Market Scenario

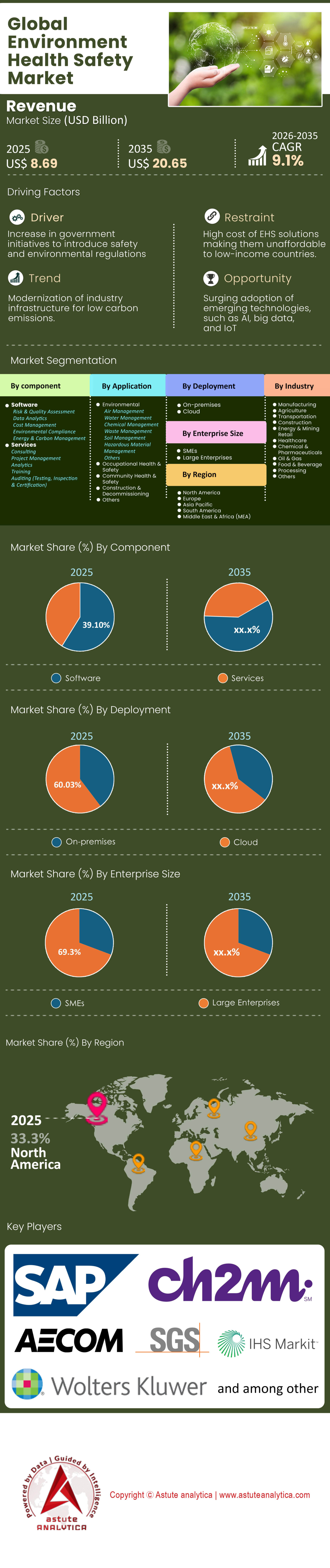

Environment health and safety market was valued at US$ 8.69 billion in 2025 and is projected to hit the market valuation of US$ 20.65 billion by 2035 at a CAGR of 9.1% during the forecast period 2026–2035.

- Based on component, software segment generated an undeniable 58.9% revenue share of the environment health and safety market.

- Based on deployment, cloud based deployment claimed more than 60% of the market’s revenue.

- Based on application, environmental management held a dominant position by capturing over 44.1% of global market revenue.

- North America has been leading the way in the environment health and safety market with over 33% of global revenue coming from the region.

The market encompasses the software, services, and hardware used to manage regulatory compliance, occupational risks, and environmental impact. However, the definition has expanded. In 2025, an EHS platform is also a data lake for Carbon Accounting (Scope 1, 2, and 3 emissions), a control tower for Supply Chain Due Diligence, and a psychological safety monitor for a post-pandemic workforce.

The fundamental shift driving this market is the move from descriptive analytics to prescriptive analytics (predicting and preventing what will happen). Organizations are no longer satisfied with "Lagging Indicators" like Total Recordable Incident Rate (TRIR), they demand "Leading Indicators" derived from predictive modeling. This shift is fueling a projected CAGR exceeding 9.10% through 2035, pushing the market valuation toward the USD 20 billion mark.

To Get more Insights, Request A Free Sample

Macro-Economic Drivers: The Regulatory and Financial "Pincer Movement"

The growth of the environment health and safety market is being forced by a pincer movement of regulatory tightening and financial necessity, creating a landscape where optionality has been replaced by mandatory adherence. This is not merely about avoiding fines; it is about maintaining the "Social License to Operate" in an era of hyper-transparency where every industrial accident is broadcast globally in real-time.

The Regulatory Tsunami

The "Brussels Effect" continues to dictate global standards, as European Union regulations ripple outward to affect any company wishing to do business in the bloc.

- EU CSRD (Corporate Sustainability Reporting Directive): Fully enforceable in 2025, this directive has forced over 50,000 global companies to report non-financial data with the same rigor as financial data in the environment health and safety market. This has effectively made EHS software the "ERP of Sustainability," requiring audit trails that spreadsheets cannot provide.

- OSHA Modernization: In the US, OSHA’s aggressive stance on heat stress standards and mental health in 2024-2025 has forced industries like construction and agriculture to adopt real-time monitoring solutions. The agency's shift toward "severe violator" enforcement programs has incentivized pre-emptive investment in EHS tech.

- SEC Climate Disclosure: Despite legal stays, the "trickle-down" effect means public companies are demanding carbon data from private suppliers, forcing EHS adoption down the supply chain to Tier 2 and Tier 3 vendors.

