Market Scenario

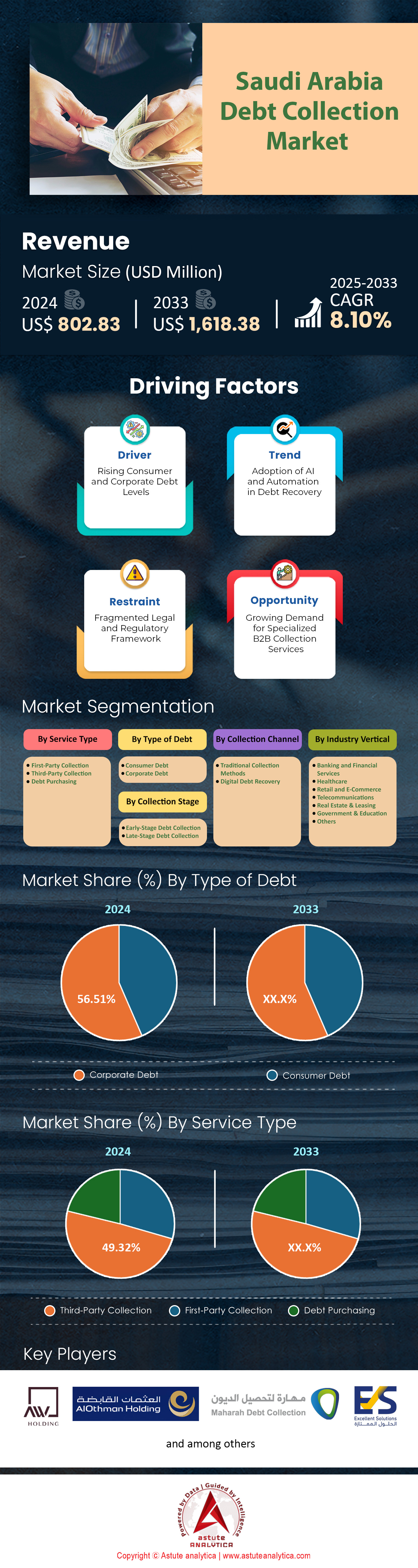

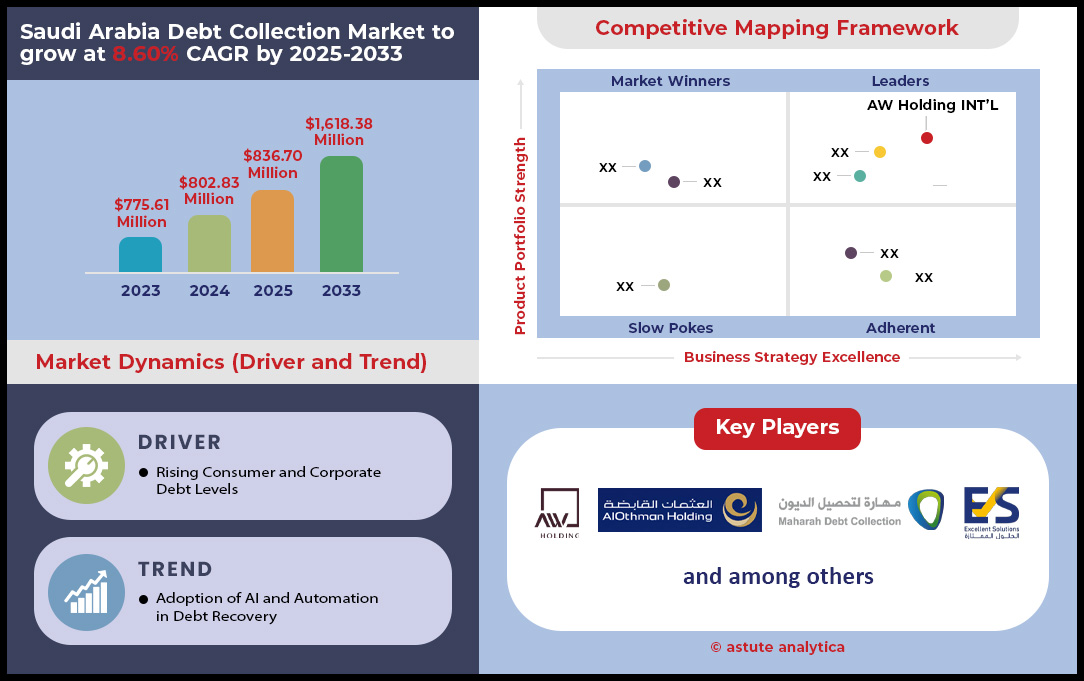

Saudi Arabia debt collection market was valued at US$ 802.83 million in 2024 and is projected to hit the market valuation of US$ 1,618.38 million by 2033 at a CAGR of 8.10% during the forecast period 2025–2033.

