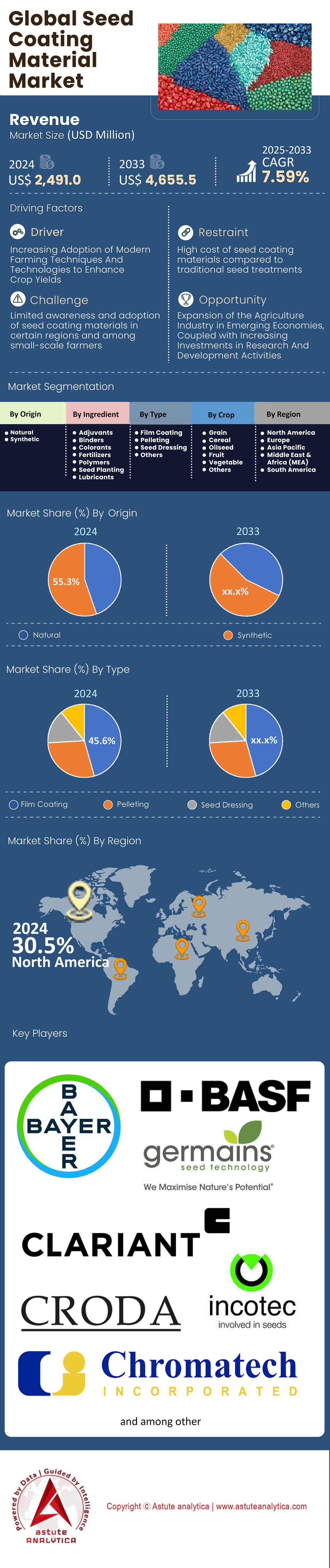

Market Snapshot

Seed coating material market was valued at US$ 2,491.0 million in 2024 and is projected to attain market valuation of US$ 4,655.5 million by 2033 at a CAGR of 7.59% during the forecast period 2025–2033.

Key Findings

- Based on ingredients, the global seed coating material market is dominated by polymers segment, commanding a significant 30.6% share.

- In terms of origin, synthetic segment is leading the market, holding a 55.30% share.

- Based on types, film coating segment leads the global market by type, holding a substantial 45.6% share.

- Based on crop, grains stand out as the leading segment, holding a 30.2% share.

- North America is market leader with over 30.50% market share.

The escalating demand for seed coating materials is best understood not as a simple agronomic trend but as a financial necessity to protect the most expensive input on the modern farm. The gravity of this market is illustrated by the sheer value of the seeds being treated. With major seed segments generating net sales in the range of $9.5 billion annually, the genetic assets inside the bag are too valuable to risk in the seed coating material market. Farmers in advanced economies, who now face seed costs averaging around $120 per acre for high-yield crops, view coating as a non-negotiable insurance policy. This investment protects against erratic weather and soil pathogens that threaten yield before the plant even emerges.

Furthermore, the rise in demand is directly correlated to the operational requirements of high-speed precision planters. These machines, operating at speeds exceeding 10 miles per hour, require polymer-coated seeds to prevent friction and ensure accurate singulation. Without advanced flowability coatings, the machinery simply cannot function at capacity, making the coating material as vital as the genetics themselves.

Trend: Great Material Shift to Biodegradable Solutions

The seed coating material market landscape is currently defined by a race against a regulatory clock that is fundamentally reshaping the chemistry of the industry. The standard synthetic polymers that have dominated the market for decades are facing extinction in key regions due to stringent microplastic restrictions. The industry is currently navigating a strict transition period that effectively mandates the phase-out of non-biodegradable seed coatings by October 2028. This regulatory pressure in the seed coating material market has forced a massive capital pivot toward bio-based polymers and flowability powders. Major material providers with turnovers in the $8 billion range have already commercialized new product lines designed to meet these compliance standards.

The demand is shifting aggressively from generic synthetic polymers to sophisticated, microplastic-free binders that can pass rigorous biodegradability tests—requiring 60% degradation in 28 days—without gumming up the delicate internal mechanisms of planting equipment.

Demand Analysis: Global Powerhouses Driving Volume and Innovation

The demand intensity varies significantly by geography in the global seed coating material market, dictated by specific agronomic engines and scale. Brazil stands as the undisputed volume leader globally. With soybean planting covering approximately 47.35 million hectares for the 2024/2025 season and treatment rates approaching 98%, the country represents the single largest concentrated volume of fungicide and insecticide coating demand on the planet. In contrast, the United States leads in value.

