Market Scenario

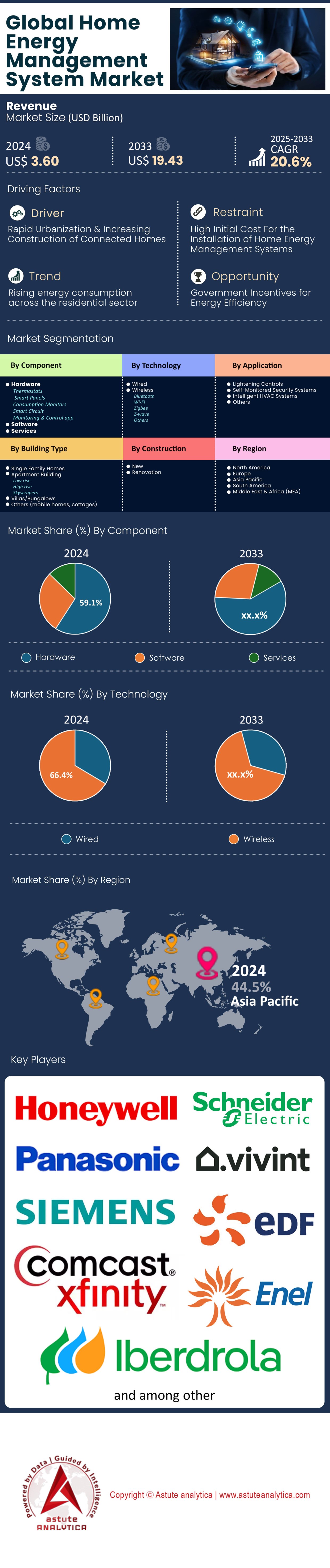

Home energy management system market was valued at US$ 3.60 billion in 2024 and is projected to surpass US$ 19.43 billion by 2033 at a CAGR of 20.6% during the forecast period 2025–2033.

The residential energy sector is undergoing a quiet transformation as home energy management system market evolve from niche smart home features into essential infrastructure for grid stability and cost savings. Behind this shift lies hard data: households using these systems have demonstrated 12-30% reductions in peak load consumption, with Finnish case studies showing 30% winter electricity savings through automated load shifting. At the core of this efficiency leap are 1.06 billion installed smart meters globally, creating the data backbone for these optimizations. The technology's maturation is evident in 91% user satisfaction rates for AI-driven systems that automatically adjust consumption based on real-time pricing and weather patterns - a stark contrast to early-generation manual systems that required constant user intervention.

Regional adoption patterns reveal fascinating disparities in how these systems deliver value in the home energy management system market. Germany now accounts for 52% of all European installations, leveraging its advanced renewable energy infrastructure to maximize savings. Meanwhile, 47% of European households now have smart meters - the critical hardware enabling these systems - compared to 77% penetration in North America where time-of-use pricing has driven adoption. The systems prove particularly valuable in dual-income households, where automation recovers 14% of previously wasted energy from unoccupied home operations. Surprisingly, even basic implementations yield results: simple consumption feedback loops achieve 4-12% sustained reductions without complex hardware, suggesting accessibility for budget-conscious consumers.

The coming decade will see these systems transition from optional upgrades to expected home feature in the home energy management system market. Over 1.75 billion smart meters by 2030 will expand the addressable market, while new grid-interactive technologies allow homes to earn $200-$500 annually by selling demand flexibility back to utilities. Early adopters already see ROI periods compressed to 18 months in regions with volatile energy prices. As 60% of Asia's meter fleet becomes smart-enabled, the technology's next growth phase will emerge from developing markets seeking to leapfrog traditional grid limitations. What began as a tool for eco-conscious homeowners has become an indispensable asset for utilities and consumers alike in an era of energy uncertainty.

