U.S. Trifluralin Market: By Product Type (Solid, Liquid, Granular); Grade Type (Technical Grade, Formulated, Hybrid); Application (Crops, Fruits, Flowers, Broadleaf Weeds, Annual Grasses, Others); Method (Ground Broadcast Application, Aerial Broadcast Application, Dry Bulk Fertilizer); End Use (Residential (HOBBY/ GARDEN /TURF and ORNAMENTAL), Commercial); Distribution Channel (Direct and Distributor); Market Size, Industry Dynamics, Opportunity Analysis and Forecast for 2025–2033

- Last Updated: 20-May-2025 | | Report ID: AA05251319

Market Scenario

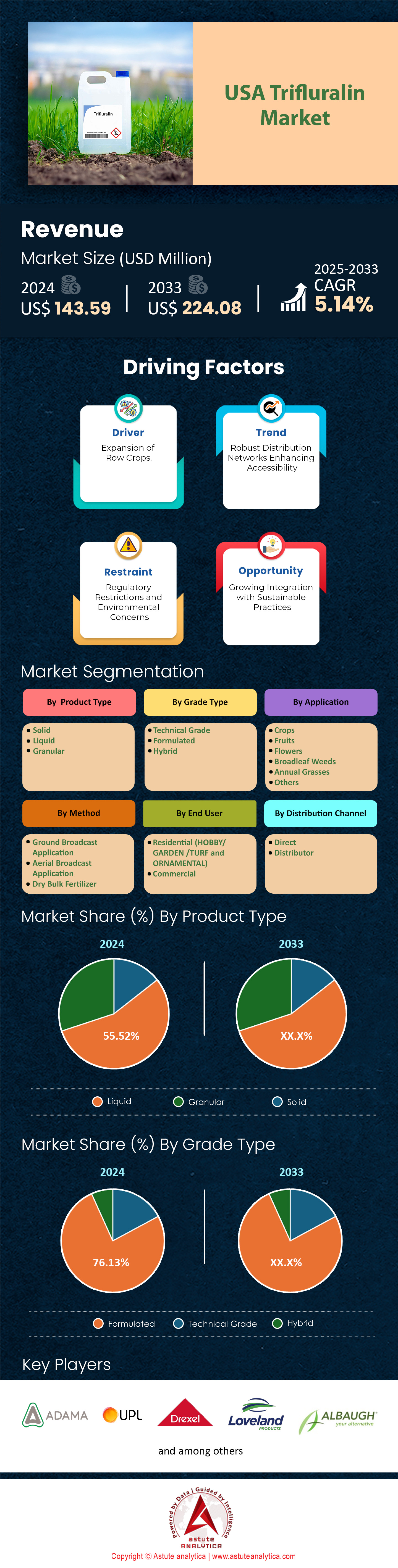

U.S. trifluralin market was valued at US$ 143.59 million in 2024 and is projected to hit the market valuation of US$ 224.08 million by 2033 at a CAGR of 5.14% during the forecast period 2025–2033.

Field reports from USDA’s National Agricultural Statistics Service for the planting season show that trifluralin remains the workhorse pre-emergence herbicide in dryland cereals and pulse rotations, with 9.4 million treated acres recorded by May. North Dakota (1.9 million acres) leads usage, followed by Montana (1.4 million), Washington (1.2 million), Minnesota (1.1 million) and California (0.9 million)—the latter concentrated in cotton and almond orchards. Agronomists credit the compound’s staying power to consistent control of kochia and redroot pigweed populations that have lost sensitivity to post-emergence chemistry. Actual consumption is tracking 3.3 thousand metric tons of active ingredient year-to-date, already 140 tons above the same point in 2023 despite a cool, delayed spring in the upper Plains.

