Market Scenario

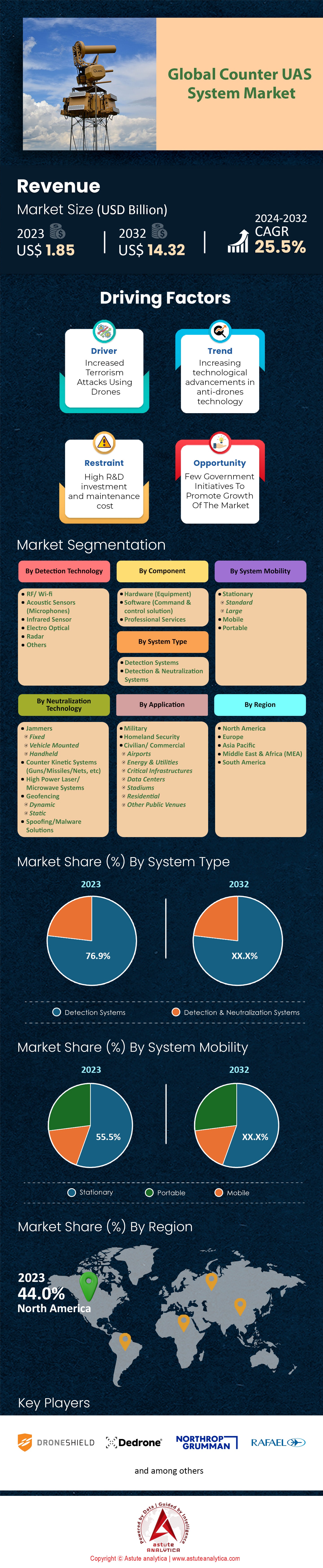

Global counter UAS system market was valued at US$ 1.85 billion in 2023 and is projected to hit the market valuation of US$ 14.32 billion by 2032 at a CAGR of 25.5% during the forecast period 2024–2032.

Counter Unmanned Aircraft Systems, or more simply Counter-UAS, are modern techniques intended for finding, pursuing, recognizing, and destroying illicit unmanned aerial vehicles. Thanks to the swift growth of these inexpensive drones, the demand for Counter-UAS systems is gradually increasing. In recent years, the Federal Aviation Administration (FAA) in the USA has more than 1.7 million registered drones indicating a rapid growth in the activities of UAVs in the national airspace. Proponents of development of drones in the counter UAS system market also saw the attendant security threats of drone traffic in huge metropolitan areas. In airports, drones have caused delays and warnings that they are disruptive devices, a major reason for the frowning of the population on their use. This growth has raised concerns of security as there have been reports of drones interfering with airport operations, the most notable being the Gatwick Airport incident where flights were grounded for about 36 hours, affecting over 140,000 passengers. Some of these include the need to secure essential facilities, manage airborne activities and prevent the use of UAV for illegal purposes like drugs, and espionage.

The primary end users of counter UAS system market are military and defense industry, governmental organizations or agencies, law enforcement authorities, airport administration and officials, organizers of events and operators of critical infrastructure, such as nuclear power plants or oil refineries. As an example, the U.S. army has integrated weapon systems classified under C-UAS at many US bases to avoid being spied and attacked, with the figures depleting over two hundred incidents in sensitive areas over a reporting period from 2016 onwards. Other uses of these systems also include the protection of structures such as the perimeter of large buildings, the protection of mass gatherings held in public and the protection of the country’s border. The components of Counter-UAS systems, include radio frequency or RF detection, radar systems, electro optical or infrared EO and IR sensors and electronic combat systems including jammers and spoofers. Also, weapons that use directed energy such as high energy lasers have been made to shoot down drones and countries such as Israel have systems that can shoot down drones while in flight.

Targeting improvement of the response elements and anti-surveillance mechanisms are some of the recent technological developments I nthe counter UAS system market/ In line with this, the investments in the market have moved forward. With regards to this technology, government funding of Counter-UAS R&D has also been on the rise, for instance, about US$ 600 million were spent by the US department of defense on such technologies in 2020. Investment from the private sector is also great, with industrial reports indicating that investment in counter UAV technology was over US$ 1 billion as of 2021. Classic defense suppliers have developed advanced Anti-Drone systems based on the use of Artificial Intelligence and machine learning for better threat evaluation and for management automation. Thus, for example, Lockheed Martin displayed its MORFIUS system, a multifunctional high-power microwave-based system with a promise to counter drone swarms. The global Counter-UAS market had an approximate id of US$ 1.2 billion in the year 2021 and is expected to grow at a healthy rate with the increasing requirement of security and the ever-growing capabilities of drone technologies.

