Marktszenario

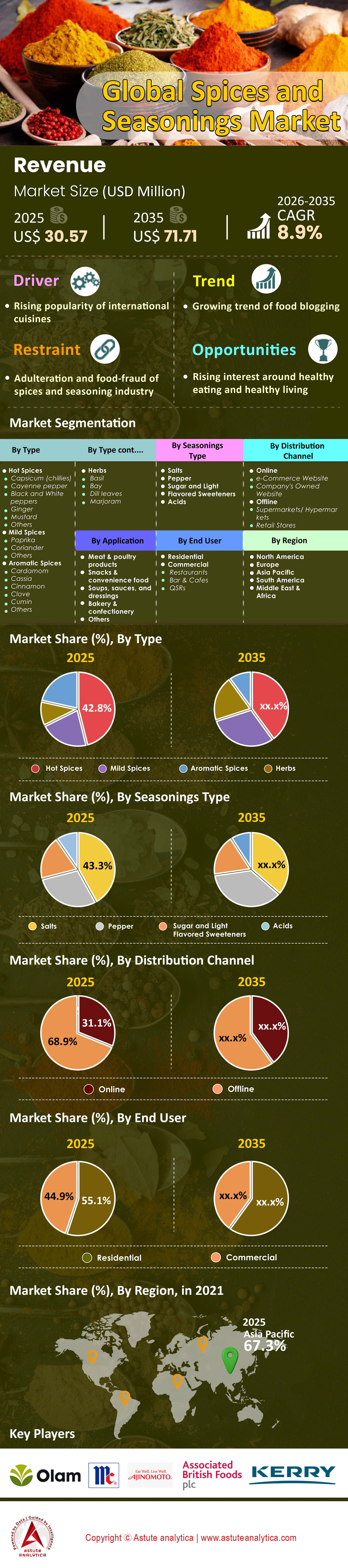

Der Markt für Gewürze und Würzmittel wurde im Jahr 2025 auf 30,57 Milliarden US-Dollar geschätzt und soll bis 2035 einen Umsatz von 71,71 Milliarden US-Dollar generieren, was einer durchschnittlichen jährlichen Wachstumsrate (CAGR) von 8,9 % im Prognosezeitraum 2026–2035 entspricht.

Wichtigste Erkenntnisse

- Nach Produktart betrachtet, halten scharfe Gewürze einen beachtlichen Marktanteil von 42,8 % am Gewürz- und Würzmittelmarkt.

- Im Bereich der Gewürze hat sich Salz als Marktführer herauskristallisiert. Es erzielt einen Umsatzanteil von über 43,30 % am Gesamtmarkt.

- Gemessen an der Verwendung sind Fleisch und Geflügel die Hauptabnehmer von Gewürzen und Würzmitteln weltweit.

- Gemessen am Vertriebskanal spielt der stationäre Einzelhandel eine bedeutende Rolle auf dem Markt für Gewürze und Würzmittel und erreicht einen Marktanteil von 68,9%.

- Der asiatisch-pazifische Raum ist mit einem Marktanteil von über 67,30 % der dominierende Marktführer.

Der globale Markt für Gewürze und Würzmittel verzeichnete 2024 ein starkes Wachstum, angetrieben durch steigenden Konsum, vielfältige Produktinnovationen und die starke Handelsleistung wichtiger Exportländer – allen voran Vietnam und Indien. Vietnam führte die Pfefferexporte mit 250.600 Tonnen im Wert von 1,31 Milliarden US-Dollar an, während Indien Rekordexporte von Gewürzen im Wert von 4,72 Milliarden US-Dollar erzielte. Diese Exportdynamik spiegelt die weltweit wachsende Nachfrage nach authentischen Aromen und ethnischen Küchen wider.

Im Produktionsbereich blieb die Kapazitätsauslastung hoch, wobei Indien und Vietnam trotz sinkender Lagerbestände und Preisschwankungen ein kritisches Produktionsniveau aufrechterhielten. Bei wichtigen Rohstoffen wie Pfeffer, Kreuzkümmel und Kurkuma stiegen die Preise aufgrund von Angebotsengpässen und steigenden Logistikkosten im Jahresvergleich um über 40 %.

Die Unternehmensleistung spiegelte die Dynamik des Gewürzmarktes wider. Branchenführer wie McCormick, Kerry Group und Olam verzeichneten ein starkes Umsatz- und EBITDA-Wachstum, das durch Produktdiversifizierung und operative Effizienzsteigerungen begünstigt wurde. Gleichzeitig beschleunigten die sich wandelnden Verbraucherpräferenzen für Bio-, Misch- und digital erhältliche Gewürzprodukte das Wachstum dieser Kategorie. Prognosen zufolge werden die anhaltende Expansion im E-Commerce, gesundheitsorientierte Konsummuster und die Modernisierung der Lieferketten den globalen Marktwert bis 2028 voraussichtlich auf über 25 Milliarden US-Dollar steigern und damit den langfristigen Wachstumskurs bestätigen.

Für weitere Einblicke fordern Sie ein kostenloses Muster an.

Welche 5 Gewürze beherrschen den globalen Gaumen?