The Financial Imperative in the Environment Health And Safety Market

The cost of non-compliance has skyrocketed, creating a direct correlation between EHS maturity and EBITDA margins. In 2025, the average cost of a single fatal workplace incident in the US exceeds USD 1.4 million in direct costs, with indirect costs (reputation, stock volatility, insurance premium hikes) often reaching 10x that amount.

Furthermore, private equity and institutional investors in the environment health and safety market are using EHS data as a proxy for management quality. A company with poor safety metrics is viewed as a high-risk asset, raising its Cost of Capital. Insurers are also playing a pivotal role, increasingly offering premium rebates to industrial clients who deploy verified EHS platforms, effectively subsidizing the market growth.

Market Restraints: Implementation Fatigue and the "Digital Divide"

Despite the bullish outlook, the environment health and safety market faces significant friction points that threaten to slow the velocity of adoption in specific sub-sectors.

Implementation Complexity & Data Debt:

For multinational corporations, migrating from legacy on-premise systems to a unified SaaS platform is a multi-year "change management" nightmare. Integrating EHS data with HR (Workday), ERP (SAP), and Manufacturing Execution Systems (MES) creates data normalization challenges. Many companies are sitting on decades of unstructured data (PDF scans, handwritten notes) that cannot be easily ingested into modern AI engines, creating a "Data Debt" that stalls deployment.

The SME Gap in Environment Health And Safety Market

While Enterprise adoption is high, Small and Medium Enterprises (SMEs) struggle with the high licensing costs of Tier-1 EHS platforms. This has created a bifurcated market where large players use AI-driven tools, while smaller players remain stuck on spreadsheets, creating supply chain blind spots. The market is waiting for "Lite" versions of these platforms to penetrate the mid-market effectively.

Data Privacy vs. Safety:

The rise of computer vision and wearables has triggered privacy concerns. In the EU, GDPR restrictions on biometric data collection hamper the full deployment of "Connected Worker" technologies. Unions in North America are also pushing back against "surveillance safety," requiring vendors to build privacy-masking features (like blurring faces in video feeds) directly into their EHS products.

Industry Vertical Assessment in the Environment Health and Safety Market

To understand where the money flows in the environment health and safety market, one must analyze the specific risk profiles and spending power of key industry verticals. The adoption is not uniform; it is concentrated in high-consequence industries where safety failure is an existential threat.

Energy, Mining, and Utilities (30% of Market Spend)

The environment health and safety market remains the largest spender and the most technologically advanced. The focus here is on Process Safety Management (PSM) and Control of Work. The integration of EHS software with digital twins (virtual replicas of physical assets) is highest in this sector. Oil majors are using these tools to simulate pressure variances and prevent catastrophic failures, justifying massive software contracts that span decades.

Manufacturing (Automotive & Discrete)

The focus here is on Ergonomics, Chemical Management, and Incident Management. With the global shift to EV (Electric Vehicle) manufacturing, new hazards related to high-voltage battery handling and exotic materials are driving a refresh cycle of EHS training software and chemical tracking databases. The "Just-in-Time" nature of this industry means any safety shutdown is costly, driving high uptime-focused EHS spending.

Construction & Engineering

Historically the "tech laggard," this vertical is now the fastest grower across the global environment health and safety market. The construction industry faces the highest fatality rates globally, often due to transient workforces. This is driving the adoption of Computer Vision (cameras detecting lack of hard hats or harnesses) and Geofencing (alerts when workers enter danger zones). The digitization of the "Permit to Work" process on construction sites is a massive growth area.

Healthcare & Pharmaceuticals

This vertical drives the specialized demand for Bio-Safety and Occupational Health. Following the pandemic, the tracking of employee health, vaccination status, and exposure to pathogens has become a permanent module in EHS suites for hospitals and labs.

Technological Frontiers: AI, IoT, and the "Connected Worker"

The environment health and safety market is currently being redefined by a technological trinity: Artificial Intelligence, the Internet of Things, and Connected Worker platforms. These technologies are stripping the latency out of safety management, allowing for real-time intervention.

1. Artificial Intelligence (AI) & Computer Vision

AI is the biggest differentiator in 2025. It is moving EHS from data entry to data insights.

- Natural Language Processing (NLP): Large Language Models (LLMs) are being used to scan millions of historical "near-miss" reports (often unstructured text) to identify hidden trends and precursors to accidents that humans miss.

