Genomic Testing Market: By Offering (System and Software, Reagents & Consumables, Services); Testing Type (Sequencing Solution, Others); Technology (Proteomics, Pharmacogenomics, Stem Cell Therapy, Cloning); Indication (Cancer, Asthma, Diabetes, Hearth Diseases, Agricultural Production, Others); End-User (Hospitals & Clinics, Research Centers & Academic Institutions, Pharmaceutical & Biotechnology Companies, Others); Region—Market Size, Industry Dynamics, Opportunity Analysis and Forecast for 2026–2035

- Last Updated: 13-Jan-2026 | | Report ID: AA0423400

Market Scenario

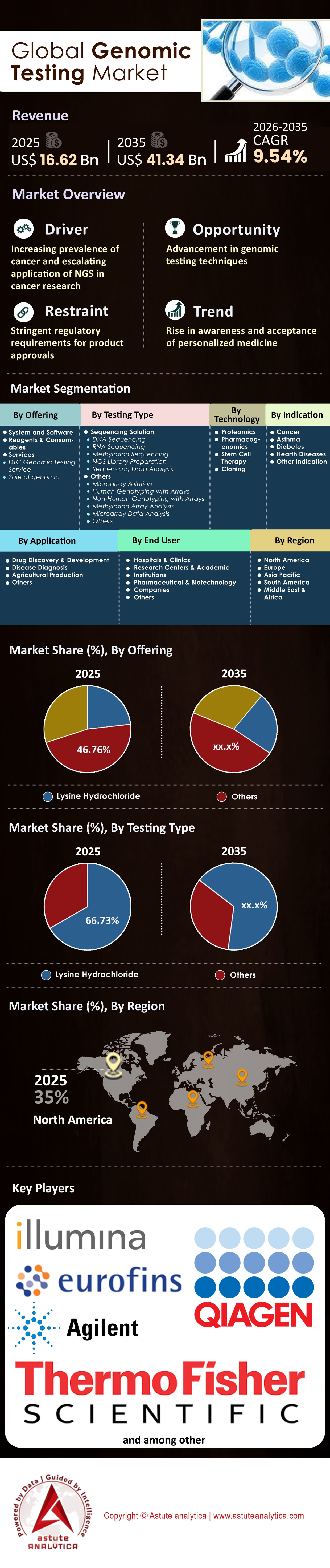

Genomic testing market was valued at USD 16.62 billion in 2025 and is projected to attain a valuation of USD 41.34 billion by 2035, at a CAGR of 9.54% during the forecast period, 2026-2035.

Key Findings Shaping the Market

- Based on product type, reagents and consumables segment accounts for over 46.7% of the market share.

- Based on testing type, sequencing solutions, more predominantly Next Generation Sequencing (NGS) technologies, remain the huge players in the genomic testing market accounting for a market share exceeding 66.73%.

- Based on application, drug development and drug discovery emerged as the key consumers of the genomic testing around the world with more than 46% global market revenue comes from this application.

- By technique, all stem cell therapy remains an important aspect of market, and it occupied 42.4% share.

- North America is leader in the global genomic testing market by accounting for 35% market share.

Genomics testing is the scientific process of decoding the genetic blueprint of an organism to identify alterations, such as mutations or variants, that may signal disease susceptibility or influence treatment responses. It has evolved from a niche research tool into the cornerstone of modern precision medicine. By analyzing DNA, RNA, or chromosomal structures, genomics testing allows clinicians to predict disease risk, diagnose rare conditions early, and tailor therapies to the molecular profile of a patient.

The genomic testing market is currently undergoing a paradigm shift, transitioning from episodic diagnostic usage to continuous health monitoring, fundamentally altering how healthcare is delivered globally.

To Get more Insights, Request A Free Sample

How Are Chronic Disease Epidemics Fueling the Surge in Demand?