Obwohl die Aromenvielfalt weltweit riesig ist, haben sich fünf Gewürze bis 2025 als die Schwergewichte des globalen Gewürzkonsums etabliert. Schwarzer Pfeffer, oft als „König der Gewürze“ bezeichnet, dominiert weiterhin und macht rund 38 % des weltweiten Gewürzhandelsvolumens aus. Seine weite Verbreitung in der industriellen Lebensmittelverarbeitung und in Privathaushalten macht ihn unverzichtbar. Dicht dahinter folgen Chilischoten (Capsicum), deren Beliebtheit aufgrund der stark gestiegenen Nachfrage nach Schärfe in westlichen Snacks und der asiatischen Küche explodiert; allein der weltweite Handel mit getrockneten Chilischoten überstieg in diesem Jahr im Gewürzmarkt 1,5 Milliarden US-Dollar.

Kreuzkümmel belegt den dritten Platz, vor allem aufgrund seiner zentralen Rolle in der Küche des Nahen Ostens, Indiens und zunehmend auch Lateinamerikas. Kurkuma rangiert an vierter Stelle, verzeichnet aber wertmäßig das schnellste Wachstum und profitiert von der zunehmenden Verbreitung im Bereich „Functional Wellness“. Die globalen Transaktionspreise für Kurkuma lagen zuletzt bei rund 1,92 US-Dollar pro Kilogramm, was auf seine entzündungshemmende Wirkung zurückzuführen ist. Ingwer schließlich verzeichnete einen Anstieg der Bio-Exportmengen um 18 Prozent, angetrieben von der Getränke- und Pharmaindustrie. Zusammen bestimmen diese fünf Gewürze den Rhythmus der globalen Handelsströme auf dem Gewürzmarkt.

Wer kontrolliert die 14 Millionen Tonnen schwere Produktionsanlage?

Der Markt für Gewürze und Würzmittel ist schier gigantisch. Ende 2025 wird die weltweite Gewürzproduktion auf 13,8 Millionen Tonnen geschätzt und nähert sich damit der Prognose von 14,3 Millionen Tonnen bis 2028. Diese Produktionsmenge ist jedoch ungleich verteilt; sie konzentriert sich stark auf wenige Schlüsselregionen. Indien bleibt der unangefochtene Gigant und trägt mit geschätzten 6,2 Millionen Tonnen für das Geschäftsjahr 2025 fast 44 % zur weltweiten Gesamtproduktion bei.

Hinter Indien belegt China den zweiten Platz und dominiert insbesondere den Knoblauch- und Ingwersektor mit einer Produktion von über einer Million Tonnen. Vietnam bleibt das strategische Drehkreuz für Pfeffer und exportierte 2024 250.600 Tonnen. Länder wie Indonesien und Brasilien sind wichtige Akteure für Nelken bzw. Pfeffer. Klimaschwankungen haben jedoch die Erträge beeinträchtigt; so war beispielsweise Madagaskar, der Hauptlieferant von Vanille, von schweren Wetterereignissen betroffen, die die Lieferketten unterbrachen und die Anfälligkeit des Marktes verstärkten.

Welche Branchenriesen dominieren das Wettbewerbsumfeld?

Der Markt für Gewürze und Würzmittel ist hart umkämpft; vier Giganten prägen die globalen Geschmackstrends. McCormick & Company behauptet seine Marktführerschaft mit einem Nettoumsatz von 6,6 Milliarden US-Dollar im Jahr 2024. Ihre Dominanz basiert auf einer Doppelstrategie: starke Marken im Einzelhandel und innovative Aromenlösungen für die Industrie.

An zweiter Stelle folgt die Kerry Group, ein führendes Unternehmen im Bereich Geschmack und Ernährung, das einen Umsatz von 8,0 Milliarden Euro (ca. 8,7 Milliarden US-Dollar) erzielte und dank intensiver Forschung und Entwicklung den Gastronomiesektor eroberte. Der dritte wichtige Akteur ist Ajinomoto Co., Inc., das den asiatischen Markt und das globale Segment der Umami- und Geschmacksverstärker dominiert. Schließlich bildet die Olam Group (insbesondere ihre „ofi“-Division) das Rückgrat der Lieferkette. Mit einem operativen Gewinn (EBIT) von 1,07 Milliarden Singapur-Dollar verschafft Olams Kontrolle über die Rohstoffquellen – vom Acker bis zur Fabrik – dem Unternehmen eine unübertroffene Verhandlungsmacht in Bezug auf Preisgestaltung und Logistik.

Wie verändern Handelskriege und Zölle die Lieferketten im Jahr 2025?

Das Jahr 2025 war von beispiellosen Turbulenzen im Gewürzhandel geprägt. Die Einführung neuer Zollregelungen durch die US-Regierung im August 2025 löste in der Branche einen Schock aus. Ein Basiszoll von 10 % auf allgemeine Importe, kombiniert mit gezielten Zöllen von bis zu 50 % auf Länder ohne bilaterale Abkommen, veränderte die Kostenstrukturen grundlegend. So wurden vietnamesische Gewürze mit einem Zoll von 46 % belegt, während Vergeltungsmaßnahmen die Zölle auf chinesischen Knoblauch und Paprika auf 145 % ansteigen ließen.