- Predictive Risk Scoring: Algorithms analyze weather data, shift schedules, fatigue levels, and historical incident rates to give a "Risk Score" for the day. If the score is too high, supervisors can halt work or mandate extra breaks.

- Generative AI: EHS platforms are using GenAI to auto-draft incident investigation reports and suggest corrective actions based on global best practices, reducing the administrative burden on safety officers by 40%.

2. The Internet of Things (IoT) & Wearables

The market for industrial wearables is merging with environment health and safety market to create the "Connected Worker."

- Smart PPE: Helmets with built-in fall detection and gas detection sensors are communicating directly with EHS platforms.

- Biometrics: Watches that monitor heart rate and core body temperature are critical for preventing heat stress in a warming world.

- Integration Challenge: The challenge—and the market opportunity—lies in piping this terabyte-scale data into the EHS platform without crashing the system. Cloud-native vendors who have solved this "high velocity" data ingestion problem are winning market share.

3. Digital Twins in the Environment Health and Safety Market

High-maturity organizations are using digital twins to simulate emergency evacuations or chemical release plumes. This allows safety teams to "practice" disasters in a virtual environment, identifying bottlenecks in evacuation routes before a real crisis occurs.

Competitive Landscape: Consolidation and "Platformization"

The environment health and safety market is highly fragmented but undergoing rapid consolidation via Private Equity, reshaping the vendor landscape into a battle of titans.

The Tier 1 "Platform" Players

Companies like Enablon (Wolters Kluwer), Sphera (Blackstone), Intelex (Fortive), and Cority (Thoma Bravo) dominate the enterprise space.

- M&A Strategy: These players are aggressively acquiring niche startups. If a startup develops a superior "Ergonomic Assessment via Video" tool, a Tier 1 player will acquire it to plug into their broader suite. This creates a high barrier to entry for new competitors.

- The "One-Stop-Shop": Enterprise buyers prefer a single contract for EHS, ESG, and Operational Risk. Vendors are responding by bundling these capabilities, freezing out point-solution competitors.

The "Strategic Acquisition" Trend

The EQT / Avetta Deal (2024): The $3 Billion acquisition of Avetta by EQT underscores the massive valuation multiples in the environment health and safety market. Investors see EHS/Supply Chain Risk software as "Critical Infrastructure" similar to utilities.

- Vertical Specialists: Smaller players are surviving by going deep into specific verticals (e.g., Veraforce for Oil & Gas compliance) rather than trying to be a generalist. They survive by offering deep, industry-specific workflows that generalist platforms cannot match.

Pricing Dynamics and Business Models

The business model in the environment health and safety market has shifted entirely to SaaS Subscription, altering how value is perceived and procured. This shift has aligned vendor incentives with customer success, as vendors must now re-earn the business every renewal cycle.

- Per-User vs. Site-Based Pricing: The market utilizes a hybrid model. General safety apps (incident reporting) are typically priced Per-User (USD 10−50/user/month), while Environmental modules are priced Per-Site or Per-Asset based on complexity and emissions volume.

- The Rise of "Freemium" for SMEs: To capture the underserved SME market, some vendors are offering "Freemium" models for basic incident reporting, hoping to upsell advanced analytics later.

- Services Ratio: While software is 58.9% of the market, the ecosystem supports a massive service industry. For every $1 spent on software, approximately $1.50 is spent on implementation and customization services, often provided by third-party partners (like ERM, Arcadis, or Deloitte). This partner ecosystem is critical for vendor growth, as partners act as a sales channel.

Segmental Analysis

By Component, Software Enjoys Market Supremacy

Based on component, software segment generated an undeniable 58.9% revenue share of the environment health and safety market. This dominance is driven by the scalability of SaaS (Software as a Service) models and the inherent "stickiness" of the ecosystem. Unlike consulting services, which are linear (hours x rate) and constrained by human capital, software generates recurring revenue with high margins and infinite scalability.

- The "Stickiness" Factor: Once an EHS software is embedded into a company’s workflow (incident reporting, audit trails, permit-to-work), churn rates are incredibly low (<5%). The cost of ripping and replacing an EHS system is prohibitive, granting incumbent vendors significant pricing power.