The Saudi Arabian economy is currently navigating a period of historic credit expansion, creating a fertile and compelling landscape for the debt collection market. With total bank credit surging past SAR 3.1 trillion in early 2025 and claims on the private sector reaching a record SAR 2.89 trillion, the sheer volume of outstanding debt is unprecedented. This is not a temporary spike but a sustained trend underpinned by the deep structural changes of Vision 2030. The parallel growth in both corporate and consumer lending forms a dual engine driving future demand for recovery services. As this immense portfolio of new debt matures, a corresponding rise in delinquencies and defaults is an inevitable and natural consequence, signalling a fundamental and long-term need for professional debt collection agencies.

The sophistication of this emerging debt collection market opportunity lies in its diversity. The demand is not monolithic; it spans from high-volume consumer portfolios, such as the SAR 27.25 billion in credit card loans, to the complex, high-value realm of corporate debt, including the SAR 883.3 billion in real estate loans. This multifaceted debt environment necessitates a move away from one-size-fits-all collection methods towards specialized, technology-driven strategies. Collection agencies equipped to handle the nuances of Sharia-compliant financing, intricate corporate restructuring, and sensitive retail collections will find themselves in an exceptionally strong position. The market is ripe for innovation, and firms that leverage data analytics and AI to enhance efficiency and compliance will capture a significant share of this burgeoning, high-potential sector.

Prominent & Key Findings in Saudi Arabia Debt Collection Market

- Historic Private Sector Indebtedness: Bank credit to the private sector reached an all-time high of SAR 2.79 trillion in January 2025, underscoring the massive scale of corporate and commercial borrowing that will require servicing and collection.

- Surging Household Debt: Total household debt in the Kingdom climbed to US$ 134.0 billion by the close of 2024, highlighting the vast and growing consumer market for debt collection services, from personal loans to credit cards.

- Real Estate as a Primary Debt Driver: The real estate sector represents the single largest pool of debt, with total loans from banks hitting a record SAR 883.3 billion by the end of 2024, driven heavily by individual mortgages.

- Rapid MSME Credit Expansion: In line with government priorities, credit facilities to Micro, Small, and Medium Enterprises (MSMEs) grew to SR 351.7 billion in 2024, creating a distinct and high-volume segment for specialized debt recovery.

- Robust Corporate Capital Market Activity: Saudi entities were dominant in the region's capital markets, raising a staggering US$ 79.5 billion from 79 primary bond and sukuk issuances in 2024, diversifying corporate liabilities beyond traditional bank loans.

- Concentrated Corporate Borrowing: Within the corporate sector, real estate activities command the largest share of debt, with borrowing reaching SR 374.5 billion by March 2025, indicating a key area of concentrated financial risk and collection opportunities.

To Get more Insights, Request A Free Sample

Top Trends Shaping the Saudi Arabian Debt Collection Market in 2025

- Accelerating Growth in Overall Bank Lending: The total volume of debt is rapidly expanding, with bank credit soaring to over SAR 3.126 trillion by April 2025. This sustained, large-scale growth continuously expands the fundamental base of receivables requiring collection services across the entire economy.

- Sustained Surge in Consumer and Credit Card Debt: Consumer borrowing remains robust, with total loans reaching SAR 479.78 billion in the first quarter of 2025. A key driver is credit card debt, which hit SR 30.66 billion, indicating a consistent, high-volume pipeline for retail collection agencies.

- Targeted and Rapid Expansion of MSME Lending: A dedicated focus on Micro, Small, and Medium Enterprises has pushed their total credit facilities to SR 351.7 billion by the end of 2024. This rapid expansion into a higher-risk segment is cultivating a specialized and fast-growing niche for debt recovery in the Saudi Arabia debt collection market.

- The Rise of Finance Companies as Major Lenders: Non-bank finance companies are emerging as significant lenders, with their total credit rising to SR 96.26 billion in 2024. Their aggressive expansion into retail segments like personal and auto finance is creating new and diverse pools of receivables.

- Deepening of the Domestic Sukuk and Bond Market: The domestic debt market is deepening significantly, with the total value of listed sukuk and bonds reaching approximately SAR 642 billion by the end of Q1 2025. This reflects consistent government and corporate issuance, diversifying the nature of outstanding debt.

- Improving Asset Quality Amidst a Lending Boom: Despite the lending boom, asset quality has improved, with the absolute value of non-performing loans falling to SAR 36.51 billion by Q3 2024. This unique dynamic suggests future collection efforts will target a larger but healthier base of debt, requiring more sophisticated recovery tactics.