Chronic diseases are the primary engine propelling the genomic testing market forward. According to the World Health Organization (WHO) 2024 updates, cancer remains a leading cause of death, with approximately 20 million new cases reported annually worldwide. The WHO further projects a 77% increase in cancer cases by 2050. Consequently, the demand for genomic profiling in oncology has skyrocketed, as oncologists rely on these tests to identify specific Cancer biomarkers for targeted therapies. In the United States alone, the Centers for Disease Control and Prevention (CDC) reported in 2024 that over 38.4 million Americans have diabetes, and another 97.6 million have prediabetes. As research increasingly links specific genetic markers to Type 2 diabetes susceptibility, genomics testing is becoming a vital tool for early intervention and lifestyle modification strategies.

Precision medicine is the direct beneficiary of these alarming statistics. For instance, the survival rate for patients treated with genomically matched therapies is significantly higher than those receiving standard chemotherapy. In 2025, Natera reported a massive 52% year-over-year increase in their oncology test volumes, processing 800,800 tests. Such figures indicate that the clinical community is aggressively adopting genomics testing to manage the burden of chronic disease. Guardant Health similarly saw its biopharmaceutical test volumes grow by 56% in Q2 2024, proving that drug developers are equally reliant on genomic data to create next-generation treatments for these conditions.

Which Technology Reigns Supreme in the Genomics Landscape?

Next-Generation Sequencing (NGS) stands as the undisputed titan of the genomic testing market. Unlike older methods like Sanger sequencing or microarrays, NGS offers high-throughput capabilities that allow for the simultaneous sequencing of millions of DNA strands. The demand for NGS is growing exponentially in cancer gene therapy because it delivers speed, accuracy, and unprecedented cost-efficiency. In 2024, Illumina claimed its NovaSeq X series reduced the cost of sequencing a human genome to approximately USD 200. This price point breaks the economic barrier that previously prevented widespread adoption, making whole-genome sequencing (WGS) feasible for routine clinical care rather than just elite research.

Innovation in read lengths is further solidifying NGS dominance in the genomic testing market. PacBio, a leader in long-read sequencing, achieved a read length record of over 4 million base pairs in 2024/2025 research studies. Long-reads are essential for detecting structural variants that short-read technologies often miss. In fact, PacBio reported a 16.7% improvement in solving previously undiagnosed neurodegenerative cases in 2025 using their technology. Such technological leaps ensure that NGS remains the preferred platform for the genomics testing industry, driving a hardware replacement cycle that benefits manufacturers.

How Are Demographic Shifts and Population Growth Acting as Catalysts?

Global population dynamics are creating a fertile environment for the genomic testing market expansion. With the global population exceeding 8.2 billion in 2025, the sheer volume of individuals requiring healthcare is at an all-time high. More critically, the world is aging; the WHO estimates that by 2030, one in six people in the world will be aged 60 years or over. An aging demographic is naturally more prone to genomic instability and age-related diseases like cancer and Alzheimer’s, necessitating frequent genomics testing.

Prenatal demographics are also driving volume in the genomic testing market. As the average maternal age rises in developed nations, the risk of chromosomal abnormalities increases, fueling the market for Non-Invasive Prenatal Testing (NIPT). North Carolina Medicaid’s decision to add coverage for Whole Genome Sequencing for NICU infants in June 2024 highlights how population health strategies are embracing genomics from birth. Additionally, the UTSW 2024 study found that 40% of Americans have now undergone some form of genetic testing, doubling from 19% in 2020. This cultural shift, driven by a growing and aging population, ensures a steady stream of customers for genomics testing providers.

What Key Products Are Witnessing the Strongest Influx of Demand in Genomic Testing Market?

Consumables and liquid biopsy tests are currently the hottest product segments in the global genomic testing market. Consumables—reagents, flow cells, and preparation kits—generate recurring revenue that dwarfs initial instrument sales. For example, Illumina reported a "pull-through" of USD 1.3 million per NovaSeq X instrument in 2024. However, in terms of specific diagnostic products, liquid biopsy is witnessing explosive growth. These non-invasive tests, which detect cancer DNA in blood, are replacing painful tissue biopsies. Guardant Health’s Shield test, a liquid biopsy for colorectal cancer screening, completed 87,000 screening tests in 2025 alone.