- Module Expansion & Net Dollar Retention (NDR): The revenue is not just from new logos but from expanding wallet share within existing clients. Customers who initially buy an "Incident Management" module are increasingly layering on ESG Reporting, Ergonomics, and Chemical Management modules. This "land and expand" strategy is the primary growth engine for the software segment.

- Hardware Commoditization: While IoT sensors are proliferating, their unit cost is dropping rapidly due to manufacturing efficiencies. The value capture in the environment health and safety market has moved from the sensor (hardware) to the analytics dashboard (software) that interprets the sensor data. The market places a premium on the insight, not the instrument.

- Service Coupling: Interestingly, the software growth drives the service market. For every dollar spent on complex enterprise EHS software, approximately $1.50 to $2.00 is spent on implementation and change management consulting, though the revenue recognition for the software itself remains the dominant market force.

By Deployment, Cloud Migration is Holding Complete Dominance

Based on deployment, cloud based deployment claimed more than 60% of the environment health and safety market’s revenue.

Strategic Implications of Cloud Dominance

- Real-Time Regulatory Agility: Regulatory standards change daily across global jurisdictions. Cloud platforms allow vendors (like Enablon, VelocityEHS, or Cority) to push regulatory content updates instantly to all users via the cloud. On-premise systems, which require manual patching, cannot match this agility, leaving companies vulnerable to non-compliance gaps.

- The Mobile Workforce Enabler: 80% of the EHS end-users are "deskless" (factory floor, oil rig, construction site). Cloud architecture is the only viable way to support mobile apps that allow workers to log hazards via smartphone (offline and online). The synchronization of data from the "edge" (the field) to the "core" (HQ) relies entirely on robust cloud pipelines.

- Security Perception Shift: Five years ago, the Defense and Pharma sectors resisted cloud EHS due to IP theft fears. In 2025, the advanced encryption and ISO 27001 certifications of AWS/Azure-hosted EHS platforms are viewed as more secure than internal on-premise servers, which are often poorly patched. This has driven the remaining holdouts in sensitive industries to migrate.

- Scalability and TCO: The Total Cost of Ownership (TCO) for cloud solutions is lower over a 5-year horizon when factoring in the elimination of internal server maintenance and IT staffing costs. This economic argument has won over CFOs, accelerating the retirement of legacy on-prem systems.

Customize This Report + Validate with an Expert

Access only the sections you need—region-specific, company-level, or by use-case.

Includes a free consultation with a domain expert to help guide your decision.

By Application, The "E" in ESG Takes the Lead

Based on application, environmental management held a dominant position by capturing over 44.1% of global environment health and safety market revenue. But, why environmental management is king?

- Carbon Accounting is the New Accounting: The demand for "audit-grade" environmental data to satisfy the EU CSRD and California’s SB 253 has exploded. Companies need software to calculate complex emission factors across global sites.

- Waste & Water: Circular economy initiatives are forcing manufacturing firms to track waste streams granularly. EHS software is the system of record for "Zero Waste to Landfill" certifications.

- Risk Profile: An occupational safety incident affects one individual; an environmental incident (e.g., a chemical spill) affects a community and can bankrupt a company (e.g., PFAS litigation). The budget allocation reflects this catastrophic risk potential.

To Understand More About this Research: Request A Free Sample

Regional Analysis in Environment Health Safety Market

North America’s Regulatory Fortress Remains Strong Over 33% Revenue Contribution

North America has been leading the way in the environment health and safety market with over 33% of global revenue coming from the region.

The North American Advantage

Litigation Culture: The U.S. legal environment makes EHS documentation a defensive necessity. The average OSHA penalty is negligible compared to the potential civil liability of negligence. This drives "over-compliance" and heavy software spend.

Technological Maturity: North American industrial bases (Automotive in Detroit, Oil & Gas in Texas) were early adopters of IIoT (Industrial Internet of Things).

Consolidation Hub: The majority of major EHS M&A activity (Private Equity buyouts) in the environment health and safety market originates in North America, keeping capital flows and revenue recognition centered in the region.

Contrast: While APAC is growing faster (CAGR >9%) due to industrialization in India and China, the Average Selling Price (ASP) of software in APAC is lower, keeping North America ahead in total revenue volume..