To Get more Insights, Request A Free Sample

Market Dynamics

Driver: Increased Drone Threats Necessitate Advanced Counter UAS Technology for Security Measures

The increasing use of drones in the counter UAS system market is contributing to the rise of threats and security concerns in different areas and yet advanced counter UAS solutions have become a requirement. In just the past few years, drones have become affordable, with commercial drone registrations exceeding 2.5 million worldwide. This net growth has also resulted to increased illegitimate use of drones with reports of 1500 open air space violations in the last year alone. There has been an increase in illegal drone flights into critical infrastructures, airports and those housing nuclear facilities with more than 200 close encounters reported at core airports in 2023, which have resulted in temporary closure of flight operations. The threats do not end on infrastructure as there is an alarming rise of drone usage for crime purposes. Even more disturbing is the fact that over 500 case reports were made by law enforcement on the use of drones for smuggling crimes into and out of prisons and countries through borders in the year 2023.

Threats such as this, led to the emergence of the counter UAS system market and significant investments in the development of various advanced detection and neutralization technologies. It has been reported that by 2032, the global counter UAS market size will increase by more than 7 times to reach US$ 14.35 billion at the rate of security needs in this case. Rainbow's report states that more than 120 companies are developing counter-drone technologies centered on radar systems, radio frequency detectors, and laser-based detection systems. In 2023, 65% of newly developed counter drone systems aimed at improving accuracy and response time used artificial intelligence. Also, different agencies of the government all over the world have invested more than US$ 1 billion into counter UAS technology R&D, showing that this area is being taken seriously.

Trend: Growing Demand for Portable and Mobile Counter UAS Solutions for Field Operations

The need for portable and mobile counter UAS solutions continues to grow in the global counter UAS system market as these organizations look for counter-measure from aerial threats in various surroundings. There were over 1 million commercially sold drones in the last year which paved the way for versatile on-field counter-drone systems. In 2023, more than 300 field operations including, military drills and security coverage over large events, required mobile counter UAS systems. Deploying such systems as quickly as possible is necessary given the wide variety of locations and scenarios such as urban and rural ecosystems where drone threats may exist. Hence, there is a considerable expectation for growth of this portable UAS counter measures related systems market as expansion to $2 billion is anticipated by year 2026 from the expansion in the market for military and civilian users.

With the increasing demand, manufacturers in the counter UAS system market are coming up with new portable counter-drone systems and other products which are quite effective but do not compromise in portability. The latest systems are below the mass of 10 kilograms allowing them to be handled by one individual and also deployed very fast making them very useful in rapid response scenarios. In 2023 according to the reports, more than 40 new mobile counter UAS products were presented and expanded their functionalities with such capabilities as being incorporated into the existing systems and real-time data exchange. Also the majority of the systems over 70 % are now modular which means that users can adapt the system based on the requirement of the operation. The increasing trend of mobile solutions to the problem and this is very encouraging as it moves with the evolving nature of drone threats and equips the security personnel with the right tools to safeguard vital institute.

Challenge: High Costs of Development and Deployment Limit Widespread Adoption of Counter UAS

There is an urgent need for counter UAS technologies in the current situation. However, the costs for developing and using these technologies create a considerable bottleneck for mass entry in the counter UAS system market. A lot of expense is necessary to come up with state of the art counter-drone systems, which calls for over US$500 million in research and development expenditure in the year 2023 alone internationally. The need to integrate the design of drone detection, tracking, and interception systems has made the designs hereof high-cost. Besides, the average costs for the installation and thereafter the maintenance of the system per unit are very high, at about $200,000, which many organizations would find even impossible trying to deploy the mechanisms over several sites. The cost of these technologies is one of the issues that hamper the fight against unmanned aerial systems, especially for smaller entities and nations with low funding.

The expenses are further limiting the potential growth of counter UAS system market rendering the development of new and more complex multi-layered defense systems more difficult. Nowadays the facts demonstrate that only 30% of airports and strategic facilities have been able to apply advanced counter-drone technologies, which stresses the unevenness in the implementation of such technologies. The market is expected to shift towards innovations and economies of scale to lower costs as manufacturers project to cut production costs by 15% in the next five years. The same challenges would require government sponsored programs designed to assist in cost reimbursements and support programs that encourage collaboration in research. Also quite encouraging is the fact that there are public-private initiatives aimed at resource consolidation in order to reduce costs. Solving the economic problems is important for broadening the scope of counter UAS technologies in all domains and handling the negative drone impacts on humankind.