Diese politischen Maßnahmen haben eine rasche Diversifizierung der Lieferketten erzwungen. US-Importeure, die im vergangenen Jahr über 466 Millionen US-Dollar mit bestimmten Gewürzkategorien erwirtschafteten, bemühen sich nun verstärkt um eine Verlagerung ihrer Beschaffung nach Indien und Brasilien, um Kosten zu senken. Infolgedessen hat sich die Frachtdynamik verschärft; der Versand eines Containers von Vietnam an die US-Westküste kostet mittlerweile rund 3.700 US-Dollar, was die Margen der Händler schmälert. Diese geopolitischen Spannungen sind wohl der bedeutendste Faktor für die aktuelle Entwicklung des Gewürzmarktes.

Wer treibt die Nachfrage an? Identifizierung der Power-User

Die Nachfrage nach Gewürzen auf dem globalen Gewürzmarkt ist dreigeteilt: Lebensmittelverarbeitung, Gastronomie und Einzelhandel. Der Gastronomiesektor (HoReCa) ist derzeit der größte Umsatzträger und trägt rund 59,9 % zum Marktumsatz bei. Dies wird durch die nach der Pandemie wieder angestiegene Beliebtheit von Restaurantbesuchen und die rasante Expansion von Schnellrestaurants (QSRs) befeuert, die mit internationalen Geschmacksrichtungen wie Peri-Peri und Chipotle experimentieren.

Parallel dazu verwendet die Lebensmittelindustrie große Mengen an Oleoresinen und gemahlenen Gewürzen für Fertiggerichte, Snacks und Soßen. Den größten qualitativen Wandel erlebt jedoch der Einzelhandel. Da Kochen zu Hause auch nach 2024 weiterhin beliebt bleiben wird, kaufen Verbraucher vermehrt hochwertige Gewürze aus einer einzigen Herkunftsregion. Der Online-Gewürzabsatz in wichtigen Märkten stieg dieses Jahr um 25 %, was die Bereitschaft zeigt, für Qualität und Authentizität mehr zu bezahlen als für generische Mischungen.

Welche Zukunftstrends und Innovationen treiben das Wachstum an?

Die Zukunft des Gewürzmarktes wird von Technologie und Wellness geprägt. KI-gestützte Geschmacksprofilierung ist eine bahnbrechende Entwicklung: Unternehmen investieren Millionen, um die nächste virale Geschmackskombination vorherzusagen, bevor sie in den Handel kommt. Der Trend „Gesundheit als Geschmack“ ist unaufhaltsam. Gewürze sind längst nicht mehr nur Geschmacksgeber, sondern auch funktionelle Nahrungsergänzungsmittel. Produkte wie Kurkuma-Lattes und Ingwer-Shots zur Stärkung des Immunsystems haben zu einem Anstieg der Kurkuma-Importe in den Westen um 20 % geführt.

Nachhaltigkeit ist ein weiteres wichtiges Thema. Da die Europäische Union strengere Rückstandsgrenzwerte durchsetzt, verlagert sich der Markt hin zu Bio-Gewürzen und Gewürzen aus integriertem Pflanzenschutz (IPM). Die weltweiten Importe von Bio-Gewürzen stiegen 2024 um 15 %, und Initiativen wie Indiens SPICED-Programm – das durch modernisierte Infrastruktur die Exportkapazität steigern soll – setzen neue Maßstäbe für die Einhaltung von Qualitätsstandards.

Welche Hindernisse gefährden die Dynamik des Gewürzhandels?

Trotz des Optimismus steht der Gewürzmarkt vor erheblichen Herausforderungen. Der Klimawandel stellt die größte existenzielle Bedrohung dar; ungewöhnliche Regenfälle in Indien und Dürren in Brasilien haben zu Ertragsschwankungen von 30–35 % bei Nutzpflanzen wie Kreuzkümmel und Paprika geführt, was wiederum Preissprünge zur Folge hatte. Hinzu kommt, dass die Verfälschungskrise weiterhin ein Reputationsrisiko darstellt und Käufer dazu veranlasst, Blockchain-basierte Rückverfolgbarkeit zu fordern.

Schließlich hat der Handelskrieg von 2025 eine zusätzliche finanzielle Unsicherheit mit sich gebracht. Kleine Exporteure in Vietnam und China stehen aufgrund der prohibitiven Zölle vor existenziellen Krisen, was möglicherweise zu einer Konsolidierung führt, bei der nur große Unternehmen mit diversifizierten Beschaffungsnetzwerken überleben werden. Die Akteure müssen in diesem turbulenten Umfeld agil agieren, da die Ära billiger und stabiler Gewürzlieferungen offenbar zu Ende geht.