Screening products for early detection are also seeing unprecedented uptake. For instance, Exact Sciences reported that its Cologuard test has been used cumulatively 18 million times as of January 2025. The shift toward preventative healthcare in the genomic testing market means that products designed for healthy or asymptomatic populations are gaining traction alongside diagnostic tools for the sick. 10x Genomics is also seeing high demand for its spatial biology instruments, having sold a cumulative 1,500 units by the end of 2025, enabling researchers to map gene expression within tissue samples.

What Are the Most Significant Recent Developments?

Regulatory milestones and strategic consolidations defined the landscape in genomic testing market. The FDA approved 55 novel drugs in 2025, many of which are tied to companion diagnostic approvals. A landmark event occurred when Guardant Health’s Shield test secured FDA approval and subsequent Medicare coverage eligibility for 45 million individuals in 2024. On the data front, the UK Biobank completed the release of whole-genome sequencing data for 490,640 participants in 2025, creating a resource that will fuel drug discovery for decades.

Corporate maneuvers are also reshaping the genomic testing market. Genomics companies raised USD 3.2 billion in equity funding in 2025 across 142 rounds, signaling strong investor confidence despite broader economic headwinds. PacBio launched its new Vega benchtop system in late 2025, delivering 32 units immediately, which signals a move to decentralize genomics testing from large core labs to smaller clinics. These developments underscore a maturing market that is moving from experimental phases to commercial solidity.

Why is the Competitive Landscape of the Genomic testing market So Intensely Rivalrous?

Competition in the market is cutthroat because the winner takes the standard-of-care status. Companies are not just competing on price but on clinical utility and reimbursement access. The barrier to entry is high due to intellectual property rights and the massive capital required for R&D; however, once established, the "lock-in" effect of proprietary reagents creates fierce battles for market share. Legal battles over patent infringements are common as players like Illumina, Oxford Nanopore, and BGI try to protect their technological territories.

Differentiation is the key survival strategy in the genomic testing market. While Illumina dominates high-throughput short-reads, Oxford Nanopore and PacBio are carving out lucrative niches in long-read sequencing. In the service sector, companies like Natera and Exact Sciences are competing fiercely for oncology volumes. Natera’s 53% revenue growth in Q4 2024 illustrates the rewards available for market leaders, incentivizing aggressive sales tactics and heavy marketing spend. The sector is characterized by rapid obsolescence; a company that fails to innovate its chemistry or software risks losing its customer base within a single product cycle.

Segmental Analysis

Reagents and Consumables Dominance Secured by High-Margin Recurring Revenue and Closed Ecosystems

The Reagents and Consumables segment commands a massive 46.7% market share of the genomic testing market, a dominance structurally engineered into the "razor-and-blade" business models of industry leaders. This leadership is not accidental but inevitable; once a sequencer is installed, it generates exponential, recurring revenue through the mandatory purchase of proprietary chemicals. Illumina’s FY2024 financial performance definitively validates this model, with consumables accounting for 72% of total core revenue, significantly outstripping instrument sales. This segment capitalizes on the elasticity of demand: as high-throughput platforms like the NovaSeq X lower the cost-per-genome, the volume of sequencing runs explodes, disproportionately driving reagent sales over hardware.

Furthermore, this dominance of the segment in the genomic testing market is rigorously defended by "closed ecosystems." Proprietary flow cells and library prep kits, such as Illumina’s XLEAP-SBS chemistry or PacBio’s SMRT cells, are non-interchangeable, creating a captive revenue stream that third-party manufacturers cannot breach. Despite fluctuations in capital equipment cycles, companies like PacBio have reported resilient consumable revenue, proving the segment's immunity to economic downturns. The industry-wide shift toward clinical markets further cements this lead, as FDA-regulated In Vitro Diagnostic (IVD) kits command premium pricing over research-grade alternatives. Consequently, every clinical test performed directly subsidies this segment’s commanding share through mandatory, high-margin consumption.