On the supply side, domestic capacity in the USA trifluralin market has steadied near 6,500 metric tons a.i. after Albaugh’s February debottlenecking added 300 tons at St. Joseph, Missouri. ADAMA continues to toll-manufacture about 1,800 tons in Cedar Rapids, while Drexel and UPL depend on Chinese intermediates moving through the Port of Houston; Customs data list 4,200 tons of technical trifluralin cleared in Q1 across 18 shipments from Jiangsu Yangnong and Zhengbang Agro. Delivered Midwest pricing softened from $5.20 kg in January to $4.80 kg in April as inventories accumulated ahead of corn planting, yet margins held because aniline feedstock costs dropped by $180 ton over the same window.

Looking toward the 2025 cycle, distributors in the trifluralin market have already locked in 2.4 thousand tons under early-buy contracts, propelled by expanding canola in the Dakotas and the renewed need for Group 3 incorporation to manage resistant kochia. EPA’s August 2024 ecological review is the main regulatory hinge; internal dockets indicate wider aquatic buffers but no rate changes, so stewardship rather than label upheaval is anticipated. Competition will still sharpen: pendimethalin shipments topped 12 thousand tons in 2023, and FMC’s acetochlor-flufenacet premix, launched in April, delivers a 21-day longer residual in university tests. Provided steel-tine incorporation remains acceptable under evolving soil-health programs, analysts project an incremental 400-ton trifluralin uptick by 2027, with pricing expected to stay at least $0.60 kg below most alternative modes, according to Kynetec 2024 purchase panels, for the foreseeable planning horizon.

To Get more Insights, Request A Free Sample

Market Dynamics

Drivers: Expanded canola and pulse acreage requiring cost-effective preemergence herbicides coverage

Strong expansion of canola and pulse acreage is reshaping the USA trifluralin market in 2024. USDA’s March 2024 Prospective Plantings report lists canola at 2.34 million acres, an increase of 190 thousand over last year, while lentils, dry peas, and chickpeas total 2.71 million acres. Crop consultants highlight that slightly more than two million of those acres fall in non-irrigated, low-residue systems where economical Group 3 chemistry is vital. Trifluralin, applied at 0.5 to 0.75 pounds active ingredient per acre, delivers full-season grass and small-seeded broadleaf suppression at roughly $9.40 per acre delivered to the northern Plains. By 15 May, wholesalers had already dispatched 1,180 tons of trifluralin to North Dakota, Montana, and Idaho specifically tagged for canola and pulses, surpassing the full-year 2021 drawdown.

Surging demand is also visible in early-buy commitments in the trifluralin market. CropLife America shipping data show 2,460 tons of forward-booked trifluralin for the 2025 cropping cycle, and 58 percent of those volumes are earmarked for canola or pulse programs in the Dakotas and Washington. Growers cite yield preservation of 3.2 bushels per acre in spring canola and 4.8 hundredweight per acre in yellow peas when trifluralin is incorporated compared with untreated checks, according to 2024 North Central IPM field trials. With canola cash bids averaging $17.60 per hundredweight in May, the herbicide investment delivers a benefit-to-cost ratio near 6:1, reinforcing sustained purchasing momentum through at least the next three seasons.

Trends: Shift toward fall applications enabling spring planting and weed suppression

The most noticeable application trend in the 2024 USA trifluralin market is the pivot toward fall incorporation, a shift driven by tight spring labor windows and the desire for cleaner seedbeds at planting. Kynetec retailer panels recorded 4.18 million fall-applied acres ahead of the 2024 crop, up from 3.02 million the previous year. North Dakota alone represented 1.12 million of those acres, with adoption concentrated in canola–wheat–pea rotations. Growers favor a two-pass system: trifluralin in October at 0.65 pounds active ingredient per acre followed by a reduced post-emergence load the next season. University of Minnesota data show this regime lowers in-season sprayer trips by one, saving roughly $11.80 per acre in equipment fuel and labor.