With corn planting covering roughly 90 million acres annually and seed bags often retailing above $300, the U.S. seed coating material market demands "stacked" coatings containing multiple biologicals and nematicides, driving higher revenue per treated ton than any other region. China is rapidly becoming a modernization engine as government initiatives to revitalize the seed industry drive a shift from farm-saved seed to commercial hybrids. Canada remains a stronghold for high-tech encrusting materials due to the small size of canola seeds, while India represents the growth frontier, with surging demand for polymer coatings to support the rapid hybridization of maize and paddy crops.

To Get more Insights, Request A Free Sample

Competitive Analysis: Industry Titans Consolidating Seed Coating Material Market Control

The competitive landscape is consolidated among massive integrated players who control both the seed genetics and the chemical treatment. Major entities like Corteva, with projected revenues exceeding $17 billion, have aggressively expanded their proprietary seed-applied technology divisions, viewing them as standalone growth engines. BASF is another dominant force, boasting a multi-billion euro innovation pipeline heavily weighted toward integrated seed treatments and traits.

On the specialized materials side, companies in the seed coating material market like Croda (Incotec) lead the charge in sustainable formulations, with data suggesting their technologies have contributed to saving over 160,000 hectares of land through yield efficiencies. Syngenta and Bayer round out the top tier, leveraging their massive chemical portfolios to lock in market share and drive the adoption of their specific coating protocols.

Extending Biological Shelf Life and Performance

The most critical recent development in the sector is the technological breakthrough in keeping biologicals alive on the seed surface. Historically, beneficial microbes would die within weeks when exposed to chemical treatments or ambient conditions. However, recent commercial launches in the 2024/2025 cycle have set a new benchmark, validating an on-seed shelf life of up to two years. This is a game-changing metric that allows biological-coated seeds—such as those carrying nitrogen-fixing bacteria—to move through the standard industrial supply chain without losing potency. Field trials have demonstrated that these advanced living coatings can deliver yield increases of 5% even when synthetic nitrogen fertilizer is reduced, effectively opening the door for a massive new category of bio-active coatings that function as living factories for the plant.

Opportunity Analysis: Unlocking Value in Climate Resilience and Emerging Markets

While pest protection is a mature segment of the seed coating material market, the untapped opportunity lies in climate resilience. There is currently a scramble to perfect hydrophilic coatings—polymers that actively attract and retain soil moisture around the seed zone. For dryland farmers in regions like the U.S. Great Plains and Australia, a coating that can lower the water potential required for germination could mean the difference between a successful harvest and crop failure.

Additionally, the retrofit market in developing nations is surging. As smallholder farmers in Africa and Southeast Asia gain access to hybrid seeds, there is an immediate, unmet need for low-cost, mobile seed treating equipment and compatible "pre-mix" polymer concentrates that can be applied at the village level, bridging the gap between subsistence farming and industrial agronomy.

Segmental Analysis

Polymer Innovations Driving Superior Seed Protection Performance

Polymers currently lead the seed coating material market with a 30.6% share because they offer unmatched binding capabilities and durability during transport. Recent technological strides have solidified their position, as seen when BASF launched the Flo-Rite Pro 02 polymer in 2024 to enhance seed flowability in automated planters. Such innovations allow farmers to plant thousands of acres with precision, reducing skips and doubles that cost yield. Seed coating material formulations rely on these advanced polymers to ensure that active ingredients like fungicides stay on the seed rather than dusting off into the environment.

Regulatory pressures are simultaneously reshaping the polymer landscape in the seed coating material market without diminishing its dominance. Covestro introduced Amulix biodegradable binding polymers in 2025 specifically to meet the stringent EU deadline of 2028 for removing microplastics. Manufacturers are rapidly pivoting to these compliant materials to maintain market access while preserving the protective benefits of traditional polymers. The Indian Institute of Seed Research also patented a new polymer composition in April 2025, further expanding the global toolkit for seed protection.

- Lallemand Plant Care released LALRISE SHINE DS in 2024 to improve root vigor.

- Nutreos debuted a plant-based polymer in January 2024 that fully degrades in soil.

- Milliken unveiled Milli Solum in 2025 to boost active ingredient retention.

Synthetic Formulations Retain Reliability Amidst Regulatory Shifts

Synthetic materials command a massive 55.30% share of the global seed coating material market due to their proven efficacy and established manufacturing infrastructure. Clariant demonstrated this scale by ramping up production of synthetic dispersants in 2024, ensuring that pesticide coatings remain stable and effective under harsh field conditions. Seed coating material of synthetic origin provides a consistent barrier against soil-borne pathogens that biological alternatives struggle to match in cost and performance. Farmers continue to favor these solutions for their reliability in protecting high-value genetically modified seeds.