Segmental Analysis

By Debt Type

The Saudi Arabian debt collection market landscape is overwhelmingly dominated by the corporate sector by capturing more than 56.51% market share, a direct consequence of the Kingdom's transformative Vision 2030. This ambitious economic diversification plan is fueling a massive wave of development and large-scale projects, necessitating a substantial increase in corporate financing. The sheer scale of this growth is evident in the corporate bond and sukuk market, which surged from $15.5 billion in the first quarter of 2020 to a remarkable $37 billion in the same period of 2025. With Vision 2030 projected to require approximately $1 trillion in total investments, the reliance on debt as a primary funding mechanism is set to intensify, creating a fertile ground for corporate debt collection activities. This boom in corporate finance is further highlighted by the Kingdom's leadership in the regional IPO market, where 42 listings in 2024 raised a total of $4.1 billion, signaling a vibrant and expanding corporate ecosystem.

This expansion is strategically supported by government policy and private sector engagement. The Saudi government's plan to run a budget deficit until 2030 to finance national projects underscores its commitment to debt-fueled growth. This is complemented by the "Shareek" program, which aims to galvanize large Saudi companies into contributing $1.3 trillion towards the investment drive. Consequently, a significant volume of corporate debt in the debt collection market is set to mature, with projections indicating approximately US$168 billion in Saudi bonds will mature between 2025 and 2029. The complexity is compounded by a rise in cross-border debt, which accounted for a significant portion of corporate recovery cases in 2024. While a new investment law that reduces licensing decisions from 30 to just five days fosters a business-friendly environment, the build-up of debt, particularly among unlisted private sector entities held by Saudi financial institutions, ensures that corporate debt collection will remain the market's primary and most dynamic segment for the foreseeable future.

- The need for corporate debt collection is escalating as projections show $168 billion in Saudi bonds will mature between 2025 and 2029.

- Corporate financing is booming, with bond and sukuk issuance skyrocketing to $37 billion in the first quarter of 2025 alone.

- The Vision 2030 initiative is projected to require an immense $1 trillion in investments, much of which will be debt-financed.

- Saudi Arabia's thriving corporate scene led the GCC with 42 IPOs in 2024, raising a substantial $4.1 billion.

- The government's "Shareek" program is designed to mobilize $1.3 trillion in investments from large domestic companies, further expanding corporate financial activities.

By Service Type

In a market characterized by increasing complexity, third-party debt collection services with over 49.32% revenue share are definitively leading the charge across Saudi Arabia debt collection market. Businesses are increasingly outsourcing their recovery activities to specialized agencies to leverage their expertise and maintain positive relationships with clients. This trend is bolstered by a clear and supportive regulatory framework established by the Saudi Central Bank (SAMA), which licenses all debt collection agencies, ensuring a professional and standardized approach. The legal system also facilitates this process, offering a simplified procedure for financial claims up to 20,000 riyals, which streamlines the recovery of smaller debts. The market is populated by highly capable firms, with leading agencies like AW Holding showcasing their significant resources by employing a team of over 190 specialists and consultants dedicated to recovery.

The value proposition of these agencies extends deep into legal proficiency and strategic execution in the debt collection market. For instance, prominent firms like Alwasl National Advocates and Legal Consultants employ a team of 18 lawyers, providing the legal firepower necessary for complex cases. Many of these agencies operate on a contingency fee basis, a model that aligns their interests with their clients by only charging upon successful debt recovery. This approach, combined with a core focus on preserving the crucial creditor-debtor relationship through professional conduct, makes outsourcing an attractive option. These agencies offer comprehensive, end-to-end services, managing the entire collection lifecycle. Their excellence is recognized within the industry, as demonstrated by Al Othman Law Firm being named "Corporate Law Firm of the Year 2025." Specialization is also a key trend, with agencies like Maharah Debt Collection focusing on specific sectors, proving that deep local expertise is paramount for navigating Saudi Arabia's unique cultural and legal nuances effectively.

- Leading collection agencies in the debt collection market are well-resourced, with firms like AW Holding boasting a team of over 190 specialists and consultants.

- The legal strength of these agencies is significant, with firms such as Alwasl National Advocates employing 18 lawyers to manage cases.

- A simplified legal procedure is in place for financial claims up to 20,000 riyals, accelerating the collection process for smaller amounts.

- The Saudi Central Bank (SAMA) provides robust oversight by formally licensing all debt collection agencies operating within the Kingdom.

- The industry's quality is recognized through accolades, such as Al Othman Law Firm being awarded "Corporate Law Firm of the Year 2025".