Segmentanalyse

Nach Gewürzart: Steigende weltweite Nachfrage nach Schärfe führt zu Rekordexporten und Produktionsmengen

Die weltweite Nachfrage nach scharfen Aromen prägt weiterhin die Handelsdynamik auf dem Gewürzmarkt, wobei scharfe Gewürze mit einem Marktanteil von 42,8 % dominieren. Schärfe ist zu einem universellen Merkmal moderner kulinarischer Erlebnisse geworden und hat Rekordexporte führender Produzenten wie Indien und Vietnam beflügelt. Indien exportierte im Geschäftsjahr 2024/25 über 715.000 Tonnen getrocknete Chilischoten und reagierte damit eindrucksvoll auf den weltweit steigenden Konsum. Gleichzeitig importierten die Vereinigten Staaten im Jahr 2024 fast 72.000 Tonnen Pfeffer aus Vietnam, um die wachsende Nachfrage ihrer Konsumenten nach kräftigen, feurigen Aromen zu befriedigen. Vietnam, das diese außergewöhnliche Nachfrage antizipiert, plant, im Jahr 2025 rund 170.000 Tonnen schwarzen Pfeffer zu produzieren, was auf eine anhaltende Produktionssteigerung hindeutet. Allein in den ersten Monaten des Jahres 2025 wurden 27.416 Tonnen schwarzer Pfeffer aus Vietnam exportiert, was beweist, dass die Marktnachfrage nach Schärfe noch lange nicht gesättigt ist. Der durch die Hitze ausgelöste Handelsstrom sichert nicht nur exportorientierte Einnahmen, sondern verstärkt auch die kulturelle Allgegenwärtigkeit von Schärfe in der globalen Küche.

Neben der reinen Schärfe prägt das wachsende Interesse an natürlichen Aroma- und Farbstoffen die zukünftige industrielle Beschaffung auf dem globalen Gewürzmarkt. Paprika, mit einem jährlichen Handelsvolumen von fast 150.000 Tonnen im Jahr 2024, hat sich als vielseitiges Gewürz etabliert, das sowohl den Geschmack als auch die Optik verbessert. China ist mit Exporterlösen von über 671 Millionen US-Dollar führend in diesem Segment, während Europa, insbesondere Spanien, mit 25.000 exportierten Tonnen weiterhin ein wichtiger Lieferant ist. Der Paprikamarkt hat mittlerweile einen Wert von 588,2 Millionen US-Dollar und unterstreicht damit seine Bedeutung für die Lebensmittelherstellung und die Entwicklung gesundheitsorientierter Produkte. Indiens Erfolg spiegelt diese Entwicklung wider: Die Exporte von rotem Chili erreichten 2024 einen Rekordwert von 1,5 Milliarden US-Dollar, während die Kreuzkümmellieferungen 160.000 Tonnen überstiegen und so die anhaltende Exportstärke des Landes verdeutlichen. Insgesamt bleiben scharfe Gewürze das wirtschaftliche und sensorische Rückgrat des wachsenden globalen Gewürzhandels.

Durch die Verwendung von Gewürzen sichert sich Essential Industrial and Culinary Reliance die Marktführerposition für Salz

Als Grundpfeiler der Geschmacksentwicklung und Lebensmittelkonservierung dominiert Salz weiterhin den globalen Gewürzmarkt mit einem Umsatzanteil von über 43,3 %. Seine Bedeutung geht über den Geschmack hinaus und umfasst biologische Notwendigkeiten sowie die Skalierbarkeit der Produktion in verschiedenen Branchen. China ist mit einer Produktion von über 53 Millionen Tonnen im Jahr 2024 weltweit führend und festigt damit seine Position als wichtiger globaler Lieferant. Die Vereinigten Staaten, mit einer Eigenproduktion von 42 Millionen Tonnen, bleiben ein bedeutender Verbraucher und importieren rund 11 Millionen Tonnen, um ihre strukturelle Versorgungslücke zu schließen. Der Gesamtverbrauch in den USA, sowohl im industriellen als auch im Lebensmittelbereich, erreichte 47 Millionen Tonnen und unterstreicht damit die unverzichtbare Rolle von Salz in der Lebensmittelindustrie. In der Gewürzindustrie dient Salz sowohl als Geschmacksverstärker als auch als Basis für Gewürzmischungen und sichert sich so seine Position als wichtigste Zutat in der Wertschöpfungskette der Gewürzherstellung.

Gleichzeitig hat das gestiegene Gesundheitsbewusstsein und der Trend zu gehobener Gastronomie zu einer bemerkenswerten Diversifizierung im Salzsegment geführt. Himalaya-Salz, bekannt für seinen Mineralstoffgehalt und sein hochwertiges Aussehen, gewinnt weltweit an Bedeutung. Pakistan exportierte in den letzten zwölf Monaten über 4.997 Lieferungen, wobei die Exporte allein nach China bis Oktober 2025 einen Wert von 6,04 Millionen US-Dollar erreichten. Der industrielle Verbrauch in China belief sich Anfang 2025 auf insgesamt 23,94 Millionen Kilogramm importiertes pakistanisches Himalaya-Salz, was die Nachfrage sowohl nach funktionalen als auch nach ästhetischen Eigenschaften unterstreicht. In westlichen Märkten importierten die USA in den ersten drei Quartalen 2024 Salz im Wert von 442 Millionen US-Dollar, darunter Steinsalz im Wert von 300 Millionen US-Dollar für industrielle Anwendungen und Enteisung. Auch Indien weist mit jährlich über 26 Millionen Tonnen eine starke Produktionsgrundlage auf. Zusammengenommen verdeutlichen diese Zahlen, wie die Allgegenwärtigkeit und Anpassungsfähigkeit von Salz die Stabilität und Skalierbarkeit des Gewürzmarktes untermauern.