Next Generation Sequencing Solutions Dominate Through Clinical Reimbursement and Liquid Biopsy Adoption

Accounting for an overwhelming 66.73% of the genomic testing market, Sequencing Solutions—predominantly Next-Generation Sequencing (NGS)—dominate because they have transitioned from research tools to the undisputed standard of care in clinical diagnostics. This massive share is driven by the commercial explosion of liquid biopsy and Minimum Residual Disease (MRD) testing, where NGS is the only technology capable of the required sensitivity. Natera’s recent performance quantifies this dominance, reporting FY2024 revenue of $1.69 billion (up 56%) fueled by processing over 3 million tests. This volume surge is directly linked to Medicare (CMS) reimbursement for NGS-based colorectal and bladder cancer surveillance, proving that NGS is now a reimbursable clinical necessity.

Similarly, Guardant Health’s growth in the genomic testing market, driven by its "Shield" blood test, confirms that NGS has effectively displaced older technologies like microarrays in high-volume markets. The 66.73% share is further secured by the obsolescence of single-gene testing in oncology; clinicians now demand Comprehensive Genomic Profiling (CGP) panels to screen for hundreds of mutations (e.g., KRAS, EGFR) simultaneously. Major reference labs like LabCorp and Quest Diagnostics have standardized these NGS workflows, ensuring that the vast majority of diagnostic spending flows exclusively through this segment.

Drug Development Leads Revenue via Genomic Target Validation and Clinical Trial De-Risking

The Drug Development and Discovery application captures over 46% of global genomic testing market revenue, cementing its position as the primary financial engine of the market. This dominance exists because the pharmaceutical sector relies on genomic data as the principal risk-mitigation tool for multi-billion dollar R&D pipelines. Operating on the "5R Framework," the industry has accepted that genetic evidence doubles the probability of clinical success. Regeneron Pharmaceuticals exemplifies this investment; their Regeneron Genetics Center (RGC) has sequenced over 3 million exomes, a database that in 2024 delivered over 30 validated drug targets directly into their clinical pipeline, fundamentally altering discovery economics.

The segment prominence is further bolstered by high-value "companion diagnostic" collaborations. AstraZeneca credits its oncology success to biomarker-driven patient stratification, which requires extensive genomic testing during trials to identify "super-responders." Companies in the genomic testing market like GSK continue to leverage large-scale data mining partnerships to identify synthetic lethality targets. The sheer capital deployed by pharma for these "biomarker-guided" trials—which cost significantly less per successful approval than non-genomic trials—ensures that drug development remains the highest volume application, as the cost of genomic testing is negligible compared to the catastrophic cost of a failed Phase III trial.

Customize This Report + Validate with an Expert

Access only the sections you need—region-specific, company-level, or by use-case.

Includes a free consultation with a domain expert to help guide your decision.

Stem Cell Techniques Rely on Mandated Genomic Safety Testing for Regulatory Approval

The Stem Cell Therapy technique with a substantial 42.4% share is dominant in the genomic testing market because genomic testing is a strict regulatory mandate, not an optional step, in the manufacturing of Cell and Gene Therapies (CGT). This market share is driven by the FDA’s finalized guidance on human gene therapy products, which explicitly requires sensitive genomic techniques to detect "off-target" edits and chromosomal rearrangements before any therapy reaches a patient. Without this genomic verification, therapies are legally barred from release, making this testing an unavoidable industrial bottleneck.

The commercial weight of the segment in the genomic testing market is visible in the production of approved therapies like Vertex Pharmaceuticals’ Casgevy. To ensure patient safety, Vertex must utilize high-resolution genomic testing to prove that CRISPR editing did not accidentally trigger tumorigenic mutations. Consequently, the "stem cell" segment operates as an industrial-scale consumer of genomic testing for Quality Control (QC). With a global pipeline of over 2,000 active cell therapy clinical trials, every single therapeutic batch manufactured requires this rigorous testing, creating a mandatory, volume-based demand that guarantees this segment’s significant portion of the market.

To Understand More About this Research: Request A Free Sample

Regional Analysis

Where is Demand Most Concentrated Geographically?