Segmental Analysis

By System Type

Based on system type, the detection system is leading the counter UAS system market with over 76.9% market share. There are a number of reasons responsible for the rise of detection systems in the counter-UAS market. First and foremost, there are certain reasons that cause this predisposition to the determination of the need for detection and not neutralization. Detection systems, which include radar, RF sensors, and optical systems, aid in the identification and tracking of the airborne vehicles at a safe distance without attempting to engage with them immediately. This strategy conforms to the regulatory measures and the requirement of considering the potential fallout of the engagement in highly populated or sensitive locations. As was the case in 2023, the bottom line is that, to avoid unnecessary escalations through the necessity of using force to neutralize items of concern, early warning should be prevalent. The purchase of advanced drone detection systems in Tokyo, to be used during the security summit in Tokyo 2023 meant protection against aerial attack, signifying that everywhere is going for the strengthen detection systems.

The increasing interest in these detection systems around the global counter UAS system market is driven by concerns over privacy issues, security risks, and airspace security. The forecast suggests that in the year 2024, the number of drones sold worldwide is expected to total 9 million units, including over 3 million units of commercial drones. This increase emphasizes the need for proper detection systems. And, the initiative of the European Union to standardize drone detection requirements for all member states by 2024 shows the extent of regulatory forces which will help this segment grow. Although the Evidence Drones Segment will continue to grow in the future because of technological advances like cloud-based AI analytics for integrated threat detection The products launched by Dedrone Ethos and DroneShield listed on their 2024 product release show a new trend on compact and portable detection devices suggesting a trend towards multifunctional and cost effective solutions. The growing deployment of detection systems into primary places such as airports and stadiums strengthens their importance in the changing security paradigm, thus securing growth prospects for the segment in the foreseeable future.

By Detection Technology

RF/WiFi technology in counter UAS system market is the frontrunner with more than 31.3% market share. The largest share of the counter UAS system market is being held by the RF/Wi-Fi technology. The primary factor enabling its growth is the facility to safely and securely pinpoint, investigate and eliminate invasive drones. The RF/Wi-Fi systems focus on monitoring the interaction between the drone and the operator and are able to paralyze the communication channels without breaking the drone or disturbing other areas. In terms of revenue, the counter-UAS market exceeded $2 billion in 2023 with a large part being captured by RF/Wi-Fi systems owing to their cheapness and versatility in operation. This cross usefulness of RF/Wi-Fi components with commercial applications such as engagement of Surveillance cameras and Radar has also enhanced their adoption. In addition, currently, more than 500 companies around the world are developing RF/Wi-Fi counter-UAS systems, which implies that this sector of the Industry has a strong orientation towards it.

Another major element is the relentless improvement of the RF/Wi-Fi technology, which resulted in the introduction of advanced functionalities such as the algorithms for machine learning as signal enhancement techniques. This is for example, the most recent models in the counter UAS system market that can trace a drone from a distance of over twenty kilometers, something that has almost doubled within the last five years. Regarding the applications, it is observed that the RF/Wi-Fi systems are largely employed in the defense of critical installations such as the airports, correctional centers, and state edifices. In 2024 alone, there are over 1,200 airports around the world using RF/Wi-Fi-based counter-UAS solutions to date. Due to the nature of RF/Wi-Fi systems, they emerge the best option compared to the conventional kinetic systems as they are able to keep pace with the different drone environments and manage multiple drone threats at the same time. In addition, the practice of deploying over thirty RF/Wi-Fi counter-UAS systems in various countries indicates the global dispensability of these systems in improving airspace safety. With the increase in drone usage where more than 15 million drones are predicted to be in use by the year 2025.

By Neutralization Technology

Based on neutralization technology, jammers in the counter UAS system market is forming a major portion covering over 74.1% market share owing to the efficiency with which they manage to neutralize drone attacks by disrupting their communication and navigation systems. This demand is fueled by the growing number of illegal flying objects that represent a threat as they can be used for spying, for transport of illicit goods or terror activities. As of 2023, over 2000 different countries reported the occurrence of security incidents where drones were involved confirming such an urge. In addition, the global drones market is set to be valued at $58 billion driven in large part by the commercial and consumer adoption of drones which are also forecast to fuel the growth of the drones market. This advancement in the operations of the drones has made the demand for security systems operational due to the operational focus on jammers or otherwise.

There are several reasons that are responsible for the growth of jammers segment in counter UAS system market. First, technology development including hardware and software facilitating more efficient and reliable jamming systems caters quite well to the expanding market of jammers. In 2023, $3 billion of the defense industry budget was aimed at counter drone technologies and this is significant to the development and use of jammers. In support, over 50 countries have enacted or instituted new regulations against the use of drones, thereby indicating that jammers are needed even more to ensure compliance and secure airspace. Jammers market is the fastest growing in the areas of national security, protection of vital infrastructure and protection of mass events due to high probability of drones usage.