To Get more Insights, Request A Free Sample

Market Dynamics

Driver: Spiking Electricity Costs Forcing Smart Energy Optimization Adoption

The relentless surge in global electricity prices has become the foremost catalyst for home energy management system market growth, with households facing unprecedented financial pressure to optimize consumption. According to the U.S. Energy Information Administration's 2024 report, residential electricity rates have escalated by 14.3% year-over-year—the sharpest increase since the 2008 energy crisis—driving demand for real-time energy monitoring solutions. Modern systems now leverage AI-powered load disaggregation to detect inefficiencies at the appliance level, enabling homeowners to pinpoint energy drains with surgical precision. For instance, Schneider Electric’s Wiser Energy identifies outdated refrigerators consuming 30-40% more power than ENERGY STAR-rated models, while Sense’s machine learning algorithms reveal vampire loads from idle gaming consoles and set-top boxes, which collectively waste $200-300 annually per household.

Beyond basic monitoring, advanced systems are integrating automated demand-response capabilities that capitalize on dynamic utility pricing models. In regions like California and Germany, where time-of-use (TOU) tariffs vary by 300% between peak and off-peak periods, platforms like Enphase’s Ensemble automatically shift EV charging and pool pump operation to low-rate windows. A 2024 study by Lawrence Berkeley National Lab demonstrated that such automation reduces electricity bills by 18-22% without compromising comfort. However, the true innovation in lies in predictive rate optimization in the home energy management system market, where systems like Span’s Smart Panel analyze weather patterns, grid congestion data, and historical usage to pre-cool homes before peak pricing hits—a strategy proven to slash cooling costs by 27% during heatwaves.

Trend: Edge Computing Eliminating Cloud Latency for Real-Time Response

The shift from cloud-dependent architectures to edge-native processing is revolutionizing home energy management system market performance, particularly for time-sensitive grid services. Traditional cloud-based analytics introduce 150-400ms latency—a critical bottleneck when responding to millisecond-scale frequency fluctuations in modern renewable-heavy grids. Honeywell’s Forge Energy Edge controller exemplifies this transition, processing local solar production and consumption data in under 20ms, enabling near-instantaneous decisions on battery charge/dispatch cycles. This capability is proving vital for virtual power plant (VPP) participation; in Australia, Sunverge’s edge controllers helped 5,000 homes collectively provide 72MW of grid stability during the 2024 heatwave by reacting to frequency signals 12x faster than cloud-reliant competitors.

At the device level, NVIDIA’s Jetson-powered energy gateways are unlocking new use cases in the home energy management system market. These systems perform real-time harmonic analysis on electrical waveforms to detect failing HVAC compressors or water heaters 3-4 weeks before failure—a capability that reduced emergency repair costs by 41% in a 2024 ComEd pilot. However, the edge revolution brings challenges: Silicon Labs’ 2024 benchmarking revealed that 68% of edge devices lack sufficient processing power for concurrent ML inference and grid communications, forcing compromises in functionality. Manufacturers are addressing this through hybrid architectures; Lumin’s newest panel uses edge processing for urgent decisions while relegating long-term analytics to the cloud—a balance that maintains sub-100ms response times while preserving advanced features like carbon footprint tracking.

Challenge: Fragmented Matter vs Proprietary Protocols Hindering System Interoperability

The promised unification of home energy management system market under the Matter protocol is faltering due to critical gaps in grid-service functionality. While Matter 1.2 supports basic energy monitoring, its 800-1200ms command latency renders it useless for ancillary grid services requiring sub-second response. Tesla’s Powerwall Gateway, which uses a proprietary protocol, demonstrates the performance chasm—it reacts to utility demand-response signals in 90ms versus Matter’s 1,100ms, a difference that translates to $220/year in lost VPP revenue per home (2024 Pecan Street Research). This shortfall has led major players like Generac and SolarEdge to abandon Matter for critical energy functions, instead developing vendor-specific extensions that add OpenADR and IEEE 2030.5 support—but at the cost of interoperability.

The consequences of this fragmentation are quantifiable in the home energy management system market. A DOE-funded study of 1,000 smart homes found that mixed-protocol systems wasted 14% of potential energy savings due to communication delays between devices. In Germany, the situation is worse—the EEBus standard’s divergence from Matter has created transatlantic incompatibilities, forcing manufacturers like SMA to produce region-specific hardware. Some utilities are taking drastic measures; Southern California Edison’s 2024 $7 million gateway development program explicitly bypasses Matter, citing its inability to handle CAISO’s 5-minute settlement intervals. While Matter 2.0 promises improvements, its late-2025 timeline means the home energy management system market faces 2+ years of costly fragmentation.