North America currently commands the largest share 35% share of the genomic testing market, driven by a favorable reimbursement environment and high healthcare spending. The US market is bolstered by the presence of major industry players and robust government funding, such as the NIH's All of Us Research Program, which released data on 633,000 participants by February 2025. However, the Asia-Pacific region is the fastest-growing frontier. China’s aggressive "Healthy China 2030" initiative is pouring billions into precision medicine, while India is seeing a surge in demand for infectious disease testing and prenatal screening.

Asia Pacific: The High-Velocity Growth Engine of Global Genomics

Asia Pacific is aggressively outpacing Western markets, establishing itself as the fastest-growing region in the genomic testing market. The region's expansion is anchored by China’s "Healthy China 2030" initiative, which has funneled billions into precision medicine to mitigate rising cancer burdens. India is simultaneously emerging as a genomic powerhouse, validated by the Department of Biotechnology’s successful completion of sequencing 10,000 genomes for the Genome India Project by early 2024.

Shenzhen-based BGI Genomics continues to disrupt global pricing structures, making high-throughput sequencing accessible across emerging economies. Furthermore, advanced markets like Japan and South Korea are witnessing a surge in regulatory approvals for liquid biopsy tests, directly boosting oncology segment revenues. With a massive population base driving unprecedented demand for Non-Invasive Prenatal Testing (NIPT) and infectious disease surveillance, Asia Pacific is shifting the global volume center of gravity Eastward, offering lucrative opportunities for stakeholders seeking high-yield expansion.

Europe Remains A Stronghold For Biobanking and Population Genomics

The UK’s NHS Genomic Medicine Service is the most advanced national integration of genomic testing market in the world, having issued 29,639 rare disease reports by March 2024. Meanwhile, countries like South Korea and Japan are rapidly adopting liquid biopsy technologies. While the US leads in revenue generation, the sheer population size of Asian markets suggests that the center of gravity for volume may shift Eastward in the coming decade.

Recent Developments in Genomic Testing Market

- Genomics plc launched Health Insights nationwide in Great Britain on June 17, 2025, a UKCA-marked predictive tool for diseases like cardiovascular issues, type 2 diabetes, breast, and prostate cancer, partnering with Bupa and Spire Healthcare.

- Illumina, Inc. released its 5-base solution on October 15, 2025, enabling simultaneous genomic variant and DNA methylation detection from one sample to advance multiomic research.

- NeoGenomics announced preliminary Q4 and full-year 2025 revenue growth on January 11, 2026, projecting $727 million total, highlighting oncology-focused genomic testing expansion.

- NeoGenomics presented a real-world study on comprehensive genomic profiling for myeloid malignancies at ASH 2025 on December 8, 2025, featuring next-gen DNA/RNA sequencing.

- GeneDx (via Revvity signals) released ultraRapid whole genome sequencing for newborns in March 2025, delivering results in under 55 hours from blood spots.

Top Companies in Global Genomic Testing Market:

- Agilent Technologies, Inc.

- BGI Group

- Bio-Rad Laboratories

- Danaher Corporation

- Eurofins Genomics

- F. Hoffmann-La Roche

- Illumina, Inc.

- QIAGEN

- Singular Genomics Systems, Inc.

- Thermo Fisher Scientific, Inc.

- Other Prominent players

Market Segmentation Overview:

By Offering:

- System and Software

- Reagents & Consumables

- Services

- DTC Genomic Testing Service

- Sale of genomic data

By Testing Type:

- Sequencing Solution

- DNA Sequencing

- RNA Sequencing

- Methylation Sequencing

- NGS Library Preparation

- Sequencing Data Analysis

- Others

- Microarray Solution

- Human Genotyping with Arrays

- Non-Human Genotyping with Arrays

- Methylation Array Analysis

- Microarray Data Analysis

- Others

By Technology:

- Proteomics

- Pharmacogenomics

- Stem Cell Therapy

- Cloning

By Indication:

- Cancer

- Asthma

- Diabetes

- Hearth Diseases

- Other Indication

By Application:

- Drug Discovery & Development

- Disease Diagnosis

- Agricultural Production

- Others

By End-User:

- Hospitals & Clinics

- Research Centers & Academic Institutions

- Pharmaceutical & Biotechnology Companies

- Others

By Region:

- North America

- The U.S.

