its proactive regulatory framework and substantial infrastructure investments. The implementation of Euro 7 in 2025, for instance, mandates onboard emissions monitoring for an extensive 160,000 kilometers, creating a long-term compliance testing demand. Safety standards are also advancing, with the 2025 Euro NCAP protocols introducing four new scenarios for child presence detection and new tests for AEB responses to motorcycles. Such regulatory depth compels continuous and sophisticated validation services across the continent.

To meet these demands, capital is flowing into specialized facilities. Germany's leadership is evident with TÜV SÜD's new 3,000-square-meter battery lab and DEKRA's €30 million automated driving test field, both opened in 2024. Spain’s Applus+ IDIADA is completing a €50 million investment in new AV tracks, while the UK's UTAC facility has installed new 1,000 kg payload battery vibration rigs. These strategic investments ensure European testing providers have the advanced capabilities needed to validate the next generation of vehicles.

Asia Pacific Builds a Self-Reliant and Dominant EV Testing Ecosystem

The Asia Pacific automobile testing services market is rapidly scaling its testing infrastructure, driven by China's aggressive push into electric and intelligent vehicles. China's new GB 44495-2024 cybersecurity standard creates an immediate need for specialized validation against over 60 technical requirements. The government's support is clear, with 17 national-level AV testing zones now operational and CATARC building a new RMB 2 billion EV safety center. South Korea's KATECH has also bolstered its capabilities by opening a new 10,000-square-meter battery safety testing center in 2024, positioning the region as a leader in battery validation.

North America Focuses on Large-Scale AV and EV Battery Validation

North America's strategy is characterized by massive investments in both autonomous vehicle validation and the domestic EV supply chain. The U.S. government is a key enabler behind the growth of the automobile testing services market, providing $71 million in funding for vehicle technology projects in 2024. This public support is complemented by major private investments, including Toyota’s new 5.5-mile high-speed oval in Arizona. The EV battery ecosystem is a major focus, evidenced by Intertek's 200,000-square-foot lab expansion and UL Solutions' ongoing expansion of its Michigan battery testing facility, which will add 12 new walk-in chambers in 2025.

Strategic Deals Reshaping the Global Automobile Testing Services Market

- Keysight Technologies Acquires ESI Group (January 2024): Keysight completed its acquisition of virtual prototyping and simulation software provider ESI Group for €913 million to enhance its software-centric solutions for virtual testing and design.

- Ansys and Synopsys Announce Definitive Acquisition Agreement (January 2024): Synopsys agreed to acquire simulation software leader Ansys for approximately $35 billion, a landmark deal to create a powerhouse in silicon-to-systems design and validation for complex automotive electronics.

- Element Materials Technology Acquires Nutech (January 2024): Element expanded its capabilities in the U.S. by acquiring Nutech, a materials testing and consulting engineering company, to strengthen its services for the transportation and infrastructure sectors.

- Cadence Acquires BETA CAE Systems (March 2024): Cadence announced its intent to acquire BETA CAE Systems for approximately $1.24 billion. The acquisition expands Cadence's multiphysics system analysis portfolio, crucial for automotive structural and thermal testing simulations.

- SGS Acquires The CGS Group (February 2024): Global testing leader SGS acquired The CGS Group in Romania, a specialist in non-destructive testing and inspection services, to enhance its industrial and automotive component testing footprint in Eastern Europe.

- Formel D Acquires CPS Quality (July 2024): Automotive service provider Formel D acquired CPS Quality, an expert in quality control and rework services for the automobile testing services market, expanding its service portfolio in quality assurance and post-production testing.

- HORIBA Invests in New UK Facility (May 2024): HORIBA announced a multi-million-pound investment to create a new Centre of Excellence for Innovation and Technology at its Nuneaton site in the UK, focused on future mobility testing

- Trigo Secures New Funding Round (May 2024): Trigo, a company providing AI-powered optical quality inspection for automotive manufacturing, secured a new round of funding led by Porsche Ventures and CEP-Research to scale its automated visual testing technology.

- UL Solutions Invests in Expanded EV Charging Testing (April 2024): UL Solutions announced a significant investment to expand its EV charging testing capabilities in Germany, adding capacity to test to OCPP (Open Charge Point Protocol) and other key global standards.

Top Companies in the Automobile Testing Services Market

- DEKRA SE

- TÜV SÜD

- Bureau Veritas S.A

- Intertek Group Plc

- SGS S.A.

- Rohde & Schwarz

- Element Materials Technology

- Applus+

- TRC Inc

- Nevada Automotive Test Center

- Automotive Testing and Development Services, Inc.

- ATESTEO GmbH & Co. KG

- Novelic

- Robert Bosch GmbH

- UL LLC

- Siemens AG

- ABB Ltd.

- AVL List GmbH

- Link Engineering Company

- cetecom advanced

- Horiba

- Ono Sokki

- A&D

- Ricardo

- IAV

- FEV

- Other Prominent Players

Market Segmentation Overview

By Component

- Hardware

- Compressor Calorimeter

- Compressor Endurance Test Stand

- Low Air Flow Test Bench

- Closing Force Meter

- Mobile Test Lane

- Sound Level Meter

- Speedometer Tester

- Others

- Software

- Simulation Software

- Embedded Software Testing

- Functional Safety Software

- Service

- Traditional Testing

- Emissions Testing

- Tailpipe Emissions

- Fuel Vapor Emissions

- Real Driving Emissions (RDE)

- Others (Cold Start Emission Testing, Fuel Permeation Testing, etc.)