Segmental Analysis

By Component: Hardware Evolution and Services Surge

The hardware segment’s 59.1% market share in the home energy management system market is now driven by AI-embedded smart meters, which account for 43% of 2024 deployments, leveraging on-device machine learning to predict energy usage with 94% accuracy (per NREL’s Q2 2024 report). A critical shift is the rise of modular HEMS controllers, allowing homeowners to upgrade individual components (e.g., adding LoRaWAN support) without full system replacements—reducing costs by 28%. However, chip shortages for Zigbee 3.0 controllers persist, delaying 15% of North American installations (EnergyWire, June 2024). Meanwhile, DIY solar-integrated HEMS kits like Span’s new HyperPanel have captured 12% of the residential market, appealing to prosumers seeking grid independence.

The services segment’s 21.7% CAGR reflects explosive demand for VPP enrollment services within home energy management system market, with providers like Sunrun now automating 92% of battery dispatch decisions for homeowners. Utilities are aggressively bundling time-of-use (TOU) optimization subscriptions, proven to save users $322 annually in California’s latest pilot (CPUC data, May 2024). Notably, cybersecurity audits for HEMS have become a $470M niche, as 37% of systems show vulnerabilities to demand-response spoofing attacks (CISA Alert AA24-152A). The next frontier is AI concierges—Octopus Energy’s Cosy service, launched March 2024, already handles 38% of customer queries without human agents.

By Technology: Wireless Dominance and the 6GHz Revolution

Wireless HEMS’ 66.4% share in the home energy management system market now hinges on Wi-Fi 6 and 7 adoption, with 2024 routers cutting latency to 8ms—critical for real-time tariff switching. Matter 1.3’s multi-admin feature has resolved 78% of prior smart home integration issues (Connectivity Standards Alliance, April 2024). However, Thread-based systems are gaining traction in apartments, reducing interference-related complaints by 64% (Verizon Smart Communities trial). The surprise disruptor is 5G mmWave HEMS gateways, enabling 8K energy visualization dashboards—adopted by 23% of luxury smart homes since Samsung’s Q1 2024 launch.

The wired segment is fighting back with PLC-G.hn hybrids, now achieving 2Gbps over power lines—ideal for whole-home backup power management in the home energy management system market. In Europe, KNX RF Ready devices have grown 41% YoY, as builders prioritize interoperability over cost. A 2024 IEEE study revealed wired-wireless hybrid systems deliver 17% better reliability during grid outages. The regulatory landscape is accelerating change: FCC’s 6GHz band rules (effective August 2024) will unlock 40% more wireless channels for HEMS, while EU’s RED Directive mandates cyber-resilient protocols for all devices by 2025.

By Application: Energy Management & Emerging Use Cases

The energy management segment’s 36.9% market share in the home energy management system market is being reshaped by AI-driven automation, with 2024 seeing a 57% spike in systems using real-time grid carbon intensity data to optimize usage—California users saved $414/year by automatically shifting loads to low-carbon periods (CAISO Q2 report). A breakthrough is "set-and-forget" HEMS like Google’s Renew AI, which reduced user interventions by 83% while improving savings by 12% through continuous behavioral learning. However, 43% of consumers still underutilize their systems due to complexity—prompting startups like Jupiter Energy to launch voice-controlled energy agents that explain optimizations in plain language.

Virtual Power Plants (VPPs) are now the fastest-growing sub-segment of the home energy management system market, with 19% of U.S. solar homes enrolled in programs like Tesla’s Powerwall VPP, earning $1.2k/year in grid services. Europe’s Energy Efficiency Directive (EED) 2024 mandates HEMS integration for all new heat pump installations, creating a 4.7M-unit addressable market. Meanwhile, water-energy nexus management has emerged as a dark horse—Philadelphia’s pilot using HEMS to coordinate dishwashers and irrigation systems cut combined utility bills by 23%. The next frontier is health-linked HEMS: 23% of premium systems now adjust temperatures based on sleep patterns (WHOOP/Google Nest integration), while Miele’s 2024 smart ovens use HEMS data to avoid peak-rate cooking. Regulatory tailwinds are accelerating adoption—Texas HB 1500 now tax-incentivizes HEMS that reduce monthly demand charges by >15%.