- Canada

- Mexico

- Europe

- Western Europe

- The UK

- Germany

- France

- Italy

- Spain

- Rest of Western Europe

- Eastern Europe

- Poland

- Russia

- Rest of Eastern Europe

- Western Europe

- Asia Pacific

- Malaysia

- Thailand

- China

- India

- Japan

- Australia & New Zealand

- South Korea

- ASEAN

- Rest of Asia Pacific

- Middle East & Africa (MEA)

- Saudi Arabia

- South Africa

- UAE

- Rest of MEA

- South America

- Argentina

- Brazil

- Rest of South America

REPORT SCOPE

| Report Attribute | Details |

|---|---|

| Market Size Value in 2025 | US$ 16.62 Billion |

| Expected Revenue in 2035 | US$ 41.34 Billion |

| Historic Data | 2020-2024 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Unit | Value (USD Bn) |

| CAGR | 9.54% |

| Segments covered | By Offering, By Testing Type, By Technology, By Indication, By Application, By End-User, By Region |

| Key Companies | Agilent Technologies, Inc., BGI Group, Bio-Rad Laboratories, Danaher Corporation, Eurofins Genomics, F. Hoffmann-La Roche, Illumina, Inc., QIAGEN, Singular Genomics Systems, Inc., Thermo Fisher Scientific, Inc., Other Prominent players |

| Customization Scope | Get your customized report as per your preference. Ask for customization |

FREQUENTLY ASKED QUESTIONS

The global market was valued at USD 16.62 billion in 2025. It is projected to attain a valuation of USD 41.34 billion by 2035, growing at a robust CAGR of 9.54% during the forecast period (2026-2035).

Next-Generation Sequencing (NGS) stands as the undisputed market leader, accounting for a market share exceeding 66.73%. Its dominance is driven by its ability to deliver high-throughput, cost-efficient sequencing, becoming the standard of care for oncology and liquid biopsy applications.

Drug development and discovery generate the highest revenue, accounting for over 46% of the global market. Pharmaceutical companies utilize genomic data to validate drug targets and de-risk clinical trials, making it essential for reducing R&D failure rates.

The reagents and consumables segment holds 46.7% of the market share. This dominance is sustained by a razor-and-blade business model, where installed instruments generate continuous, high-margin demand for proprietary chemical kits and flow cells.

North America leads the global market with a 35% share, supported by favorable reimbursement frameworks and large-scale government initiatives like the NIH’s All of Us program. However, Asia Pacific remains the fastest-growing region due to aggressive precision medicine investments.

With cancer causing 20 million new cases annually, oncology is the primary catalyst for demand. Clinicians are shifting toward genomic profiling to identify biomarkers for targeted therapies, making testing indispensable for managing chronic conditions like cancer and diabetes.

LOOKING FOR COMPREHENSIVE MARKET KNOWLEDGE? ENGAGE OUR EXPERT SPECIALISTS.

SPEAK TO AN ANALYST

.svg)

Features | Type of License | ||||

Data Book | Single User |   Multi User | Corporate | ||

| e-Access | ✓ | ✓ | ✓ | ✓ | |

User Sharing | 1 User Only | 1 User Only | Up to 7 Users | Unlimited User Access | |

⨉ | ⨉ | ⨉ | ✓ | ||

Free Customization | No Free Customization | Up To 30 hrs work | Up To 60 hrs work | Up To 80 hrs work | |

Deliverable |

| ⨉ | ✓ | ✓ | ✓ |

| ✓ | ⨉ | ✓ | ✓ | |

| ⨉ | ⨉ | ⨉ | ✓ | |

Analyst Support | 2-Months Analyst Support | 4-Months Analyst Support | 7-Months Analyst Support | One Year Analyst Support | |

Free Report update in next update cycle | ⨉ | ⨉ | ⨉ | ✓ | |

Free Industry Update (Within 180 days) | ⨉ | ⨉ | ⨉ | ✓ | |

Benefit | Up to 10% off on Post Purchase | Up to 20% off on Post Purchase | Up to 30% off on Post Purchase | Up to 40% off on Post Purchase | |