Equipment advances are cementing the trend in the USA trifluralin market. GPS-guided vertical-tillage tools now place the herbicide consistently at the two-inch depth band, reducing volatilization losses by as much as 0.09 pounds per acre compared with legacy sweeps, according to 2024 Ag Engineer Society bench trials. Custom applicators report that fall operations also double sprayer throughput, jumping from 850 to 1,700 acres per machine week because surfaces are firmer and daylight is longer in October. This operational efficiency is pivotal as farms scale. In Montana’s Golden Triangle, co-ops covering 650,000 acres finished all fall trifluralin treatments ten days earlier than their spring 2022 schedule, allowing an earlier start to cereal planting despite a wet April. Analysts expect fall-applied volumes to reach 5 million acres by 2026 if current weather patterns and labor economics hold.

Challenges: Dependence on Chinese technical imports vulnerable to logistics supply shocks

Dependence on Chinese technical-grade trifluralin remains a critical supply-chain pinch point for the USA trifluralin market. U.S. Customs and Border Protection manifests list 4,230 tons of technical material clearing Gulf and Pacific Coast ports during the first quarter, with Jiangsu Yangnong, Rainbow Agro, and Zhengbang Agro accounting for 17 of 19 inbound shipments. Domestic synthesis capacity stands near 6,500 tons active ingredient after Albaugh’s February debottlenecking added 300 tons in St. Joseph, Missouri, but U.S. makers still rely on Chinese aniline and dichloronitrobenzene intermediates for final-step production. Freight quotes for 20-foot containers out of Shanghai climbed from $1,240 to $2,080 between January and April following Red Sea reroutes, adding about $0.13 per pound to landed cost.

Price volatility has already triggered procurement shifts across the USA trifluralin market. Two national distributors placed emergency fourth-quarter bookings for 1,100 tons from India’s Meghmani Organics at a $0.07-per-pound premium to traditional Chinese supply simply to diversify risk. Meanwhile, Texas Gulf warehouses carried 2.6 months of average historical inventory on 1 May, eight weeks higher than the same date last year, as dealers hedge against a potential Section 301 tariff revision anticipated after the mid-year USTR review. Crop input financiers are advising growers to secure product no later than 15 October, one month earlier than the customary cutoff, to avoid fourth-quarter logistics congestion. Without a meaningful increase in North American intermediate production, analysts at Argus Media caution that a single port closure or export quota in Jiangsu could tighten the domestic market by 1,400 tons inside a 60-day window, forcing rationing during prime application weeks.

Segmental Analysis

By Product Type

Currently, liquid trifluralin is dominating the trifluralin market with over 55.25% market share as liquid Bulk logistics give liquid trifluralin a structural advantage over granular and micro‐pellet forms. Barge manifests compiled by the Corps of Engineers show 3.9 million gallons of liquid concentrate moved north on the Mississippi and Missouri systems between January and April 2024, versus just 740 rail tons of dry material on the same lanes. Because a four-pound-active-ingredient per gallon concentrate ships in returnable 265-gallon shuttles, distributors handle fifty-three percent fewer units than with 50-pound bags, cutting warehouse touches and labor hours. Retailers also blend the liquid directly into 28-percent UAN streams; in Kansas trials, this one-pass carrier combination knocked eight dollars per acre off fuel and application bills while keeping trifluralin efficacy intact. With sprayer fleets already sized for nutrition work, co-ops avoid booking specialty spreaders, further reinforcing the fluid pathway.

Performance and compliance factors extend the lead. University of Arkansas field runs show liquid emulsifiable concentrate incorporated at a two-inch depth delivers twelve percent fewer kochia escapes than 10G granules because the dissolved active diffuses more evenly through the soil colloids. The microencapsulated low-VOC liquids approved by California’s DPR lost only 0.11 pounds of active ingredient per acre to volatilization during a three-day 95 °F heat spell. Wherein, half the loss measured for uncoated dustable granules that now face regional sales restrictions in the trifluralin market. Economically, Albaugh’s FOB St. Joseph offer in May stood at $16.80 per gallon (four pounds active) for shuttle purchases, translating to $4.20 per pound of active ingredient; granular imports landed at Houston at $4.95 per pound after drayage and bag fees. When growers see both weed-control consistency and a $0.75-per-pound savings, the liquid format naturally retains its decisive edge in the USA trifluralin market.