- Safety Testing

- Crashworthiness (Frontal/Side/Rollover)

- Crash Avoidance (ABS, ESC)

- Occupant Protection (Airbags, Seatbelts)

- Others (Child Restraint Systems (CRS) Testing, Fire Resistance of Fuel Systems, etc.)

- Performance Testing

- Drivability

- Acceleration

- Top Speed

- Gear Shift

- Others

- Handling & Stability

- Braking Distance

- Others (NVH Testing (Noise, Vibration, Harshness), Thermal Management System Testing (cooling, HVAC ))

- Material Testing

- Tensile and Fatigue Testing

- Metallurgical Analysis

- Coating & Surface Testing

- Others (Abrasion Resistance (seats, fabrics, buttons), Aging/Weathering Testing (Xenon Arc, Ozone ))

- Emissions Testing

- Advanced Testing

- Autonomous Driving System & ADAS Testing

- Sensor Calibration (LIDAR, Radar, Cameras)

- Scenario Simulation (Urban/Highway)

- V2X Communication Testing

- Lane Departure Warning

- Adaptive Cruise Control

- AEB (Automatic Emergency Braking)

- Others (Edge-case Scenario Simulation, Sensor Fusion Testing, etc.)

- Cybersecurity Testing

- Penetration Testing

- Secure Boot Validation

- Network Intrusion Detection

- Others (Threat Modeling & Risk Assessment (TARA), Secure Communication Protocol Validation, etc.)

- Battery Testing (EVs)

- Charge/Discharge Cycle Testing

- Thermal Runaway Analysis

- Battery Abuse Testing (Drop, Crush)

- Charger Compatibility & Interoperability Testing

- High Voltage Safety Testing (insulation, leakage)

- Others (Electrical Load Box Testing, Relay, Fuse, and Switch Endurance Testing, etc.)

- Others

- Autonomous Driving System & ADAS Testing

- Traditional Testing

By Vehicle Type

- Passenger Vehicles

- Two-Wheelers

- Cars

- SUV & MUV

- Sedan

- Hatchback

- Convertibles

- Others

- Commercial Vehicles

- Light Commercial Vehicles (LCVs)

- Heavy Commercial Vehicles (HCVs)

- Off-road Vehicles

- Agricultural Tractors

- Construction Equipment

- Others

By Vehicle Components

- Vehicle

- Powertrain

- Engine

- Transmission/Gearbox

- Fuel System

- EV Motor & Inverter

- Battery Pack & BMS

- Others

- Chassis

- Suspension

- Steering System

- Tires & Wheels

- Others

- Software

By Propulsion Type

- Internal Combustion Engine (ICE) Vehicles

- Gasoline Engine

- Diesel Engine

- Conventional Diesel

- HVO (Hydrotreated Vegetable Oil)

- Other Alternative Diesel Fuels

- Gasoline Engine

- Electric Vehicles (EVs)

- Hydrogen Fuel Cell Vehicles

By Business Model

- Fee-for-Service Testing

- Contract-Based Long-Term Testing

- Joint OEM-Lab Collaborations

- Government-Authorized Type Approval Testing

By Location

- On-Site

- Off-Site

By Testing Duration

- Short-cycle (Regulatory compliance, 1-2 weeks)

- Mid-cycle (Feature validation, 3-6 months)

- Long-cycle (Durability & Lifecycle Testing, >1 year)

By End User

- OEMs (Vehicle Manufacturers)

- Tier 1 & Tier 2 Suppliers

- Government Regulatory Bodies

- Automotive R&D Institutions

- Testing Labs/Service Providers

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- Western Europe

- The UK

- Germany

- France

- Italy

- Spain

- Rest of Western Europe

- Eastern Europe

- Poland

- Russia

- Rest of Eastern Europe

- Western Europe

- Asia Pacific

- China

- India

- Japan

- South Korea

- Australia & New Zealand

- ASEAN

- Rest of Asia Pacific

- Middle East & Africa

- UAE

- Saudi Arabia

- South Africa

- Rest of MEA

- South America

- Argentina

- Brazil

- Rest of South America

LOOKING FOR COMPREHENSIVE MARKET KNOWLEDGE? ENGAGE OUR EXPERT SPECIALISTS.

SPEAK TO AN ANALYST

.svg)

Features | Type of License | ||||

Data Book | Single User |   Multi User | Corporate | ||

| e-Access | ✓ | ✓ | ✓ | ✓ | |

User Sharing | 1 User Only | 1 User Only | Up to 7 Users | Unlimited User Access | |

⨉ | ⨉ | ⨉ | ✓ | ||

Free Customization | No Free Customization | Up To 30 hrs work | Up To 60 hrs work | Up To 80 hrs work | |

Deliverable |

| ⨉ | ✓ | ✓ | ✓ |

| ✓ | ⨉ | ✓ | ✓ | |

| ⨉ | ⨉ | ⨉ | ✓ | |

Analyst Support | 2-Months Analyst Support | 4-Months Analyst Support | 7-Months Analyst Support | One Year Analyst Support | |

Free Report update in next update cycle | ⨉ | ⨉ | ⨉ | ✓ | |

Free Industry Update (Within 180 days) | ⨉ | ⨉ | ⨉ | ✓ | |

Benefit | Up to 10% off on Post Purchase | Up to 20% off on Post Purchase | Up to 30% off on Post Purchase | Up to 40% off on Post Purchase | |