In response to the growth of the jammers segment, players in the counter UAS system market are engaging in research and development activities. Over 200 companies worldwide pay attention to Counter-UAS technologies. According to reports, the five biggest players in this space invested $500 million in developing jammer capabilities in the year 2023. Furthermore, there is a noticeable increasing trend towards collaboration and M&A, as evidenced by the formation of thirty additional strategic partnerships within the technical and defense industry for innovations approval. Moreover, the companies are widening the scope of their product range with the introduction of portable and vehicle mounted jamming systems targeting different operational requirements. Due to this, the jammers segment is optimistic with many forecasts estimating the segment to be worth $2 billion by the year 2025.

By System Mobility

Of all the mobility systems in the counter UAS system market, stationary system accounted for more than 55.5% of the market share. These systems have a very large degree of reliability which makes it easy to offer protection to all critical infrastructure like airports, government Centers, and military Bases. Stationary systems are fully equipped with modern radar, RF detection systems, and advanced electro-optical sensors which can incapacitate intruder drones within a great distance. On 'the other hand, a recent research report stressed that more than 2000 main airports in the all over world have included stationary counter UAS system into their security measures and management to prevent terrorist actions. The resilience of stationary systems is also observable in that they are established in more than 500 metropolitan cities where use of these devices enhances safety during mass gatherings events.

Other than their own technical aspects, stationary systems in the counter UAS system market are also in demand for their economics and easy expansion In addition, the cost required for the maintenance and operational activities for these systems is much lower than that of mobile counterparts hence making these systems a favorite for small budget organizations. In the year 2024, statistics indicated that more than 1,500 municipalities in Europe alone had integrated stationary counter-UAS systems, among them a promising reduction of the costs in the long term. Moreover, the advent of AI and machine learning technologies has improved the versatility of such systems, making them more effective against numerous drone threats as they emerge. This, coupled with the award of contracts by providers of stationary systems, reflects the need for such systems as bases in the in this year over 300 new tenders were floated in the Asia-Pacific counter UAS system market and awarded. With the increasing focus and use of urban air mobility and drones, there is a demand for effective counter-UAS solutions and this UAS defense installation will also continue to growth with industry experts forecasting a deployment of stationary systems in another 1800 locations across the globe by 2025. As a result stationary counter-UAS, systems are what is prevailing in the market now and they are bound to influence the aerial defense as well in the future.

Customize This Report + Validate with an Expert

Access only the sections you need—region-specific, company-level, or by use-case.

Includes a free consultation with a domain expert to help guide your decision.

To Understand More About this Research: Request A Free Sample

Regional Analysis

North America was by far the leading counter UAS system market in 2023 with more than 44% of the share primarily due to its improved technological landscape and allocation of budget for defense. In this, the U.S. has, for instance, set aside over US$700 billion towards defense budget and part of it goes to counter-UAS technologies. Investment in the progressive anti-UAS systems had also grown due to the growing concerns regarding the homeland security and increasing threats of drone usage. In 2023, the U.S. Department of Defense has even carried out more than 50 tests using various counter-drone technologies Of these, radar and jamming countermeasures have received the most attention. Also, the American based companies like Raytheon and Boeing seem to have the latest technologies and systems in place and even lead in the filings of patents for drone countermeasures. The FAA has granted more than 10,000 drone operation waivers which calls for effective counter-UAS systems. It is also noteworthy that more than 100 joint ventures have been created as a result of interaction of these tech giants with defense establishments in order to bolster counter-drone capabilities securing North America’s top place in this market.

In Europe counter UAS system market, counter-UAS technologies and systems have shown positive growth as the threat of unauthorized drones penetrating sensitive areas such as airports and generating harms to the critical infrastructure has risen. Within a year, the member states of EASA have had more than 200 cases concerning drone near airports, which is why their governments take steps with the use of counter-UAS technologies, giving a boost to the counter UAS system market. France and Germany has taken the lead wherein France has more than 30 counter drone system deployment projects underway. The UK’s Ministry of Defense has allocated over £160 million towards the development of technologies that deal with targeting hostile drones. Companies in Europe including Airbus are making strides in the development of laser-oriented anti-drone systems and have performed over 40 tests. The support of the European Commission for drone security has been more than €1 billion until 2025. Another point to note is that one of NATO's military exercises has included the anti-drone warfare element in more than 20 joint operations, showing how structures are committed to advancing the prospect of defending against drones in the region.