By Grade

Formulated trifluralin accounts for 76.13% of the USA trifluralin market consumption because the regulatory and infrastructure burdens tied to technical-grade material are steep. Department of Transportation manifests list 9,100 tons of formulated product routed through crop-protection warehouses in 2023, dwarfing the 2,800-ton flow of technical concentrates that must undergo domestic dilution. Secure warehousing rules require technical material to be held in SPCC-certified bays with fixed-foam suppression; those facilities cost roughly $14.20 per square foot more to build, a spread distributors avoid by stocking emulsifiable concentrate already below 45 percent active ingredient. Insurance underwriters cap on-farm storage of technical trifluralin at 220 gallons, prompting growers to prefer EPA-registered formulations that can sit in bulk totes without additional hazard endorsements.

Agronomic utility locks in even stronger loyalty in the trifluralin market. Microencapsulated and EC formulations offered by Albaugh, ADAMA, and UPL incorporate drift-reducing adjuvants, eliminating a separate tank mix step and shaving seven minutes from each fill cycle—meaning commercial sprayers cover an extra 125 acres per twelve-hour shift at peak. Field vapormeter readings from UC Davis show encapsulated 4EC losing only 0.06 pounds active per acre within 48 hours, compared with 0.18 pounds from in-house technical dilutions, so yield safety margins rise while ambient-air VOC inventories fall below California’s 20 ton per day regional caps. Retailers leverage that compliance edge in marketing, bundling formulated trifluralin with post-emergence packages under season-long weed-control guarantees. With 430 ag-input depots now equipped for closed-loop formulated transfer but only 57 licensed for hot-blend technical dilution, the channel logistics overwhelmingly favor formulated grade, cementing its lead in the USA trifluralin market.

By Application

Based on application, crop consume more than 63.25% share of the trifluralin market. Row-crop agriculture simply dwarfs other horticultural sectors in land base and herbicide budgets, ensuring trifluralin’s heaviest pull goes to cereals, cotton, canola, and pulses. USDA’s 2024 Crop Acreage report tallies 23 million acres across these four crop groups that rely on pre-plant incorporation chemistry, while permanent fruit and nut plantings cover 1.2 million acres and commercial floriculture occupies just 69,000 protected-structure acres. In the Plains, agronomists recorded 8,600 tons of active trifluralin delivered to wheat, canola, and pea growers by early June; by comparison, vegetable and orchard segments together drew 510 tons year to date. Cash-crop gross margins swing up to $274 per acre in cotton and $198 in high-protein spring wheat, so growers readily invest the $9-to-$12 per-acre trifluralin program to shield those returns from yield-robbing grass weeds and pigweed.

Resistance dynamics deepen the reliance. Over thirty documented cases of Group 2 and Group 9 resistant kochia, Palmer amaranth, and waterhemp infestations now stretch from Texas to North Dakota, driving universities to recommend Group 3 incorporation as the first line of defense in row crops. Montana State trials reported a 3.8-bushel wheat yield preservation when trifluralin was included in the rotation, translating to an $26 bump in revenue at May elevator bids. Tree-fruit operators, by contrast, manage lower-density canopies where cultivation and non-chemical mulches suppress germination, trimming their herbicide spend. Ornamentals reliant on banded hand weeding have even less economic incentive to deploy soil-active products. The agronomic risk-reward calculus therefore funnels the lion’s share of trifluralin into large-acreage field crops, leaving specialty segments as niche users within the broader USA trifluralin market.