Despite the push for sustainability, synthetic innovation remains vigorous and essential for global food security in the seed coating material market. BASF released a nano-encapsulated synthetic adjuvant in June 2024 that significantly improves the uptake of crop protection agents. Furthermore, the US EPA mandated new drift-reducing technologies in 2024, which has ironically boosted the demand for heavy synthetic encrusting to prevent chemical drift. Major players like Sumitomo Chemical expanded synthetic facilities in Argentina in early 2025 to meet this enduring demand.

- China registered 170 synthetic seed-treating manufacturers by May 2024.

- India approved five new synthetic molecules for cotton in the 2024 season.

- Corteva launched a synthetic nematicide coating for US soybeans in 2025.

Film Coating Precision Enhances Planting Efficiency Globally

Film coating technology leads the seed coating material market with a 45.6% share, driven by the need for precision agriculture and automated planting systems. Covestro expanded its film color palette to include red, orange, and blue in 2025, allowing farmers to visually distinguish between different trait stacks and treatments easily. Seed coating material applied via film ensures that the seed shape remains virtually unchanged, preventing clogs in high-speed planting equipment. This method significantly reduces dust, protecting both the operator and the environment from hazardous chemical exposure.

The adoption of film coatings has accelerated in major agricultural economies in the seed coating material market due to their compatibility with modern machinery. Brazil saw film coating usage surge as soybean production hit 169 million tons in the 2024/2025 season, requiring efficient processing of massive volumes. Incotec further advanced the technology by transitioning its vegetable portfolio to 100% microplastic-free films by 2024. Such advancements ensure that film coating remains the gold standard for delivering active ingredients directly to the seed surface without altering its weight.

- Precision Laboratories confirmed film coatings significantly reduced dust-off in 2024 trials.

- Germains Seed Technology launched an organic-compliant film coat in 2025.

- Centor Oceania introduced a high-opacity film coat in 2025 for better cosmetics.

Customize This Report + Validate with an Expert

Access only the sections you need—region-specific, company-level, or by use-case.

Includes a free consultation with a domain expert to help guide your decision.

Grain Crops Fueling Massive Volume Demand Worldwide

Grains dominate the seed coating material market with a 30.2% share because they represent the largest volume of planted acreage globally. Food security initiatives drove this demand, with India reporting a 6.5 lakh hectare increase in summer sowing areas for 2025, directly boosting the consumption of treated seeds. Seed coating material is vital for these crops to ensure uniform germination and early-stage protection against aggressive pests. The sheer scale of wheat, corn, and rice production necessitates cost-effective and scalable coating solutions that only the grains segment can command.

Strategic national programs are further cementing the leadership of grains in the seed coating material market. China initiated a Seed Revitalization Strategy in 2024 that explicitly focuses on advanced treatments for corn and wheat to secure domestic food supplies. Simultaneously, BioConsortia launched FixiN 33 in December 2024, a nitrogen-fixing microbial specifically for corn and cereals. These developments highlight how critical coated grain seeds are to satisfying the caloric needs of a growing global population.

- RiceTec introduced a hybrid coated rice seed in India for the 2025 Kharif season.

- Argentina approved a drought-resistant wheat coating in early 2025.

- US USDA recorded 1.89 million farms using treated grain seeds in 2024.

To Understand More About this Research: Request A Free Sample

Regional Analysis

North America Captures 30.50% Market Share and Dominates Through High Value Genetics and Mechanization

The overwhelming concentration of seed coating material market valuation in North America is a direct reflection of the region's advanced agronomic model. In the United States and Canada, the seed is treated as a high-value technology platform rather than a simple input. With the widespread adoption of genetically modified organisms (GMOs) in corn, soybeans, and cotton, the cost of a single bag of seed can exceed $300. This high price point compels farmers to invest in premium "stacked" coatings that combine fungicides, insecticides, and biologicals to protect their investment. Furthermore, the region’s dominance is cemented by the universal use of high-speed precision planting equipment.

These machines require seeds with specific flowability coefficients to function correctly, making advanced polymer coatings a non-negotiable operational requirement. Consequently, North America captures the highest revenue per treated acre, as farmers pay for sophisticated, multi-layered chemical delivery systems that offer yield insurance.

Asia Pacific Expands via Rapid Hybridization and Food Security Policies

Asia Pacific is rapidly establishing itself as the volume engine of the global seed coating material market, driven by a fundamental shift in farming practices. The primary catalyst here is the transition from farm-saved seeds to commercially treated hybrids, particularly in China and India. In China, government mandates focused on national food security are forcing the modernization of the grain sector, leading to a surge in demand for industrial seed treatments in rice and wheat. India follows a similar trajectory, where the "hybridization" of cotton and maize is creating a massive new market for polymer coatings.

Unlike North America, where value is driven by complex chemical stacks, the demand in Asia is currently volume-centric, focused on basic dust control and establishing stand uniformity. However, as the region adopts drone seeding technologies, the demand for specialized, heavier coatings that drift less during aerial application is creating a new, lucrative niche.