Anwendungsbedingt erfordert der steigende Proteinkonsum massive Mengen an Aromastoffen und Konservierungsmitteln

Fleisch- und Geflügelverarbeitung bleibt der größte Abnehmer von Gewürzen und Würzmitteln, angetrieben durch den steigenden Proteinkonsum in Schwellen- und Industrieländern. Die weltweite Geflügelfleischproduktion wird Prognosen zufolge im Jahr 2025 151,4 Millionen Tonnen erreichen, was die Nachfrage nach Marinaden, Gewürzmischungen und Pökelgewürzen deutlich erhöht. Allein die USA erwarten eine Produktion von 47,69 Milliarden Pfund Broilerfleisch, was einen enormen Bedarf an Pfeffer, Knoblauch und Gewürzmischungen mit sich bringt. Parallel dazu konsumierte China im Jahr 2024 29,26 Millionen Tonnen Geflügel und bildete damit einen riesigen integrierten Markt für Aromastoffe. Da der weltweite Pro-Kopf-Verbrauch von Geflügel im Jahr 2025 auf 6,1 Kilogramm geschätzt wird, dürfte der industrielle Einsatz von Würzmitteln proportional steigen. Diese Abhängigkeit von Gewürzen unterstreicht ihre doppelte Funktion: Sie erhalten die Frische und verbessern den Geschmack. Dieser wachsende Bedarf positioniert den Gewürzmarkt als wichtigen Bestandteil der globalen Proteinverarbeitung.

Auf der Produktionsseite setzen Fleischverarbeiter und Zutatenhersteller verstärkt auf funktionelle Extrakte, um Produktqualität und Effizienz zu steigern. So verwendete die Branche 2024 über 18.000 Tonnen Paprika-Oleoresin als Farb- und Aromastoff für verarbeitetes Fleisch. Geflügelfutterhersteller setzten 2023/24 schätzungsweise 6.000 Tonnen Paprika-basierte Zusatzstoffe ein, um die Pigmentierung und die Marktakzeptanz zu verbessern. Der Inlandsverbrauch von Geflügel in den USA blieb mit 20,18 Millionen Tonnen im Jahr 2024 weiterhin hoch, während Vietnams kleinerer, aber schnell wachsender Sektor 1,8 Millionen Tonnen erreichte. Der Exportwert von Spezialgewürzmischungen für Fleisch überstieg 200 Millionen US-Dollar und ging in die asiatischen Verarbeitungszentren, was das expandierende Produktionsökosystem der Region unterstreicht. Da die weltweiten Fleischexporte im Jahr 2024 voraussichtlich auf 40,2 Millionen Tonnen ansteigen werden, sind Gewürzhersteller in allen Bereichen der Wertschöpfungskette für Proteine vertreten und müssen Geschmackskonsistenz, Sicherheit und regionale Geschmacksanpassung gewährleisten.

Diesen Bericht anpassen + von einem Experten validieren

Greifen Sie nur auf die Abschnitte zu, die Sie benötigen – regionsspezifisch, unternehmensbezogen oder nach Anwendungsfall.

Beinhaltet eine kostenlose Beratung mit einem Domain-Experten, der Sie bei Ihrer Entscheidung unterstützt.

Nach wie vor sind weitverzweigte physische Ladennetze der bevorzugte Vertriebskanal für sensorische Einkaufserlebnisse

Trotz der rasanten Digitalisierung hält der stationäre Handel weiterhin einen dominanten Marktanteil von 68,9 % am globalen Gewürzmarkt. Dies spiegelt die Vorliebe der Verbraucher für haptische, sinnliche Erlebnisse wider. Der Kauf von Gewürzen ist naturgemäß visuell und olfaktorisch geprägt, da Käufer vor dem Kauf häufig Farbe, Körnung und Aroma beurteilen. Einzelhandelskonzerne wie Walmart, die 2025 weltweit über 10.500 Filialen betreiben, bieten eine unübertroffene Auswahl an hochwertigen und preisgünstigen Gewürzen. Auch Costco, mit 890 Lagerhäusern weltweit bis Ende 2024, bedient Großabnehmer und kleine Restaurants. Der Lebensmittelhändler Kroger mit fast 2.800 Filialen verstärkt die Nachfrage der Privathaushalte, während McCormicks umfangreiches Netzwerk in 150 Ländern die anhaltende Bedeutung von Partnerschaften im stationären Handel unterstreicht. Diese weitverzweigten Filialnetze prägen das Kaufverhalten, indem sie den Verbrauchern die Möglichkeit bieten, Produkte physisch zu prüfen und Marken kennenzulernen.