Asia-Pacific: The High-Velocity Growth Engine and Digital Leapfrog

Asia-Pacific (APAC) is undoubtedly the undisputed leader in environment health and safety market when it comes to growth. The region is projected to register the highest CAGR through 2035. The narrative in APAC has shifted dramatically from "minimal compliance" to "strategic digitization," driven by the region's role as the world's manufacturing floor. As Western OEMs (Original Equipment Manufacturers) impose strict Scope 3 emission targets and safety audits on their supply chains, factories in China, India, and Vietnam are being forced to digitize their EHS operations to retain contracts.

Unlike the West, which is burdened by legacy on-premise systems, APAC environment health and safety market is benefiting from the "Leapfrog Effect"—skipping the desktop era entirely and moving directly to mobile-first, cloud-native EHS applications. The market is witnessing a surge in demand for lightweight, Android-based safety apps that function in low-bandwidth environments. Furthermore, rapid infrastructure development in India and Southeast Asia is fueling massive demand for Construction Safety and Permit-to-Work software, as governments tighten regulations to curb historically high incident rates in infrastructure projects.

Europe: The Global Regulatory Superpower and ESG Incubator

Europe remains the intellectual and regulatory heartbeat of the global environment health and safety market, setting the gold standard for sustainability and worker health that the rest of the world eventually adopts. The market dynamics here are defined by complexity and sophistication rather than just raw volume. The European Union’s "Green Deal" and the enforcement of the Corporate Sustainability Reporting Directive (CSRD) have effectively merged the EHS and ESG markets into a single compliance ecosystem.

European enterprises are not just buying safety software; they are investing in complex Environmental Management Information Systems (EMIS) to track carbon neutrality pathways with audit-grade precision.

Top 5 Recent Strategic Developments in the Environment Health and safety Market (2025)

Cority Acquires Meddbase (January 2025):

Cority announced the acquisition of Meddbase, a pioneer in cloud-native occupational medicine software. This strategic consolidation integrates Meddbase’s clinical management capabilities directly into Cority’s enterprise EHS platform, allowing clients to unify safety data with medical surveillance and workforce health records to meet rising bio-safety demands.

EcoOnline Acquires D4H (June 2025):

EcoOnline expanded its operational resilience portfolio by acquiring D4H, a global leader in crisis response software. The acquisition embeds active emergency management tools—such as live incident command boards—into EcoOnline’s preventive safety suite, bridging the gap between risk planning and real-time emergency execution.

Sphera Secures Strategic Investment from Neuberger Berman (September 2025):

Sphera announced a significant growth investment from Neuberger Berman Capital Solutions. While Blackstone retains majority ownership, this new capital is explicitly earmarked to accelerate Sphera’s "Scope 3" supply chain transparency tools and AI-driven sustainability innovations, signaling strong institutional confidence in the ESG-EHS overlap.

VelocityEHS Launches AI-Powered Incident Management (October 2025):

VelocityEHS unveiled major updates to its Accelerate® Platform, featuring generative AI capabilities. The new tools automatically draft incident narratives and identify root causes from unstructured data fields, significantly reducing the administrative burden on safety professionals while improving data fidelity.

Blackline Safety Unveils G8 Wearable (December 2025):

Blackline Safety launched the G8, marketed as the industry’s most advanced connected safety wearable. The device combines multi-gas detection with satellite connectivity and real-time biometric monitoring, pushing the boundaries of the Industrial Internet of Things (IIoT) for lone worker protection in hazardous environments.

Top Players in the Environment Health and Safety Market

- AECOM Corp

- CH2M HILL, Inc.

- Cority Software Inc.

- Dakota Software Inc.

- DNV GL

- Enablon Corp.

- ENVIANCE

- ETQ, LLC

- Gensuite LLC

- Golder Associates

- HIS

- Intelex Technologies Inc.

- Isometrix

- ProcessMAP

- Quentic GmbH

- SAI Global Pty Limited

- SAP SE

- SGS SA

- Sphera

- Tetra Tech, Inc.

- UL LLC

- Velocity EHS Holdings Inc.