By Collection Stage

The operational center of gravity in Saudi Arabia's debt collection market is firmly situated in the late stage of the recovery cycle. This stage of recovery accounts for over 52.92% market share. This concentration is a result of a confluence of commercial practices, cultural norms, and protracted legal timelines. It is common commercial practice for debtors in the Kingdom to be granted generous payment terms, which frequently average 90 days or even longer. This inherently pushes a significant volume of receivables into a delayed status, making late-stage intervention a necessity rather than an exception. Once a debt becomes overdue, the formal legal process for recovery can be lengthy and complex. Pursuing a claim through the Board of Grievances, for example, can take as long as 12 months to reach a conclusion, a substantial period that solidifies the debt's position in the late-stage category.

The procedural timelines further entrench the debt collection market's focus on late-stage collection in the Saudi Arabia. Even after a favorable judgment is secured, the subsequent enforcement process can require an additional six months to complete. The legal framework itself contains multiple steps that extend the timeline; for instance, a debtor is given a 15-day period to contest a Payment Order. Once a case is filed in the enforcement court, the debtor has a further 21 days to settle the payment. Should the initial decision be contested, there is a 30-day window to file an appeal. Even before formal legal action commences, the pre-legal, amicable settlement phase can take between 7 and 14 days. If this fails, the process of filing a claim adds another 30 to 60 days, and obtaining a formal judgment can take a further 60 to 90 days, ensuring that by the time recovery is successful, the debt is firmly in the late stage.

- The formal legal process for debt recovery is lengthy, with proceedings in the Board of Grievances taking up to 12 months to conclude.

- Even after a judgment, the enforcement process itself can take an additional six months, prolonging the recovery cycle significantly.

- Commercial norms contribute to delays, with debtors frequently being granted generous payment terms that average 90 days or more.

- The legal framework provides debtors a 30-day window to file an appeal against a court's decision, adding another potential delay.

- Once a case reaches the enforcement court, the debtor is given a 21-day period to settle the outstanding payment.

By Collection Channel

The most transformative force shaping the Saudi debt collection market is the widespread adoption of digital recovery channels, a trend propelled by Vision 2030's emphasis on technological advancement. As a result, digital recovery channel capture over 60.02% market share. Digital methods are proving to be the most efficient and widely embraced approach, fundamentally altering how debts are managed and recovered. The fintech sector is a hotbed of innovation in this space, attracting significant investor confidence. This is powerfully illustrated by the AI-powered debt collection platform Ebra raising US$ 2 million in seed funding in early 2025, and the AI−driven debt resolution firm Clear Grids securing US$ 10 million in funding in March 2025. The broader financial ecosystem has already undergone a massive digital shift, with a staggering 10.8 billion digital payment transactions recorded in 2023, creating a digitally native consumer base receptive to online financial management, including debt resolution. The government's foresight in this area is notable, having established the "Sadad" e-payment system as early as 2009.

The momentum towards digital recovery in the debt collection market is supported by a robust and evolving infrastructure. In a move set to increase the demand for advanced collection software, Saudi Arabia appointed five new financial institutions as primary distributors of government debt instruments in July 2024. Government bodies are also leading by example, with the Ministry of Health implementing its own e-Payment Collection Service. The Saudi Central Bank is actively fostering this ecosystem through initiatives like the "Mada Atheer" contactless payment service and the overarching Financial Sector Development Program, which aims to expand digital payment options. The launch of a new instant payments system in 2021 further solidified the country's advanced digital payment capabilities. Major financial institutions are at the forefront of this evolution, with Al Rajhi Bank launching a sophisticated AI-driven platform in 2023 specifically to enhance its debt recovery processes, signaling a market-wide pivot to technology-driven efficiency.

- The scale of digitalization is immense, with Saudi Arabia debt collection market recording a total of 10.8 billion digital payment transactions in 2023.

- Investor confidence in digital debt solutions is high, with fintech firm ClearGrid securing $10 million in funding in March 2025.

- The AI-powered debt collection platform Ebra successfully raised $2 million in seed funding in early 2025, highlighting the focus on tech.

- In July 2024, the Kingdom appointed five new financial institutions as primary distributors of government debt, boosting the digital infrastructure.

- The government's commitment to digital payments was established early, with the "Sadad" e-payment system being launched back in 2009.

Customize This Report + Validate with an Expert

Access only the sections you need—region-specific, company-level, or by use-case.

Includes a free consultation with a domain expert to help guide your decision.