Expansionsinitiativen im Einzelhandel bestätigen die Stärke und Reichweite des stationären Handels. Aldi kündigte an, bis 2028 800 neue Filialen in den USA zu eröffnen und so die Erschwinglichkeit und Verfügbarkeit von Gewürzen zu verbessern. Sprouts Farmers Market eröffnete 2024 35 neue Standorte, um gesundheitsbewusste Kunden mit Bio-Mischungen zu bedienen, während Ollie's Bargain Outlet 47 Filialen hinzufügte, um preisbewusste Käufer anzusprechen. Ethnische Supermärkte wie Patel Brothers (über 50 Filialen) und H Mart (über 90 Filialen in den USA) verbinden weiterhin kulturelle Vorlieben mit geografischer Erreichbarkeit. Trader Joe's vertreibt exklusive Eigenmarken-Gewürze in über 540 Filialen und erweitert so die Markenvielfalt und das Einkaufserlebnis im Geschäft. Die Beständigkeit dieses stationären Vertriebsmodells unterstreicht die anhaltende Vorliebe der Verbraucher für haptische Einkaufserlebnisse. Folglich bleibt der Gewürzmarkt trotz wachsender Online-Konkurrenz weiterhin fest in stationären Einzelhandelsnetzen verankert, die Markentreue, Absatzvolumen und Marktpräsenz fördern.

Um mehr über diese Studie zu erfahren: Fordern Sie ein kostenloses Muster an

Regionalanalyse

Asien-Pazifik kontrolliert das globale Angebot durch massive Produktions- und Konsummengen

Der asiatisch-pazifische Raum dominiert den Gewürzmarkt mit einem gewaltigen Marktanteil von 67,30 %. Diese Vormachtstellung beruht auf seiner Doppelrolle als weltweit größter Produzent und Konsument. Maßgeblich für diese Hegemonie ist Indien, der unangefochtene Produktionsmotor, der in diesem Geschäftsjahr rekordverdächtige 1,8 Millionen Tonnen Gewürze exportierte und gleichzeitig 4,7 Millionen Tonnen im Inland verbrauchte. Diese Binnennachfrage sichert der Region ihre Selbstversorgung auch in Zeiten globaler Handelsstörungen.

Vietnam ergänzt dies durch seine zentrale Rolle im globalen Pfefferhandel und generiert allein im Jahr 2024 Exporterlöse in Höhe von 1,318 Milliarden US-Dollar. Darüber hinaus festigt China die Position der Region in der Lieferkette, indem es 918.000 Tonnen Knoblauch und Ingwer exportiert hat, um die globalen Lagerbestände zu stabilisieren. Letztendlich gibt der asiatisch-pazifische Raum die Marktentwicklung vor, da er die Rohstoffquellen direkt vom Erzeuger kontrolliert.

Nordamerika generiert Wertschöpfung durch verarbeitete Lebensmittel und hohe Importabhängigkeit im Gewürz- und Würzmittelmarkt

Mit Blick auf den Westen erweist sich Nordamerika als zweitgrößter Markt, angetrieben nicht von landwirtschaftlichen Nutzflächen, sondern von der hochwertigen industriellen Weiterverarbeitung und dem Trend zu Convenience-Produkten. Allein der US-Markt für Gewürzmischungen wuchs bis 2025 auf 5,49 Milliarden US-Dollar, befeuert durch einen massiven Anstieg der Verbrauchernachfrage nach scharfen Barbecue-Gewürzen und Chilisaucen um 373 %. Da die lokale Produktion begrenzt ist, ist die Region stark auf Importe angewiesen und importierte dieses Jahr 150.000 Tonnen schwarzen Pfeffer für ihre industriellen Mühlen. Der Importwert bestimmter Gewürzkategorien überstieg 466 Millionen US-Dollar, was die Bereitschaft widerspiegelt, höhere Logistikkosten zu tragen, um den Bedarf des Convenience-Food-Sektors zu decken. Diese Region verarbeitet importierte Rohstoffe zu margenstarken Konsumgütern und schafft so einen immensen wirtschaftlichen Mehrwert.

Europa setzt bei Gewürzen und Würzmitteln auf höchste Qualität und Bio-Zertifizierung

Europa behauptet den dritten Platz auf dem globalen Gewürzmarkt, indem es Premiumisierung, Nachhaltigkeit und die strikte Einhaltung gesetzlicher Vorschriften über reine Mengen stellt. Die Region importierte rund 780.000 Tonnen Gewürze und Kräuter, wobei Deutschland als zentrales Verarbeitungszentrum fungierte und allein 14.580 Tonnen vietnamesischen Pfeffer abnahm. Charakteristisch ist die Nachfrage nach Reinheit und Zutaten mit transparenten Inhaltsangaben („Clean Label“). Europäische Märkte trugen bis 2024 zu einem Anstieg des weltweiten Absatzvolumens von Bio-Gewürzen um 15 % bei. Daher akzeptieren Käufer in dieser Region höhere Preise; so liegt der Durchschnittspreis für weißen Pfeffer bei 6.884 US-Dollar pro Tonne, um die strengen EU-Sicherheitsstandards zu erfüllen. Europas Einfluss besteht darin, den globalen Maßstab für Qualitätssicherung und Rückverfolgbarkeit zu setzen.

Aktuelle Entwicklungen auf dem Gewürz- und Würzmittelmarkt

Die 5 wichtigsten Unternehmensentwicklungen der letzten Zeit im Bereich Gewürze und Würzmittel (2025)

- McCormick® Geschmack des Jahres 2025: Bekanntgegeben am 28. Januar 2025. Die Wahl fiel auf Aji Amarillo – eine fruchtige peruanische Paprika – für die limitierte Gewürzmischung, ideal für Meeresfrüchte, Geflügel und Saucen.