- Other Prominent Players

Market Segmentation Overview:

By Component

- Software

- Risk & Quality Assessment

- Data Analytics

- Cost Management

- Environmental Compliance

- Energy & Carbon Management

- Services

- Consulting

- Project Management

- Analytics

- Training

- Auditing (Testing, Inspection & Certification)

By Deployment

- On-Premises

- Cloud

- By Enterprise Size

- SMEs

- Large Enterprises

By Application

- Environmental

- Air Management

- Water Management

- Chemical Management

- Waste Management

- Soil Management

- Hazardous Material Management

- Others

- Occupational Health & Safety

- Community Health & Safety

- Construction & Decommissioning

- Others

By Industry

- Manufacturing

- Agriculture

- Transportation

- Construction

- Energy & Mining

- Retail

- Healthcare

- Chemical & Pharmaceuticals

- Oil & Gas

- Food & Beverage Processing

- Others

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- UK

- Germany

- France

- Italy

- Belgium

- Spain

- Poland

- Russia

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Australia & New Zealand

- South Korea

- ASEAN

- Thailand

- Rest of ASEAN

- Rest of Asia Pacific

- Middle East & Africa (MEA)

- UAE

- Turkey

- Saudi Arabia

- Jordan

- Rest of MEA

- South America

- Argentina

- Brazil

- Rest of South America

REPORT SCOPE

| Report Attribute | Details |

|---|---|

| Market Size Value in 2025 | US$ 8.69 Billion |

| Expected Revenue in 2035 | US$ 20.65 Billion |

| Historic Data | 2020-2024 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Unit | Value (USD Bn) |

| CAGR | 9.1% |

| Segments covered | By Component, By Deployment, By Application, By Industry, By Region |

| Key Companies | AECOM Corp, CH2M HILL, Inc., Cority Software Inc., Dakota Software Inc., DNV GL, Enablon Corp., ENVIANCE, ETQ, LLC, Gensuite LLC, Golder Associates, HIS, Intelex Technologies Inc., Isometrix, ProcessMAP, Quentic GmbH, SAI Global Pty Limited, SAP SE, SGS SA, Sphera, Tetra Tech, Inc., UL LLC, Velocity EHS Holdings Inc., Other Prominent Players |

| Customization Scope | Get your customized report as per your preference. Ask for customization |

FREQUENTLY ASKED QUESTIONS

Valued at US$8.69 billion in 2025, it's projected to reach US$20.65 billion by 2035, growing at a 9.1% CAGR (2026–2035), driven by regulatory pressures and AI/IoT adoption.

Software leads with 58.9% (scalable SaaS stickiness), cloud deployment over 60% (real-time agility for mobile workforces), and environmental management 44.1% (carbon accounting mandates like EU CSRD).

A pincer movement of regulations (EU CSRD, OSHA modernization, SEC disclosures) and financial imperatives (US$1.4M+ per fatal incident, investor EHS scrutiny), enforcing prescriptive analytics over lagging indicators.

Energy/mining/utilities (30% spend, digital twins for PSM), manufacturing (EV hazards), and construction (fastest growth via computer vision/geofencing), prioritizing high-risk, high-consequence operations.

AI enables predictive risk scoring and NLP for near-miss trends; IoT wearables create Connected Workers for real-time heat/fall detection; digital twins simulate disasters, slashing admin by 40% via GenAI.

North America leads (33% revenue, litigation-driven); APAC grows fastest (leapfrog to cloud/mobile); Europe sets ESG standards. Restraints include SME cost gaps, data debt, and privacy hurdles (GDPR/union pushback).

LOOKING FOR COMPREHENSIVE MARKET KNOWLEDGE? ENGAGE OUR EXPERT SPECIALISTS.

SPEAK TO AN ANALYST

.svg)

Features | Type of License | ||||

Data Book | Single User |   Multi User | Corporate | ||

| e-Access | ✓ | ✓ | ✓ | ✓ | |

User Sharing | 1 User Only | 1 User Only | Up to 7 Users | Unlimited User Access | |

⨉ | ⨉ | ⨉ | ✓ | ||

Free Customization | No Free Customization | Up To 30 hrs work | Up To 60 hrs work | Up To 80 hrs work | |

Deliverable |

| ⨉ | ✓ | ✓ | ✓ |

| ✓ | ⨉ | ✓ | ✓ | |

| ⨉ | ⨉ | ⨉ | ✓ | |

Analyst Support | 2-Months Analyst Support | 4-Months Analyst Support | 7-Months Analyst Support | One Year Analyst Support | |

Free Report update in next update cycle | ⨉ | ⨉ | ⨉ | ✓ | |

Free Industry Update (Within 180 days) | ⨉ | ⨉ | ⨉ | ✓ | |

Benefit | Up to 10% off on Post Purchase | Up to 20% off on Post Purchase | Up to 30% off on Post Purchase | Up to 40% off on Post Purchase | |