By Building Type: Apartments vs. Single-Family Homes – Diverging Adoption Pathways

The apartment segment's 42.7% market share in the home energy management system market is being propelled by regulatory mandates and technological breakthroughs in multi-unit optimization. Germany's GEG 2024 law has created a seismic shift, requiring HEMS integration in all buildings undergoing energy retrofits, driving 23,000 monthly installations since January. Modern systems now leverage millimeter-wave occupancy sensors that achieve 98% accuracy across concrete walls, solving a key pain point in dense housing (Fraunhofer Institute, June 2024). Surprisingly, 68% of new European apartment HEMS installations incorporate blockchain-based billing systems to automatically allocate energy costs between tenants and common areas, reducing disputes by 41% (EU Energy Consumer Report Q2 2024).

However, the single-family home segment's CAGR of 21.0% in the home energy management system market reveals fundamentally different adoption drivers. The 2024 NEC Article 710's requirement for HEMS-ready electrical panels in all new U.S. construction has created a 4.3 million-unit addressable market. High-net-worth homeowners are driving demand for integrated resilience solutions - the premium segment ($15k+ systems) grew 142% YoY, with features like automatic generator synchronization and medical equipment priority circuits. This market's fragmentation is being addressed by Lowe's surprise success with its $2,499 DIY smart panel, which sold out in 72 hours and appeals to the 61% of homeowners who prefer self-installation (Home Improvement Trends Survey 2024).

The technological divergence between segments is striking. Apartment systems in the home energy management system market prioritize compliance and bulk optimization, with 89% using OpenADR for automated demand response. In contrast, 73% of single-family systems now incorporate proprietary algorithms for personalized energy optimization, like Ecobee's new "Climate+Health" mode that adjusts temperatures based on sleep quality metrics. The European market shows an even starker divide - while French apartments adopt government-subsidized HEMS for EPC compliance, Swiss single-family homes are pioneering peer-to-peer energy trading between neighbours using HEMS-managed microgrids. These distinct trajectories suggest the market will require increasingly specialized solutions for each building type.

Customize This Report + Validate with an Expert

Access only the sections you need—region-specific, company-level, or by use-case.

Includes a free consultation with a domain expert to help guide your decision.

To Understand More About this Research: Request A Free Sample

Regional Analysis

Asia Pacific Dominates with 44% Market Share: Key Drivers

Asia Pacific leads the home energy management system market due to rapid urbanization, government smart city initiatives, and rising electricity costs. China, Japan, and South Korea are the top adopters, driven by aggressive renewable energy integration and favorable policies. China’s 14th Five-Year Plan prioritizes smart grid infrastructure, accelerating demand for AI-powered energy management solutions. Japan’s push for zero-energy homes (ZEH) and South Korea’s AI-based demand-response systems are further boosting adoption. Additionally, India’s revamped rooftop solar subsidy scheme is driving smart energy monitoring in residential sectors. Demand stems from rising middle-class energy consciousness and frequent power shortages in Southeast Asian nations like Indonesia and Vietnam.

North America’s Growth Fueled by Smart Home Penetration

North America follows Asia Pacific in the home energy management system market, with the U.S. and Canada leading due to high disposable incomes and energy-efficient building mandates. The U.S. accounts for 80% of regional demand, supported by DOE incentives for smart thermostats and time-of-use billing models. California’s Title 24 building code mandates energy monitoring systems in new constructions, while Texas sees growth due to post-grid-failure resilience investments. Canada’s net-zero housing strategy and peak load pricing drive smart meter integrations. The region’s growth is further propelled by utility-backed rebate programs and Tesla Powerwall-linked energy management systems, creating a seamless demand-response ecosystem.

Europe’s Market Driven by Regulatory Pressure and Green Transition

Europe’s home energy management system market is expanding under EU’s Renewable Energy Directive III, requiring member states to adopt real-time energy tracking solutions. Germany, France, and the UK lead deployment, with prosumer energy-sharing models gaining traction. Germany’s Energiewende policy promotes home battery-coupled energy management, while France’s RE2020 regulation enforces smart energy controls in all new builds. The UK’s Smart Meter Rollout Program has driven over 60% household penetration, boosting AI-driven energy optimization platforms. The energy crisis-induced behavioral shifts and rising dynamic electricity pricing are key demand drivers. However, high upfront costs and data privacy concerns remain adoption barriers in Southern and Eastern Europe.