- McCormick Gourmet Redesign: Einführung am 5. November 2025 mit hochwertigen Verpackungs-Upgrades für Kräuter und Gewürze zur Stärkung der Positionierung im Gewürzmarkt und zur Förderung des Wachstums bis 2026.

- Die globalen Geschmackscharts der Kerry Group für 2025: Veröffentlicht am 15. Januar 2025, mit Prognosen zu Trends wie Sichuan-Gewürzen in Europa, indischen Masalas in Snacks und Yuzu in Getränken.

- Droosh™ Neue scharfe Saucen & Verpackung: Vorgestellt am 6. Januar 2025, mit Jalapeno-Grün-Chutney, süß-saurem Mango-Chutney und neu gestalteten Gewürzmischungen für authentische indische Aromen.

- Pansuola Gewürzmischungen mit reduziertem Natriumgehalt: Eingeführt am 15. Oktober 2025 von Oriola mit AromaPansuola und GrilliPansuola – mineralstoffreiche Varianten mit 50 % weniger Natrium als herkömmliches Salz.

Führende Unternehmen auf dem Gewürz- und Würzmittelmarkt:

- McCormick & Company, Inc. (USA)

- Olam International (Singapur)

- Ajinomoto Co. Inc. (Japan)

- Associated British Foods plc (UK)

- Kerry Group plc (Irland)

- Sensient Technologies Corporation (USA)

- Döhler-Gruppe (Deutschland)

- SHS-Gruppe (Irland)

- Worlée Gruppe (Deutschland)

- Watkins Incorporated (USA)

- Ariake Japan Co. Ltd (Japan)

- MDH (Indien)

- Weitere prominente Spieler

Marktsegmentierungsübersicht:

Nach Typ

- Scharfe Gewürze

- Capsicum (Chilis)

- Cayennepfeffer

- Schwarzer und weißer Pfeffer

- Ingwer

- Senf

- Andere

- Milde Gewürze

- Paprika

- Koriander

- Andere

- Aromatische Gewürze

- Kardamom

- Cassia

- Zimt

- Nelke

- Kreuzkümmel

- Andere

- Kräuter

- Basilikum

- Bucht

- Dillblätter

- Majoran

- Estragon

- Andere

Nach Gewürzart

- Salze

- Pfeffer

- Zucker und leichte Aromasüßstoffe

- Säuren

Vom Endbenutzer

- Wohnen

- Kommerziell

- Restaurants

- Bars & Cafés

- Schnellrestaurants

Nach Vertriebskanal

- Online

- E-Commerce-Website

- Firmeneigene Website

- Offline

- Supermärkte/Hypermärkte

- Einzelhandelsgeschäfte

Durch Bewerbung

- Fleisch- und Geflügelprodukte

- Snacks und Fertiggerichte

- Suppen, Soßen und Dressings

- Bäckerei & Konditorei

- Andere

Nach Region

- Nordamerika

- Die USA.

- Kanada

- Mexiko

- Europa

- Westeuropa

- Vereinigtes Königreich

- Deutschland

- Frankreich

- Italien

- Spanien

- Übriges Westeuropa

- Osteuropa

- Polen

- Russland

- Übriges Osteuropa

- Westeuropa

- Asien-Pazifik

- China

- Indien

- Japan

- Südkorea

- Australien und Neuseeland

- ASEAN

- Übriges Asien-Pazifik

- Naher Osten und Afrika (MEA)

- VAE

- Saudi-Arabien

- Südafrika

- Rest von MEA

- Südamerika

- Brasilien

- Argentinien

- Restliches Südamerika

BERICHTSUMFANG

| Berichtattribute | Details |

|---|---|

| Marktgröße und Wert im Jahr 2025 | 30,57 Mrd. US-Dollar |

| Erwartete Einnahmen im Jahr 2035 | 71,71 Mrd. US-Dollar |

| Historische Daten | 2020-2024 |

| Basisjahr | 2025 |

| Prognosezeitraum | 2026-2035 |

| Einheit | Wert (Mrd. USD) |

| CAGR | 8.9% |

| Abgedeckte Segmente | Nach Art, Gewürzart, Endverbraucher, Vertriebskanal, Anwendung, Region |

| Wichtige Unternehmen | McCormick & Company, Inc. (USA), Olam International (Singapur), Ajinomoto Co. Inc. (Japan), Associated British Foods plc (Großbritannien), Kerry Group plc (Irland), Sensient Technologies Corporation (USA), Döhler Group (Deutschland), SHS Group (Irland), Worlée Gruppe (Deutschland), Watkins Incorporated (USA), Ariake Japan Co. Ltd (Japan), MDH (Indien), Weitere bedeutende Akteure |

| Anpassungsumfang | Erhalten Sie Ihren individuell angepassten Bericht nach Ihren Wünschen. Fragen Sie nach individuellen Anpassungen. |

HÄUFIG GESTELLTE FRAGEN

Der globale Markt für Gewürze und Würzmittel wurde im Jahr 2025 auf 30,57 Milliarden US-Dollar geschätzt und soll bis 2035 einen Umsatz von 71,71 Milliarden US-Dollar generieren, was einer durchschnittlichen jährlichen Wachstumsrate (CAGR) von 8,9 % im Prognosezeitraum 2026–2035 entspricht.