Recent Developments in Seed Coating Material Market

- BioConsortia Revolutionizes Biological Shelf Life: BioConsortia has solved the industry’s biggest logistical hurdle with its FixiN 33 and Always-N formulations. By validating a two-year on-seed shelf life for nitrogen-fixing microbes, this technology allows living biological coatings to survive standard distribution chains without cold storage, finally matching the logistical durability of synthetic chemicals for the corn and cereal markets.

- Syensqo Launches Bio-Based Canola Binder: Addressing the EU's 2028 microplastic ban, Syensqo released Peridiam Quality 2001. This fully bio-based binder is engineered specifically for the difficult-to-coat oilseed rape market. It offers a critical drop-in replacement for synthetic polymers, maintaining high abrasion resistance and ensuring regulatory compliance without compromising the retention of insecticides during pneumatic planting.

- Lallemand Merges Flowability with Agronomy: Lallemand Plant Care introduced LALRISE SHINE DS, a dual-action coating combining a dry finisher with Bacillus velezensis. Using proprietary Pizazz technology, this formulation improves seed flowability while delivering microbes that boost phosphorus availability by 28%. This innovation effectively merges cosmetic enhancement with active agronomic performance in a single dry application.

Top Players in Global Seed Coating Material Market

- Bayer Crop Science AG

- BASF SE

- Clariant International

- Croda International

- Incotec Group

- Chromatech Incorporated

- Germains Seed Technology

- Brett Young

- Keystone Aniline Corporation

- Precision Laboratories

- Mahendra Overseas

- German Seeds Technology

- Other Prominent Players

Market Segmentation Overview:

By Origin

- Natural

- Synthetic

By Ingredient

- Adjuvants

- Binders

- Colorants

- Fertilizers

- Polymers

- Seed Planting Lubricants

By Type

- Film Coating

- Pelleting

- Seed Dressing

- Others

By Crop

- Grain

- Cereal

- Oilseed

- Fruit

- Vegetable

- Others

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- Western Europe

- The UK

- Germany

- France

- Italy

- Spain

- Rest of Western Europe

- Eastern Europe

- Poland

- Russia

- Rest of Eastern Europe

- Western Europe

- Asia Pacific

- China

- India

- Japan

- Australia & New Zealand

- South Korea

- ASEAN

- Rest of Asia Pacific

- Middle East & Africa (MEA)

- Saudi Arabia

- South Africa

- UAE

- Rest of MEA

- South America

- Argentina

- Brazil

- Rest of South America

REPORT SCOPE

| Report Attribute | Details |

|---|---|

| Market Size Value in 2024 | US$ 2,491.0 Mn |

| Expected Revenue in 2033 | US$ 4,655.5 Mn |

| Historic Data | 2020-2023 |

| Base Year | 2024 |

| Forecast Period | 2025-2033 |

| Unit | Value (USD Mn) |

| CAGR | 7.59% |

| Segments covered | By Origin, By Ingredient, By Type, By Crop, By Region |

| Key Companies | Bayer Crop Science AG, BASF SE, Clariant International, Croda International, Incotec Group, Chromatech Incorporated, Germains Seed Technology, Brett Young, Keystone Aniline Corporation, Precision Laboratories, Mahendra Overseas, German Seeds Technology, Other Prominent Players |

| Customization Scope | Get your customized report as per your preference. Ask for customization |

LOOKING FOR COMPREHENSIVE MARKET KNOWLEDGE? ENGAGE OUR EXPERT SPECIALISTS.

SPEAK TO AN ANALYST

.svg)

Features | Type of License | ||||

Data Book | Single User |   Multi User | Corporate | ||

| e-Access | ✓ | ✓ | ✓ | ✓ | |

User Sharing | 1 User Only | 1 User Only | Up to 7 Users | Unlimited User Access | |

⨉ | ⨉ | ⨉ | ✓ | ||

Free Customization | No Free Customization | Up To 30 hrs work | Up To 60 hrs work | Up To 80 hrs work | |

Deliverable |

| ⨉ | ✓ | ✓ | ✓ |

| ✓ | ⨉ | ✓ | ✓ | |

| ⨉ | ⨉ | ⨉ | ✓ | |

Analyst Support | 2-Months Analyst Support | 4-Months Analyst Support | 7-Months Analyst Support | One Year Analyst Support | |

Free Report update in next update cycle | ⨉ | ⨉ | ⨉ | ✓ | |

Free Industry Update (Within 180 days) | ⨉ | ⨉ | ⨉ | ✓ | |

Benefit | Up to 10% off on Post Purchase | Up to 20% off on Post Purchase | Up to 30% off on Post Purchase | Up to 40% off on Post Purchase | |