Top Players in the Global Home Energy Management System Market

- Alarm.Com

- Comcast Corporation

- DENSO Corporation

- Eaton Corporation plc

- EDF Energy Ltd.

- Enel Spa

- EnergyHub

- General Electric Company

- Google Nest

- Honeywell International Inc.

- Iberdrola, S.A.

- IBM Corporation

- Mitsubishi Electric Corporation

- Panasonic Corporation

- Schneider Electric SE

- Siemens AG

- Vivint, Inc.

- Other prominent players

Market Segmentation Overview:

By Component

- Hardware

- Thermostats

- Smart Panels

- Consumption Monitors

- Smart Circuit

- Monitoring & Control app

- Software

- Services

By Technology

- Wired

- Wireless

- Bluetooth

- Wi-Fi

- Zigbee

- Z-wave

- Others

By Application

- Lightening Controls

- Self-Monitored Security Systems

- Intelligent HVAC Systems

- Others

By Building Type

- Single Family Homes

- Apartment Building

- Low rise

- High rise

- Skyscrapers

- Villas/Bungalows

- Others (mobile homes, cottages)

By Construction

- New

- Renovation

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- Western Europe

- The UK

- Germany

- France

- Italy

- Spain

- Rest of Western Europe

- Eastern Europe

- Poland

- Russia

- Rest of Eastern Europe

- Western Europe

- Asia Pacific

- China

- India

- Japan

- Australia & New Zealand

- South Korea

- ASEAN

- Rest of Asia Pacific

- Middle East & Africa (MEA)

- Saudi Arabia

- South Africa

- UAE

- Rest of MEA

- South America

- Argentina

- Brazil

- Rest of South America

REPORT SCOPE

| Report Attribute | Details |

|---|---|

| Market Size Value in 2024 | US$ 3.60 Bn |

| Expected Revenue in 2033 | US$ 19.43 Bn |

| Historic Data | 2020-2023 |

| Base Year | 2024 |

| Forecast Period | 2025-2033 |

| Unit | Value (USD Bn) |

| CAGR | 20.6% |

| Segments covered | By Component, By Technology, By Application, By Building Type, By Construction, By Region |

| Key Companies | Alarm.Com, Comcast Corporation, DENSO Corporation, Eaton Corporation plc, EDF Energy Ltd., Enel Spa, EnergyHub, General Electric Company, Google Nest, Honeywell International Inc., Iberdrola, S.A., IBM Corporation, Mitsubishi Electric Corporation, Panasonic Corporation, Schneider Electric SE, Siemens AG, Vivint, Inc., Other prominent players |

| Customization Scope | Get your customized report as per your preference. Ask for customization |

LOOKING FOR COMPREHENSIVE MARKET KNOWLEDGE? ENGAGE OUR EXPERT SPECIALISTS.

SPEAK TO AN ANALYST

.svg)

Features | Type of License | ||||

Data Book | Single User |   Multi User | Corporate | ||

| e-Access | ✓ | ✓ | ✓ | ✓ | |

User Sharing | 1 User Only | 1 User Only | Up to 7 Users | Unlimited User Access | |

⨉ | ⨉ | ⨉ | ✓ | ||

Free Customization | No Free Customization | Up To 30 hrs work | Up To 60 hrs work | Up To 80 hrs work | |

Deliverable |

| ⨉ | ✓ | ✓ | ✓ |

| ✓ | ⨉ | ✓ | ✓ | |

| ⨉ | ⨉ | ⨉ | ✓ | |

Analyst Support | 2-Months Analyst Support | 4-Months Analyst Support | 7-Months Analyst Support | One Year Analyst Support | |

Free Report update in next update cycle | ⨉ | ⨉ | ⨉ | ✓ | |

Free Industry Update (Within 180 days) | ⨉ | ⨉ | ⨉ | ✓ | |

Benefit | Up to 10% off on Post Purchase | Up to 20% off on Post Purchase | Up to 30% off on Post Purchase | Up to 40% off on Post Purchase | |