Zu den Schwergewichten des globalen Gaumens zählen schwarzer Pfeffer, der etwa 38 % des Handelsvolumens ausmacht; Chilischoten mit einem Handelswert von über 1,5 Milliarden US-Dollar; Kreuzkümmel, unverzichtbar in der Küche des Nahen Ostens und Indiens; Kurkuma, das aufgrund von Wellness-Trends den größten Wertzuwachs verzeichnet; und Ingwer, bei dem die Bio-Exportmengen im Jahr 2025 um 18 % steigen werden.

Indien ist unangefochtener Marktführer und trägt mit einer Eigenproduktion von 6,2 Millionen Tonnen fast 44 % zur Weltproduktion bei. China folgt an zweiter Stelle und dominiert die Knoblauch- und Ingwerproduktion. Vietnam bleibt das strategische Drehkreuz für Pfefferexporte, während Indonesien (Nelken) und Brasilien (Pfeffer) wichtige Akteure im globalen Produktionszentrum mit einem Volumen von 14 Millionen Tonnen sind.

Die Einführung neuer US-Zölle im August 2025 hat die Lieferketten erheblich beeinträchtigt. Ein allgemeiner Basiszoll von 10 %, ergänzt durch spezifische Zölle von 46 % auf vietnamesische Gewürze und Vergeltungszölle von bis zu 145 % auf chinesischen Knoblauch und Paprika, hat Importeure gezwungen, ihre Beschaffung auf Indien und Brasilien auszuweiten. Zudem sind die Frachtkosten sprunghaft angestiegen; die Versandkosten von Vietnam in die USA erreichen rund 3.700 US-Dollar pro Container.

Der Markt konzentriert sich auf vier große Unternehmen: McCormick & Company, Marktführer mit einem Nettoumsatz von 6,6 Milliarden US-Dollar; die Kerry Group, ein Schwergewicht in den Bereichen Geschmack und Forschung & Entwicklung; Ajinomoto Co., Inc., das den Markt für Geschmacksverstärker beherrscht; und die Olam Group (ofi), die als Rückgrat der globalen Lieferkette vom Acker bis zur Fabrik dient.

Der asiatisch-pazifische Raum wird voraussichtlich 2025 einen beeindruckenden Marktanteil von 67,30 % halten. Diese Dominanz ist darauf zurückzuführen, dass die Region sowohl der weltweit größte Produzent (angeführt von Indien und Vietnam) als auch eine riesige Konsumentenbasis darstellt. Nordamerika folgt als zweitgrößter Markt, angetrieben von einer hochwertigen industriellen Verarbeitung und einer starken Importabhängigkeit zur Deckung der Nachfrage nach Fertiggerichten.

Der Markt für Gewürze und Würzmittel steht vor drei großen Herausforderungen: dem Klimawandel, der aufgrund ungewöhnlicher Wetterbedingungen zu Ertragsschwankungen von 30-35 % bei Nutzpflanzen wie Kreuzkümmel und Paprika geführt hat; der Verfälschung von Produkten, die Reputationsrisiken birgt und die Nachfrage nach Rückverfolgbarkeit erhöht; und geopolitischen Spannungen, insbesondere Handelszöllen, die die Kostenstrukturen verändern und die Konsolidierung kleinerer Exporteure erzwingen.

SIE SUCHEN UMFASSENDES MARKTWISSEN? KONTAKTIEREN SIE UNSERE EXPERTEN.

SPRECHEN SIE MIT EINEM ANALYSTEN

.svg)

Merkmale | Lizenzart | ||||

Datenbuch | Einzelbenutzer |   Mehrere Benutzer | Unternehmen | ||

| E-Zugang | ✓ | ✓ | ✓ | ✓ | |

Benutzerfreigabe | Nur für 1 Benutzer | Nur für 1 Benutzer | Bis zu 7 Benutzer | Unbegrenzter Benutzerzugriff | |

⨉ | ⨉ | ⨉ | ✓ | ||

Kostenlose Anpassung | Keine kostenlose Anpassung | Bis zu 30 Stunden Arbeit | Bis zu 60 Stunden Arbeit | Bis zu 80 Arbeitsstunden | |

Lieferformat |

| ⨉ | ✓ | ✓ | ✓ |

| ✓ | ⨉ | ✓ | ✓ | |

| ⨉ | ⨉ | ⨉ | ✓ | |

Analystenunterstützung | 2 Monate Analystenunterstützung | 4 Monate Analystenunterstützung | 7 Monate Analystenunterstützung | Ein Jahr Analystenbetreuung | |

Kostenloses Bericht-Update im nächsten Aktualisierungszyklus | ⨉ | ⨉ | ⨉ | ✓ | |

Kostenloses Branchen-Update (Innerhalb von 180 Tagen) | ⨉ | ⨉ | ⨉ | ✓ | |

Nutzen | Bis zu 10 % Rabatt nach dem Kauf | Bis zu 20 % Rabatt nach dem Kauf | Bis zu 30 % Rabatt nach dem Kauf | Bis zu 40 % Rabatt nach dem Kauf | |