To Understand More About this Research: Request A Free Sample

10 Major Developments in Saudi Arabia Debt Collection Market

- Riyadh-based fintech Ebra, the first AI-powered debt collection company in the Middle East, secured a $2 million seed funding round in February 2025. Led by Seen Holding and Raz Holding, the investment will enhance its AI platform for ethical recovery and fund its expansion in the Kingdom.

- AI-driven debt resolution firm ClearGrid raised $10 million in March 2025 to fund its expansion into Saudi Arabia. The funding rounds were led by prominent investors including Raed Ventures, Beco Capital, and Nuwa Capital, with significant participation from Aramco's Waed Ventures and KBW Ventures.

- Scene Holding made a strategic investment in Ebra (Ibraa) in February 2025, aiming to support innovative, AI-driven financial solutions. This partnership aligns with Vision 2030's goal of advancing digital transformation in the financial sector.

- Since launching in 2024, ClearGrid has secured partnerships with major fintechs and banks in the MENA region, signing over 10 major enterprise clients. The company is now actively building its 2025 pipeline with a strategic focus on the Saudi Arabia debt collection market.

- The Saudi government appointed five new financial institutions as primary distributors for government debt instruments in July 2024. This move diversifies the investor base and is expected to fuel demand for advanced debt collection services and software.

- In March 2025, global MedTech firm Mölnlycke Health Care increased its stake to 60% in its joint venture with the Tamer Group. This expanded partnership, which includes developing a local factory, reinforces its long-term commitment to the Saudi market under Vision 2030.

- Aramco and Ma'aden, the Middle East's largest mining company, signed terms in January 2025 to form a joint venture. The partnership will focus on exploring and mining key energy transition minerals like lithium.

- Saudi Arabia saw robust M&A activity throughout 2024 and into the first half of 2025, driven by Vision 2030 and business-friendly reforms. Key sectors for deals included construction, real estate, and healthcare.

- Joint ventures have become an increasingly popular market entry strategy for foreign businesses in Saudi Arabia debt collection market. This is facilitated by recent regulatory easing and a new Saudi Companies Law that officially recognizes and enforces such agreements.

- The General Authority for Competition (GAC) is actively regulating economic concentrations. In the first quarter of 2025 alone, it reviewed 108 new notifications, of which 83% were acquisitions and 12% were joint ventures, reflecting a high volume of strategic market transactions.

Top Companies in the Saudi Arabia Debt Collection Market

- Al Madani & Co .

- AW Holding

- Alwasl National Debt Collection for Financing Entities Co .

- Oddcoll

- Baker Ing

- Maharah Debt Collection

- Saudi Debt Collection

- Unified Credit Solutions Pvt Ltd .

- Mutalabah

- Excellent Solutions

- TCM Group

- Cedar Financial

- Debt Works

- Credit Reform

- Eyad Reda Law Firm LLP

- Other Prominent Players

Market Segmentation Overview

By Type of Debt

- Consumer Debt

- Corporate Debt

By Service Type

- First-Party Collection

- Third-Party Collection

- Debt Purchasing

By Collection Stage

- Early-Stage Debt Collection

- Late-Stage Debt Collection

By Collection Channel

- Traditional Collection Methods

- Digital Debt Recovery

By Industry Vertical

- Banking and Financial Services

- Healthcare

- Retail and E-Commerce

- Telecommunications

- Real Estate & Leasing

- Government & Education

- Others

LOOKING FOR COMPREHENSIVE MARKET KNOWLEDGE? ENGAGE OUR EXPERT SPECIALISTS.

SPEAK TO AN ANALYST

.svg)

Features | Type of License | ||||

Data Book | Single User |   Multi User | Corporate | ||

| e-Access | ✓ | ✓ | ✓ | ✓ | |

User Sharing | 1 User Only | 1 User Only | Up to 7 Users | Unlimited User Access | |

⨉ | ⨉ | ⨉ | ✓ | ||

Free Customization | No Free Customization | Up To 30 hrs work | Up To 60 hrs work | Up To 80 hrs work | |

Deliverable |

| ⨉ | ✓ | ✓ | ✓ |

| ✓ | ⨉ | ✓ | ✓ | |

| ⨉ | ⨉ | ⨉ | ✓ | |

Analyst Support | 2-Months Analyst Support | 4-Months Analyst Support | 7-Months Analyst Support | One Year Analyst Support | |

Free Report update in next update cycle | ⨉ | ⨉ | ⨉ | ✓ | |

Free Industry Update (Within 180 days) | ⨉ | ⨉ | ⨉ | ✓ | |

Benefit | Up to 10% off on Post Purchase | Up to 20% off on Post Purchase | Up to 30% off on Post Purchase | Up to 40% off on Post Purchase | |