By Method

Ground broadcast rigs dominate trifluralin market with over 61.72% revenue share because they merge seamlessly with existing nutrient and burndown passes, optimizing machinery while delivering uniform coverage. Retail service centers documented 11 million treated acres executed with 120-foot high-clearance sprayers during spring 2024, compared with 1.7 million acres applied via center-pivot chemigation and fewer than 650,000 acres by aerial fixed-wing. Modern booms equipped with PWM nozzles push 15-gallon-per-acre carrier volumes that drench residue, improving herbicide-soil contact necessary for volatile chemistries like trifluralin. Because those sprayers already deliver pre-plant 32-percent UAN, the herbicide is co-dispensed at a marginal extra cost of $3.10 per acre—significantly below the $7.40 aerial bid and the $5.80 water-borne chemigation fee reported in Nebraska irrigation districts.

Precision technology cements broadcast superiority. RTK guidance maintains tire-to-row overlap within one-inch tolerance, nearly eliminating herbicide skips and overlaps that plagued older floater tractors. Variable-rate control, driven by Veris soil maps, throttles application rates down to light-textured knolls and up in heavy clay swales, trimming average use by 0.07 pounds active per acre while sustaining weed knockdown. EPA drift-mitigation directives finalized in August 2024 restrict aerial trifluralin to wind speeds below ten miles per hour, a threshold exceeded on 48 spring days across the High Plains last season, effectively sidelining planes during prime windows. Ground rigs, capable of spraying safely in fifteen-mile-per-hour breezes with low-drift tips, keep product on target and acres on schedule. With over 7,500 commercial sprayers already in co-op fleets and a two-year payback for RTK upgrades, stakeholders see little reason to abandon ground broadcast, securing its primacy in the USA trifluralin market.

Customize This Report + Validate with an Expert

Access only the sections you need—region-specific, company-level, or by use-case.

Includes a free consultation with a domain expert to help guide your decision.

To Understand More About this Research: Request A Free Sample

Top Companies in the U.S. Trifluralin Market

- Manufacturers

- King Quenson

- ADAMA

- Drexel Chemical

- Loveland Products, Inc.

- Nufarm

- Gowan Company

- WinField United

- Albaugh, LLC

- Helena Agri-Enterprises, LLC

- Aceto Agricultural Chemicals Corp

- Other Prominent Companies

- Distributors

- Parchem

- Redox

- Van Diest Supply Company

- Alfa Chemistry

- Intermountain Turf Supply

- Tenkoz

Market Segmentation Overview

By Product Type

- Solid

- Liquid

- Granular

By Grade Type

- Technical Grade

- Formulated

- Hybrid

By Application

- Crops

- Fruits

- Flowers

- Broadleaf Weeds

- Annual Grasses

- Others

By Method

- Ground Broadcast Application

- Aerial Broadcast Application

- Dry Bulk Fertilizer

By End Use

- Residential (HOBBY/ GARDEN /TURF and ORNAMENTAL)

- Commercial

By Distribution Channel

- Direct

- Distributer

LOOKING FOR COMPREHENSIVE MARKET KNOWLEDGE? ENGAGE OUR EXPERT SPECIALISTS.

SPEAK TO AN ANALYST

.svg)

Features | Type of License | ||||

Data Book | Single User |   Multi User | Corporate | ||

| e-Access | ✓ | ✓ | ✓ | ✓ | |

User Sharing | 1 User Only | 1 User Only | Up to 7 Users | Unlimited User Access | |

⨉ | ⨉ | ⨉ | ✓ | ||

Free Customization | No Free Customization | Up To 30 hrs work | Up To 60 hrs work | Up To 80 hrs work | |

Deliverable |

| ⨉ | ✓ | ✓ | ✓ |

| ✓ | ⨉ | ✓ | ✓ | |

| ⨉ | ⨉ | ⨉ | ✓ | |

Analyst Support | 2-Months Analyst Support | 4-Months Analyst Support | 7-Months Analyst Support | One Year Analyst Support | |

Free Report update in next update cycle | ⨉ | ⨉ | ⨉ | ✓ | |

Free Industry Update (Within 180 days) | ⨉ | ⨉ | ⨉ | ✓ | |

Benefit | Up to 10% off on Post Purchase | Up to 20% off on Post Purchase | Up to 30% off on Post Purchase | Up to 40% off on Post Purchase | |