Asia Pacific counter UAS system market is projected to expand at robust CAGR due to increased military capabilities and the growth of the commercial drones. Wherein, China and India are in the advance position, it is also worth mentioning the 500 million yuan investments by the Chinese government in the development of anti-drone technologies. Future counter UAS systems have been used in the Indian Armed Forces over 100 times in recent years. In Japan, the defense ministry aimed at defending the Tokyo Games allocated over 200 billion yen for counter drone technology respectively. The region is gaining speed in the commercial drone market, there are more than 1 million registered drones in China that requires effective counter-UAS systems to be put in place. Over 500 incursion of drone into restricted areas in the republic of Korea was reported leading to the emergence of a framework for national defenses against drones. In addition, more than 10 forums for drone security were organized by the Asia-Pacific Economic Cooperation which indicates that the region is moving quickly in preparation for combat against the drone systems.

Top Players in Global Counter UAS System Market

- Lockheed Martin Corporation

- Thales Group

- Northrop Grumman Corporation

- Northrop Grumman Corporation

- The Boeing Company

- Saab AB

- ELBIT SYSTEMS LTD.

- Raytheon Technologies Corporation

- Leonardo S.p.A.

- Robin Radar Systems

- Diehl Stiftung & Co. KG

- General Dynamics Corporation

- HENSOLDT

- Aselsan

- QinetiQ

- Rheinmetall AG

- D-Fend Solutions AD Ltd.

- Dedrone

- DroneShield Ltd

- Aaronia AG

- Advanced Protection Systems S.A.

- Apolloshield

- AVNON Group

- CERBAIR

- BLUEHALO

- Sentrycs

- Fortem Technologies

- DETECT, INC.

- Rafael Advanced Defense Systems Ltd.

- Rohde & Schwarz

- Squarehead Technology AS

- TRD Systems Pte Ltd.

- Other Prominent Players

Market Segmentation Overview:

By Component

- Hardware (Equipment)

- Software (Command & control solution)

- Professional Services

By System Type

- Detection Systems

- Detection & Neutralization Systems

By Detection Technology

- RF/ Wi-fi

- Acoustic Sensors (Microphones)

- Infrared Sensor

- Electro Optical

- Radar

- Others

By Neutralization Technology

- Jammers

- Fixed

- Vehicle Mounted

- Handheld

- Counter Kinetic Systems (Guns/Missiles/Nets, etc)

- High Power Laser/Microwave Systems

- Geofencing

- Dynamic

- Static

- Spoofing/Malware Solutions

By System Mobility

- Stationary

- Standard

- Large

- Mobile

- Portable

By Application

- Military

- Homeland Security

- Civilian/ Commercial

- Airports

- Energy & Utilities

- Critical Infrastructures

- Data Centers

- Stadiums

- Residential

- Other Public Venues

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- Western Europe

- The U.K.

- Germany

- France

- Spain

- Italy

- Rest of Western Europe

- Eastern Europe

- Poland

- Russia

- Rest of Eastern Europe

- Western Europe

- Asia Pacific

- China

- India

- Japan

- Australia

- ASEAN

- South Korea

- Rest of Asia Pacific

- Middle East & Africa (MEA)

- UAE

- Turkey

- Saudi Arabia

- South Africa

- Rest of MEA

- South America

- Argentina

- Brazil

- Rest of South America

LOOKING FOR COMPREHENSIVE MARKET KNOWLEDGE? ENGAGE OUR EXPERT SPECIALISTS.

SPEAK TO AN ANALYST

.svg)

Features | Type of License | ||||

Data Book | Single User |   Multi User | Corporate | ||

| e-Access | ✓ | ✓ | ✓ | ✓ | |

User Sharing | 1 User Only | 1 User Only | Up to 7 Users | Unlimited User Access | |

⨉ | ⨉ | ⨉ | ✓ | ||

Free Customization | No Free Customization | Up To 30 hrs work | Up To 60 hrs work | Up To 80 hrs work | |

Deliverable |

| ⨉ | ✓ | ✓ | ✓ |

| ✓ | ⨉ | ✓ | ✓ | |

| ⨉ | ⨉ | ⨉ | ✓ | |

Analyst Support | 2-Months Analyst Support | 4-Months Analyst Support | 7-Months Analyst Support | One Year Analyst Support | |

Free Report update in next update cycle | ⨉ | ⨉ | ⨉ | ✓ | |

Free Industry Update (Within 180 days) | ⨉ | ⨉ | ⨉ | ✓ | |

Benefit | Up to 10% off on Post Purchase | Up to 20% off on Post Purchase | Up to 30% off on Post Purchase | Up to 40% off on Post Purchase | |